Amanda Townsley, CME Group

AT A GLANCE

- Events are driving above-average swings in an already-volatile crude market

- On days when OPEC meets, the average price move for WTI Crude was $4.16, 1.4x the average

The smaller Micro WTI Crude Oil Options contracts are useful tools in this environment as they provide even more flexibility to manage adverse price movements. So is watching the calendar: days with key macroeconomic or oil-specific announcements, many which are scheduled and known in advance, drive above-average levels of price movements.

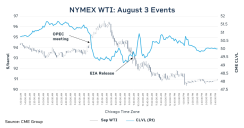

Price movement on August 3, 2022 illustrates the impact that news is having on WTI prices, which swung $6.19 per barrel on the back of two known events. In the early U.S. hours, OPEC gathered according to their predetermined schedule, and agreed on a small production increase for September: front month WTI crude oil futures rallied $2 per barrel. A few hours later, prices promptly reversed course as the weekly Energy Information Agency (EIA) data release revealed dismal gasoline demand. WTI ended the day down $3.76 per barrel.

August 3 was not an anomaly. Since March, there have been 22 releases of the EIA Weekly Petroleum Status Report – which provides a near-real-time update on U.S. stocks and implied demand. On those days, the average move in WTI price was $3.55, 1.2x that of other days. Likewise, OPEC has met six times since March to discuss production quotas, on which days the average price move was $4.16, 1.4x the average. Federal Reserve decisions, monthly inflation statistics, and portfolio rebalancing around quarter-end and at contract expiration dates also have potential for larger market moves. On average, these expected events have provided wider than normal price moves. But price response to events, even if news differs from consensus expectation, can also be unremarkable.

Unstable Environments Drive Unscheduled Volatility

Plenty of the triggers for oil price volatility are unscheduled events. The largest daily move in 2022 - $15 per barrel – came on March 9, coinciding with new headlines indicating potential compromise from Ukraine.Sometimes volatility is not event-specific. On July 5, WTI settled down $8.93 on no explicit news, but the move was attributed to a cumulative build-up of increasing recession risk – analyst reports alluding to such may have been the straw that broke the camel’s back. Periods of unstable underlying economic states or geopolitical conditions tend to create more frequent opportunities for large price moves.

Options Premiums Shrink

Despite above-average moves around recent events, implied volatility of WTI – the movement in futures prices that is implied by WTI crude oil options values – has fallen to levels not seen since February. The CLVL Index – the CME Group CVOL measure of implied volatility for WTI – hit a low of 47 on July 29, down from a Q2 average of 55 and less than half the high of 98 set in March.Read more about Micro WTI Crude Oil Options

This means options traders are pricing a fraction of the volatility from earlier in the year: options premiums are much lower. As of August 4, the premium for a call option on September WTI with a strike of $93.50 - $5 dollars above the futures price – was $1.19. On July 5, a similar $5 out-of-the-money call option cost $1.80.

CME’s CVOL measure of implied volatility for WTI (CLVL)

In March, an option with these same characteristics settled at $6.97 or more than six times the cost of buying an option in early August. While declining volatility has helped to lower the premium to hedge and trading crude oil with options, CME Group has also introduced Micro WTI options this year, which also lower the barrier to entry to hedging with options.

One fundamental factor that may be contributing to lower implied volatility is the expectation of loosening crude oil balances and a lower price of crude oil. Many market forecasters are calling for inventories to build into the end of 2022, due to a combination of rising supplies and a weaker demand outlook. Higher inventories make the market less vulnerable during a supply disruption. However, CVOL levels for Ag Products and Metals are also in decline and nearing post March lows, implicating broader macroeconomic drivers at work.

Upcoming News

In addition to the ongoing geopolitical and economic uncertainty, the Atlantic hurricane season is just getting started, with its highest concentration of storms occurring between early August and mid-October. Between NOAA’s updated forecast for an active hurricane season, low inventories, and the memory of 2021’s Hurricane Ida impact on supply, traders also need to consider how potential storms could impact price. OPEC’s next meeting is currently scheduled for September 5, the U.S. Labor Day Holiday. The Federal Reserve reconvenes to announce a rate decision on September 21. CVOL indexes such as the CLVL, are often elevated ahead of potentially market-moving events, or may react in response to surprising news as the events on August 3 show. Monitoring even short-term changes in CVOL levels can help investors and traders understand which events and periods of time are expected to bring higher volatility, and decide which futures and options products are most effective.CVOL is now streaming in real-time to CME Direct users.

Read more articles like this at OpenMarkets