By Mary-Therese Barton, Head of Emerging Market Fixed Income at Pictet Asset Management

Green appetite

Governments everywhere are racing to lock in historically low borrowing costs by issuing ever longer dated debt – in recent years Mexico and Argentina even managed to sell century bonds. That presents several new challenges for fixed income investors. Particularly those who own emerging market bonds.Not only do bondholders have to weigh the usual near-term factors like political, economic and commodity cycles, but, in lending money to sovereigns over such extended periods, they now also have to consider the impact of longer-term trends such as climate change and social development. Both can affect creditworthiness in profound ways.

This has called for new approaches to investment thinking. Economic and financial forecasts are having to be recast with climate dynamics in mind. Meanwhile, modelled pathways of climatic change are themselves subject to expectations about future technological change as well as the evolution of political thinking in these countries. The number of moving parts only grows as investors realize they also have a role to play in shaping how governments approach making their economies sustainable and low-carbon.

It’s a complex problem. But not an insurmountable one.

The greening of EM debt

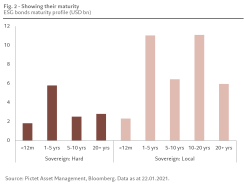

In 2015, some 17% of emerging market hard currency debt had a maturity of 20 years or more. By the start of 2021, that proportion had grown to 27%. Even local currency denominated emerging market debt, which tends to be shorter-dated, has moved along the maturity curve. Over the same time period, the proportion of local currency debt with a maturity of five years or longer had risen 11 percentage points to 58%.1That shift reflects growing demand for yield from investors starved of income. But at the same time, bondholders have recognized the importance of taking a long-term view on environmental issues. This is apparent in both the appetite for green bonds – capital earmarked for environmental- or climate-related projects – and, more generally, bonds that fall under the environmental, social and governance (ESG) umbrella.

Governments are happy to meet that demand. Increasingly, they recognize the need to make efforts to mitigate climate change and given that emerging market economies make up half the world’s output, they have a significant role to play in meeting global greenhouse gas emissions goals.

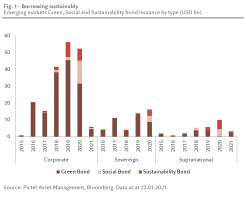

In the five years to the end of 2020, annual issuance of green, social and sustainability bonds by emerging market governments grew nearly four-fold to USD 16.2 billion.2 And demand is only increasing. For instance, in the first few weeks of January, Chile met 70% of its expected USD 6 billion debt issuance for 2021, all in green and social bonds and it plans only to issue sustainable and green bonds during the remainder of the year.3 In September 2020, Egypt became the first Middle Eastern government to issue a green bond. It raised USD 750 million to finance or refinance green projects. Investors were enthusiastic – the bond was five times oversubscribed.4

And generally, these bonds have longer maturities than conventional fixed income securities. Some 46% of USD 36.8 billion of outstanding emerging market ESG bonds priced in local currency terms have a maturity of more than 10 years, while for emerging markets hard currency ESG bonds, it’s 41% of USD 12.9 billion of outstanding bonds.5

These bonds allow investors to track performance, while green agendas can also help governments to improve their credit ratings, which then lifts the value of their debt, thus rewarding bond holders.

Overall, green bonds generate positive feedback effects. The rising volumes of green and sustainable bond issuance highlights investors' willingness to take more of a long-term approach to EM investing. But at the same time, governments are being made more accountable – in order to issue these bonds, governments are having to publish their sustainability frameworks in greater detail. This additional accountability helps to mitigate political risks that are a key consideration in EM investing. Investors, however, will need to analyze and monitor developments closely to ensure proceeds are used as intended.

Indeed, green bonds are the most exciting development in emerging market financing for decades and, we think, will have an equivalent impact to the Brady bonds of the 1980s6 – albeit this is dependent on improved disclosure and monitoring and industry standardization of green labels.

Climate change matters (especially in EM)

For all the sovereign issuance of green bonds so far, a great deal more funding will need to be raised to limit climate change. Globally it will cost between USD 1 trillion and USD 2 trillion a year in additional spending to limit global warming, some 1% to 1.5% of worldwide GDP, according to the Energy Transitions Commission.7 And a significant part of those costs will need to be borne by emerging economies, not least because they are likely to suffer most.By the end of this century, unmitigated climate change – entailing warming of 4.3° centigrade above pre-industrial levels – would cut per capita economic output in major countries like Brazil and India by more than 60% compared to a world without climate change, according to a report by Oxford University’s Smith School sponsored by Pictet Asset Management (Pictet AM).8 Globally, the shortfall would be 45%.

Limiting warming to 1.6° C would sharply reduce that hit to roughly 27% of potential output per capita for the world as a whole, albeit with considerable variation among countries. While those in tropical countries would be hit hard by the effects of drought and altered rainfall patterns, those in high latitudes, like Russia, would be relative winners as ports become less ice-locked and more territory is opened up to extractive industries and agriculture. And though China would suffer smaller overall losses than average, its large coastal conurbations would be subject to depredations caused by rising sea levels.

Integrating risks

As these effects are felt, investors will grow increasingly wary of lending to vulnerable countries. And climate change is already having an impact on developing countries’ credit ratings. In 2018, rating agency Standard & Poor’s cited hurricane risk when it cut its ratings outlook on the sovereign debt issued by the Turks and Caicos.9Investors could expect climate-related events, like droughts, severe storms, and shifts in precipitation patterns, to push up output and inflation volatility in emerging economies during the next ten to 20 years, according to Professor Cameron Hepburn, lead author of the Oxford report.

That would represent a significant reversal for emerging market sovereign borrowers. Since the turn of the century, the relative rate of growth and inflation volatilities between emerging and developed markets has halved,10 which, in turn, has reduced the risk faced by investors. Rising economic volatility would feed into sovereign risk assessments, eroding their credit profiles.

“Climate change is already having an impact on developing countries' credit rating.”

Other research from the Oxford team highlights the choices countries will need to take to remain on the path towards building a greener economy.11

At Pictet AM, we already use a wealth of ESG data – from both external and internal sources – as part of how we score countries. The environmental factors we monitor include air quality, climate change exposure, deforestation, and water stress. Social dimensions include education, healthcare, life expectancy, and scientific research. And governance covers elements like corruption, electoral process, government stability, judicial independence, and right to privacy. Together these factors are aggregated to become one of six pillars in the country risk index (CRI) ranking produced by our economics team.

Level playing fields

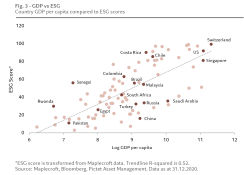

We believe that ESG considerations are inefficiently reflected in emerging market asset prices. This is a consequence of the market still being at an early stage in its understanding and application of ESG factors and analysis. There is also a lack of consistent and transparent ESG data for many emerging countries. We believe that using an ESG score alone is simply not enough. Having a sustainable lens through which to examine emerging market fundamentals helps us to mitigate risk and unearth investment opportunities. We use our own ESG data and analysis and engage with sovereign bond issuers to help bring about long-term change.Emerging market economies vary hugely in their degree of development. This complicates how investors should weigh their ESG performance – after all, richer countries are more able to make the ESG-positive policy decisions that often have high front end costs for a long tail of benefits, such as shutting down coal mines in favor of solar power.

Applying the most simplistic approach to ESG – investing on the basis of countries' ESG rankings – would squeeze fixed income investors out of the poorest developing countries, even if they are implementing the right policies to improve their ESG standing. Instead, it’s important for investors to recognize what is possible and achievable by poorer countries and allocate funding within those constraints – understanding countries’ direction of travel in terms of ESG is critical to analyzing their prospects.

One solution we are implementing at Pictet AM is to weigh ESG criteria against a country’s GDP per capita. So, for example, under our new scoring system, Angola does well on this adjusted basis despite having a low overall ranking. And the reverse is true for Gulf Cooperation Council member states.

Dynamic approaches

How governments react to long-term issues like climate change or to the challenge of developing their human capital will influence their economies’ trajectories and, ultimately, play a role in their credit ratings. Those long-term decisions are only growing in importance, not least given the scale of fiscal policies implemented in the wake of the Covid-19 pandemic. Tracking these spending programs – through, say, the likes of the Oxford Economic Stimulus Observatory12 – then becomes an important step towards understanding the ESG pathways governments are likely to follow.Countries with good, well-structured policies are likely to see their credit ratings improve, which attracts investors, drawing funding into their green investment programs and ultimately driving a virtuous investment cycle.

Engaged investors

All this implies that investors have an active role to play – they can’t just passively allocate funding based on index weightings or be purely reactive to policymakers’ decisions. The most successful investors will help steer governments towards the path that boosts their credit ratings, gives them most access to the market and improves the fortunes and potential of citizens.Like, for instance, explaining how electricity generated by wind turbines or solar can prove to be more cost-effective over the long term if financed by green bonds than ostensibly cheaper coal extracted from a mine paid for with higher yielding conventional debt. Or how fossil fuel investments could prove to be major white elephants as these sorts of polluting assets become stranded by shifts towards cleaner energy production. Or that failing to invest enough in education is a false economy that over the long run will fail to make the most of human capital and thus depress national output – something we raised with the South African government after our meetings with our on-the-ground charitable partners in the country.

To that end, The World Bank produced in 2020 a timely guide on how sovereign issuers can improve their engagement with investors on ESG issues.13

“The most successful investors will help steer governments towards the path that boosts their credit ratings.”

This sort of intensive analysis – using everything from long run macro models down to meetings with leaders of youth clubs in impoverished districts – can also help to paint a rounded picture of what’s happening in a country. For instance, it helped to ensure that we weren’t caught off guard by the shift to populism in Argentina ahead of their last elections and allowed us to trim our positions in the country.

For emerging market investors, ensuring all of these cogs mesh correctly is a difficult proposition, especially given that the parts are moving all the time, many driven by forces that will develop over many decades. But by using the full breadth of analytical tools, independent research, and shoe leather fact-finding, it’s possible to gain a deeper and more profitable insight into these markets than a simple reading of credit ratings or index weightings offers. And, at the same time, influence policy makers to champion their country’s sustainable initiatives. Taking a sustainable approach to growth and issuing related bonds, emerging economies can fundamentally change their prospects for the better. It has the potential to be revolutionary for emerging markets and exhilarating for those of us who invest in them.

Discover more about Pictet Asset Management's Emerging Markets capabilities.

1 JPM EMBI-GD and GBI-EM. Data as at 25.01.21.

2 Ibid

3 https://www.latinfinance.com/daily-briefs/2021/1/22/interview-chile-diversifies-investor-base-with-esg-bonds

4 https://www.reuters.com/article/egypt-bonds-int-idUSKBN26K1MJ

5 Source: Pictet Asset Management, Bloomberg. Data as at 25.01.21

6 Brady bonds were an innovative debt reduction program in response to the Latin American debt crisis of the 1980s, involving the issuance of US dollar denominated bonds.

7 https://www.reuters.com/article/uk-energy-transition/global-net-zero-emissions-goal-would-require-1-2-trillion-a-year-investment-study-idUKKBN2670OA?edition-redirect=in

8 Hepburn, C. et al. “Climate Change and Emerging Markets after Covid-19.” November, 2020. Estimates based on the Intergovernmental Panel on Climate Change’s shared socioeconomic pathway 2 (SSP2) using cmip5 climate models.

9 https://www.spglobal.com/marketintelligence/en/news-insights/trending/vep0j9mtowo52rlsmmww9g2#:~:text=S%26P%20Global%20Ratings%20revised%20its,two%20major20major%20hurricanes%20last%20year.&text=S%26P%20expects%20real%20GDP%20to,average%20from%202019%20to%202021

10 Average of rolling 2-year standard deviation of growth and inflation rates for 27 EM countries relative to 25 DM countries. Source: Pictet Asset Management, CEIC, Refinitiv. Data 01.01.2000 to 01.01.2021.

11 https://www.researchgate.net/publication/340509193_Economic_complexity_

and_the_green_economy

12 https://www.ouerp.com/totaltracking

13 https://www.worldbank.org/en/news/press-release/2020/11/08/world-bank-releases-guide-for-sovereign-issuers-to-engage-with-investors-on-environmental-social-and-governance-esg-issues

Disclaimer

Marketing CommunicationMarketing material for investment professionals only. The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell, or subscribe to any securities or financial instruments. Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional. The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested. Past performance is not a guide to future performance.