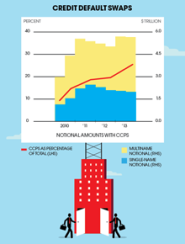

Between Timothy Geithner’s book tour and a continuing stream of billion-dollar fraud settlements with banks, some argue that little has changed as a result of the financial crisis. Try telling that to players in the $710 trillion derivatives market.

Seeking to contain the systemic risk posed by what

Warren Buffett once called financial weapons of mass destruction, global regulators have pushed banks to standardize derivatives contracts and clear trades through central counterparties (CCPs). The impact has been significant. Last year 26 percent of all credit default swaps were cleared through central counterparties, up from less than 10 percent in 2010, the Bank for International Settlements reports. Netting of duplicative contracts, meanwhile, has helped reduce the notional amount of CDSs outstanding to $21 trillion at the end of 2013, down from $29 trillion in 2011 and a peak of $58 trillion in 2007. A similar trend is under way in interest rate derivatives, with CCPs accounting for much of the gain in volume conducted with “other financial institutions.” The BIS report may not make for a bestseller, but it might just avert the need for a future Treasury secretary to write one.