Institutional investors spend tremendous time, money and effort drafting their portfolio of investments and investment managers. Similarly, National Football League teams spend millions of dollars on scouting and analysis, trying to select the best players in the rookie draft. Can investors learn anything about selecting investments by studying how NFL teams select players — including the most recent NFL draft?

The answer is yes. One of us (Thaler) co-wrote a paper on errors in the NFL draft with Wharton professor Cade Massey. The main finding: In spite of spending so much time and money — and the huge stakes involved — NFL teams still make big behavioral errors that let smarter teams draft better and win more games. The primary mistake: NFL teams pay too much for the right to pick early in the draft. Understanding the sources of these NFL draft miscues can provide useful lessons for investing in stocks.

For investors, there are two big lessons. First, the best player does not necessarily make the best draft pick — just as the best company does not necessarily make the best stock to buy. On average the players taken with first-round picks do not provide teams as much value — performance relative to their cost — as players taken in later rounds. Value matters. Second, NFL general managers — like investors — pay too much for glamour and neglect duller, solid performers. Specifically, NFL general managers often overpay for early round draft picks, so they can draft an alluring star — just as many investors overpay for glamorous, fast-growing companies and neglect solid but less exciting ones.

Lesson 1: The best player (or company) does not necessarily make the best pick.

Obviously, teams are not picking players at random, and players taken early in the draft are indeed better, on average, than those taken later. But football players don’t work for free: Earlier draft picks must be paid higher salaries. And because football teams have team salary caps, the salary is not just a financial cost; it is also an opportunity cost. The more a team pays for one player, the less money it has to spend on other players. Even Peyton Manning needs linemen to block and receivers to catch his passes. So the return on investment of a draft pick is not just how good the player turns out to be, but how good the player is relative to his cost.

One of the unique aspects of hiring players via a draft is that players have very limited ability to negotiate their compensation — their salaries are primarily determined by when in the draft they are selected. And while the NFL rookie salaries are high, they are not as high as the salaries for a veteran player of the same caliber. In other words, a big benefit of drafting players is that managers can get a great player at a lower cost. Fans can argue endlessly about whether Peyton Manning or Tom Brady (the 2014 Super Bowl winner) has been the better quarterback, but there can be no debate about which was a better draft pick. Manning was selected with the very first pick and paid a big salary from day one. Brady was the 199th pick, so for the early years of his contract, the Patriots were getting his services (in football terms) for next to nothing.

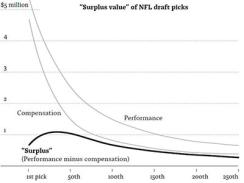

The paper studied all the players selected in the NFL draft from 1983 to 2008, and for each player computed his “surplus value” — that is, the performance he provides to the team minus his compensation. Figure 1 is a graph of the results. The top line shows that performance does decline as the draft proceeds — teams do know something! But while performance declines with later draft picks, compensation also declines. So for any player, surplus value is performance (the top line) minus compensation (the second line). And here’s a result that is shocking to most football fans: Surplus value increases throughout the first round of 32 teams. And even later rounds provide almost as much surplus value as the first picks.

Value is important when picking players — and when selecting stocks. Great companies often make expensive stocks. There is a long line of research showing value stocks have higher returns. For example, an early paper by Werner De Bondt and Thaler, Does the Stock Market Overreact, showed that value stocks (those with the lowest returns over the past three to five years) — like later draft picks — on average provide a better return on investment. Subsequent research has found that this simple measure of value performs in currencies, government bonds and commodities. On average, value works.

Today, we worry that investors have forgotten to beware of high-priced investments as they pile into ever more expensive government and blue-chip corporate bonds. We suspect investors — like NFL general managers — are forgetting the importance of value.

Lesson 2: NFL general managers (and investment managers) overpay for glamour.

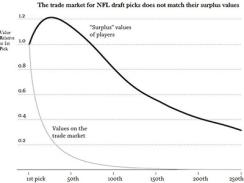

After NFL teams are assigned their seven rounds of draft picks (in reverse order of the previous year’s standings), NFL GMs often trade draft picks. And NFL general managers pay crazy prices to pick earlier. Consider the 2014 draft, when Buffalo gave up a future first-round draft pick (and more) — just to move from ninth to fourth in that year’s draft. Based on dozens of trades over the years, figure 2 plots the average trade price of any draft pick relative the first pick of the draft.

While the surplus value of a second-round pick (that is, the 33rd pick, given there are 32 teams) is slightly higher than the first pick, the trade value is around 0.2, only one fifth as much. In other words, you could typically trade the first pick for five second-round picks — even though a second-round pick provides more surplus than the first one. Talk about an opportunity.

Why does this happen? One behavioral reason is overconfidence. Many teams are just certain that if they had one of those early picks they could select a player who will be a star. But predicting the future is really hard. If you compare two players at the same position taken consecutively — for example, the third and fourth running backs picked in the draft — what do you think is the chance that the earlier one will turn out to be the better player? If teams were perfect forecasters the chance would be 100 percent; if they are flipping coins it would be 50 percent. How do teams do? Just barely better than chance. The player taken earlier has just a 52 percent chance to be the superior player.

Another reason teams overpay for early picks is they overreact to limited data and make extreme forecasts. Teams don’t just predict a player will become an NFL starter; they predict he’ll become a superstar. In the 2012 draft, the Washington Redskins were so confident that Robert Griffen III (or RG3 as he is called) would be a great quarterback that they gave up three years’ worth of first-round picks to get him. Although RG3 had a good rookie year, he got hurt and soon lost his starting job. Meanwhile, Russell Wilson, a quarterback taken 75th in that same draft, has so far led his team to two Super Bowls. Overpaying to get RG3 was a poor investment.

Are teams getting smarter? Not really. In the most recent draft, the Philadelphia Eagles purportedly made an attempt to move up to first or second, offering at least two first-round picks and multiple players as well. Our take: Tampa Bay and Tennessee (the owners of the first two picks) made a mistake to not accept the Eagles’ aggressive offer.

The decision we find most problematic is that of Tampa Bay using its first pick to draft Jameis Winston, a Heisman Trophy winner who has had repeated brushes with the law for shoplifting, alleged rape and other issues. Even if Tampa Bay does not care about potential reputational damage from off-the-field activities, in today’s NFL it is easy to imagine Winston being suspended for yet another infraction — and suspended players don’t win games. Most important, nobody can know if Winston’s college success will translate into NFL success — remember there’s on average only a 52 percent chance he’s better than the second drafted quarterback. In short, Tampa Bay put a lot of eggs in one risky basket. Instead, the team could have made a deal with the Eagles to acquire multiple first-round picks and quality players, thus getting a much more diversified portfolio.

While the Eagles offer this year was high, apparently it was not high enough for Tampa Bay or Tennessee to trade. We suspect that teams are learning not to make offers quite as crazy as the one the Redskins made for RG3 in 2012, but that the teams that own the high picks are still demanding crazy prices to be willing to give up their high picks. This is a bit like what happens in declining real estate markets. There are lots of For Sale signs but not many sales because sellers are reluctant to accept less than their neighbors received before prices fell.

Still, in the 2015 draft, there were 20 trades between teams where one team got more picks, and the glamour-seeking team got an earlier pick. We’ll happily bet anyone that in more than half of those trades, the team that got more picks will ultimately have gotten the better deal.

Another anomaly found by Massey and Thaler is that teams use a simple rule of thumb to trade picks from this year’s draft for picks in next year’s draft: If you give up a pick in a given round this year, you get a pick one round earlier next year. While this might not seem unreasonable, it translates to an interest rate of 137 percent per year. Presumably, most of the billionaire owners of NFL teams did not acquire that kind of wealth by borrowing at such high rates.

By combining the strategies of trading for multiple later-round picks this year and for higher-round picks next year, smarter draft-pick-trading teams (like the New England Patriots) on average win 1.5 more games per season — a huge amount in a 16-game season.

Similarly, smart investors can win in the stock market by trading against biased investors. Research has found that fast-growing, sought-after stocks earn low returns on average, while conservative, neglected stocks earn high returns on average. Whether “fast-growing” is measured by past three-to-five-year returns or asset growth and whether “sought-after” is measured with trading volume or Google searches, the results are the same: Neglected stocks perform better. Similarly, a study of plan sponsors found that sponsors hire managers with glamorous past returns and fire managers with poor past returns — but in the future the fired outperform the hired. Why? Investors overreact to past performance. Smart investors should avoid overreacting.

Biased investors see high-flying stocks (or funds) and imagine they will go up forever. Smart investors sell glamorous stocks and buy neglected stocks instead.

As investors — like NFL general managers — we all have behavioral biases. We are overconfident. We overreact. The trick to overcoming these biases is to use a disciplined system of checklists and guidelines that recognize our own biases. Cheap neglected stocks are not necessarily the best companies but — like later-round draft picks — are often the best investments.

Raife Giovinazzo is director of research at Fuller & Thaler Asset Management in San Mateo, California. Richard Thaler is a principal of Fuller & Thaler Asset Management, professor of behavioral science and economics at the University of Chicago Booth School of Business and author of the recently published Misbehaving: The Making of Behavioral Economics.