Emily Balsamo, CME Group

AT A GLANCE

- With a climate ideal for high-quality, high-protein spring wheat, Western Canada has long been a top grower and exporter

- CME Group’s upcoming launch of Canadian Western Red Spring Wheat futures* introduces an opportunity to participate in one of the most significant global wheat markets

Spring wheat is generally planted in regions with winters too severe to sustain the over-wintering necessary for winter wheat. While winter wheat is planted in the fall and harvested in late spring, spring wheat is planted in spring and harvested in late summer. Canadian Western Red Spring wheat has a higher protein content than most winter wheat, making it ideal for strong bread flour demanded by the highest caliber of bakers. CWRS is also highly valued in Asia for making high-quality noodles, positioning CWRS as a major competitor to high-protein Black Sea and Australian wheat in Asian markets.

An Elite Group

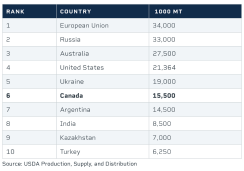

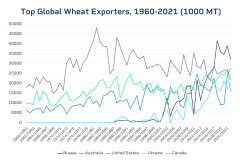

Canada belongs to an elite group of wheat-exporting nations, ranking between two and six among top exporters annually over the past decades. Canada was the world’s sixth largest wheat exporting country in the latest full crop year, with 15.5 million metric tons exported. Vancouver, Canada’s largest and most diversified port, is the primary point of departure for Canadian Western Red Spring Wheat exports.

Since 2014, Canada has exported over 100 million metric tons of CWRS to 80 countries. With almost 13 million metric tons of CWRS received between 2014 and 2021, Indonesia has been the most significant export destination for CWRS over the past eight years. Japan, China, Bangladesh and Colombia round out the top five export destinations for CWRS during this time. Since 2014, almost 55% of CWRS exported from Canada left from Vancouver. In terms of export seasonality from Vancouver, May is the most active month within the year (with August and January also busy), while Q4 tends to see a slowdown in exports.

A Brief History

Canadian wheat was historically traded via the Winnipeg Commodity Exchange, which commenced operation in 1887 (then, as the Winnipeg Grain & Produce Exchange) and established a futures market for wheat in 1904. The Winnipeg Commodity Exchange worked in tandem with the Canadian Wheat Board (CWB), which until 2012 operated as a monopsony, or single buyer, of all Canadian wheat. Since 1960, Canada has accounted for 5.59% of global wheat production.

Source: USDA Production, Supply, and Distribution

Hedging Potential

The upcoming launch of CME Group cash-settled Canadian Western Red Spring Wheat (Platts) futures will present a new tool for farmers, merchandisers, importers and exporters to hedge their exposure to Canadian Western Red Spring wheat markets. This financially-settled product will reflect export prices at the Port of Vancouver and create an opportunity for participants to take an outright hedge or trade the spread/basis of CWRS and other wheat markets, including Chicago Soft Red Winter Wheat, Black Sea Wheat, and Kansas City Hard Red Winter Wheat futures.CME Group Canadian Western Red Spring Wheat futures product specifications will reflect the unique growing season of spring wheat, with the September contract representing new-crop delivery (while July will represent new-crop delivery for winter wheat contracts). The futures product specifications will represent the high quality of the underlying supply; Canadian Western Red Spring wheat FOB Port of Vancouver is based on a 13.5% protein content.

The year 2022 has been a volatile one for wheat so far. The war in Ukraine and adverse North American weather conditions have resulted in substantial upward price movements in both domestic and international wheat markets. And if U.S. and Canadian dryness continue, supply could continue to tighten. Meanwhile, exogenous inflationary pressures add yet another layer of uncertainty, further contributing to the industry’s need for a way to manage regionally-specific risk.

Read more articles like this at OpenMarkets