Blu Putnam, CME Group

AT A GLANCE

- Since March 2022, the Federal Reserve has raised interest rates by 300 basis points

- Higher rates are challenging both homebuyers and sellers

There are growing signs that the Federal Reserve’s rate policies are starting to bite into the U.S. housing market.

Mortgage rates on 30-year fixed rate loans have risen from around 3% at the end of 2020 to just over 7% in October 2022 as the Fed has withdrawn its accommodative monetary policy and raised short-term rates. One would have to go back two decades to the year 2000 to find U.S. mortgage rates as high as they are now. (A relatively shallow recession followed that period.)

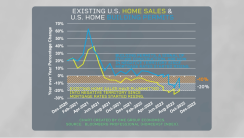

The current higher mortgage rates are clearly impacting the housing market today. Sales of existing homes have dropped to about 20% below year-ago levels, while building permits for new home construction have fallen over 10% below year-ago levels.

But is this housing slowdown likely to be anything as bad as what occurred in the sub-prime mortgage crisis that presaged the Great Recession of 2008-2009? No. It is different this time.

During the Great Recession, the unemployment rate went to 10%. Many borderline home buyers lost the income to pay their mortgages and were forced to sell their homes, deepening the economic crisis.

In 2022, the unemployment rate has yet to rise, remaining below 4% for now.

Equally important, most homeowners are of much better credit quality than in the 2008 debacle, and they are sitting on very low fixed rate mortgages. They can still pay their mortgage, so there’s no forced sales crisis this time around. But homeowners cannot afford to give up the low-rate mortgage to move up, buy a new home and sell their existing one. This means the supply of existing homes will be quite constrained, tempering the housing impact on the economy. Still, new home construction appears headed to a much slower pace in 2023.

Monetary policy acts with a lag, but for the housing market, one can now see that rising rates are taking their toll. However, one may not see the impact in the inflation data for many months to come, as the knock-on effects from a weak housing market take their time to domino through the economy.