Anne Krema and Emily Balsamo, CME Group

AT A GLANCE

- Differences in supply and demand of hogs and pork are influenced by seasonality, the hog production cycle and other factors

- The spread between Lean Hog and Pork Cutout indices is traditionally largest in November and December due to greater hog supplies and increased demand for pork products

Put another way, farmers looking to sell hogs and packers looking to sell meat to restaurants and grocery stores face different pricing risks at different times.

The Pork Cutout-Lean Hog Spread

Lean Hogs and Pork Cutout futures together enable market participants to hedge their swine and pork exposure throughout the supply chain. The spread between the two products can reflect differences in supply and demand between unprocessed hogs and wholesale cuts.Pork Cutout futures settle to the CME Pork Cutout Index, which is derived from prices paid for wholesale cuts of pork, including the loin, butt, picnic, rib, ham and belly. Lean Hog futures settle to the CME Lean Hog Index, which represents the price of hogs sold from producers to meat processors in the physical market. Both products specify a contract unit of 40,000 pounds and are priced in U.S. cents per pound, with a minimum price fluctuation of $0.00025, or $10 per contract. Such commonalities between the contract specifications allow for the two products to easily be spread against one another. The CME Lean Hog and Pork Cutout Indices are calculated each weekday from data published daily by the USDA.

Learn More About Pork Cutout Futures and Options

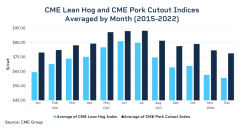

The above chart shows the Lean Hog and Pork Cutout Indices by month averaged from September 2015 to July 2022. This illustrates the seasonal trend of high summer prices due to lower processing inventory and increased demand. While both prices tend to show a seasonal decline from the summer highs through the end of the year, the decline off the highs is not as pronounced in pork as it is for hogs.

Lean Hogs and Pork Cutout are tightly correlated, though seasonal influences and differing market conditions dictate that the spread between the two varies throughout the year. The most active season for sows farrowing is June to August, according to the USDA quarterly Hogs and Pigs Report. The pigs that are born over those summer months are then market-ready by the early winter months, leading to seasonally higher hog supplies toward the end of the year.

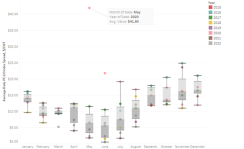

The chart below shows the difference between the Pork Cutout and the Lean Hogs Indices averaged and grouped by month, across the period from September 2015 to July 2022. The spread represents the value of processed pork relative to unprocessed hogs: the median spread is highest in November and December and lowest in the summer months. As a result of seasonal trends in farrowing, there is an abundant supply of lean hogs in the market in November and December relative to the rest of the year. This tends to drive the price down. At the same time, there are various factors that can lend strength to pork cutout prices, such as holiday demand for hams, which can ultimately lead to a higher cutout price relative to hogs.

Pork Cutout Index minus Lean Hog Index, Averaged by Month

Factors outside of regular seasonal supply and demand disrupt the expected relationship between Lean Hog and Pork Cutout futures. The mark at the top of the above chart annotates May 2020, for example, when the average daily spread was $41.85 per hundredweight, compared to a median spread of $6.39 for the month of May across the period from 2015 to2022. In May 2020, economic disruptions due to the Covid-19 Pandemic left processors with greater supply than they had the ability to process. The wide spread for this month represents oversupply of hogs relative to the value of processed meat, which was in demand from a country under pandemic lockdown.

Finally, international demand can wield strong influence over domestic hog prices. From 2012 to 2022, between 20% and 26% of pork produced in the United States was exported. Export markets differ for processed and unprocessed hogs and emerging market demand can lead to high prices, regardless of season, as seen in the commodity boom of 2008-2009 on the back of a growing appetite in the BRIC nations. In the above chart, which shows annual trends in exports of U.S. pork and variety meats between 2015 and 2022, export levels decline in the summer months and peak in the winter months. Spikes in export demand for pork can also support increases in cutout prices relative to hogs.

While historically high levels of correlation have allowed market participants with both pork and swine exposure to manage their price risk using Lean Hog futures, Pork Cutout futures now provide the industry with an additional tool to more precisely manage risk associated with price moves in the market for wholesale pork.

For more information on Livestock seasonality, see CME Group Education