Blu Putnam, CME Group

AT A GLANCE

- The last time the Fed had a neutral interest rate policy was in 2018

- In August, U.S. inflation eased slightly to 8.3%, down from 9.1% in June

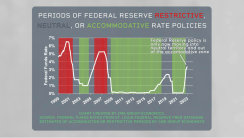

- Federal Reserve policy is only just now moving into “neutral” territory and out of the accommodative zone.

The Fed has been raising short-term interest rates from near zero during 2022, with guidance that more hikes are to come. Should we call this a “tightening” of monetary policy? No, not really, at least not yet. It’s better to refer to what is happening in 2022 as a withdrawal of accommodation that helped create the inflation we are experiencing.

The Fed has not yet pushed short-term rates into what most economists would deem as “neutral” territory. The definition of “neutral” monetary policy is a little slippery. The “neutral” rate is thought to reside at a level that equals or slightly exceeds longer-term inflation expectations. With long-term inflation expectation probably in the 3% territory, the Fed would not get to “neutral” until short-term rates were raised to more like 3.5% or so.

A “neutral” interest rate policy would typically mean that policy is neither accommodative nor restrictive in terms of its influence on economic activity. By analogy, the Fed is taking its foot off the accelerator, but it has not yet hit the brakes. This is best described as a withdrawal of the accommodation that helped to create inflation, rather than a tightening that would send the economy into a recession.

Recession risks rise only when the Fed hits the brakes, and that may or may not happen in 2023. In the fall of 2022, the Fed is just putting the car in “neutral.” Only time will tell if the Fed decides to hit the brakes in 2023 and push short-term interest rates up into the 4% or 5% territory, raising recession risks.