Private credit will create an interesting set of winners and losers in private debt markets. Borrowers will have a more difficult time due to an increasingly challenging macroeconomic environment, but such a landscape might provide private debt managers with more bargaining power than in years past.

Difficulty for some, advantage for others and overall resilience

2022 was a difficult year for private credit borrowers. A series of historic interest rate hikes, unrelenting inflation and geopolitical tensions have all contributed to significant headwinds for those looking to borrow in the private credit space. This led to higher competition for deals, lenders deploying loans with fewer stipulations in order to secure business and tight spreads to public debt.

Despite this, investors continued making investments and renewing with their managers given the lackluster yields available elsewhere. The private lending space in fact has shown signs of resilience, and how it is built for supplying corporate borrowers with needed finance in rising rate and turbulent market conditions.

As we move further into 2023, the private debt picture looks different, and shows signs of resilience if not for borrowers needing to hang tight perhaps for a couple quarters more. An important shift, 2023 thus far has shown that lenders have greater influence in securing stronger loan covenants than years past. When money was easy and competition high, private lenders had less power in negotiating terms of their loans. This led to loans with fewer restrictions and newer, less-experienced market entrants. Now, a reversal is underway and lenders are able to secure better terms.

Adding another layer to lender strength was the tremendous pullback in traditional bank middle market liquidity. Major banks saw around $40 billion of incomplete deals on their balance sheets in 2022, and the meltdown of Silicon Valley Bank made middle market lenders even more skittish.

This has created the ideal mix of factors that gives the upper hand back to private lenders. Smaller delayed draw term loans, maintenance requirements and enhanced call protections are now back in a lender’s loan arsenal.

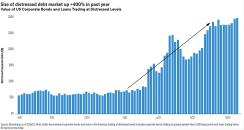

Low default risk

Private debt has seen markdowns, as the private markets lag public market markdowns in valuations, but overall the asset class remains healthy and outside of default territory. Interest coverage ratios sit well-above 1.0x, indicating a significant fallback cushion to avoid a default should rates rise further and EBITDA ratios decline.

Managers can emphasize the value-add

One flaw in the private credit space made obvious during recent turbulent markets is the need for highly-skilled management teams in the event of worsening macro conditions and increased risk of default. A considerable amount of private debt investments were made during favorable market conditions without realistic downturn scenarios built in. Higher competition led to lax covenant deals and high demand led to inexperienced market entrants.

Now with the risk of recession looming in a very real way, it highlights the need for experienced managers to mitigate the possible fallout.

Previous high yield default cycles peaked at 12 percent on average following recessions1, which means underwriting discipline is a non-negotiable in the face of potential recession. Importantly though, market downturns also provide experienced private debt managers with an immeasurable opportunity.

Should defaults rise and the economy enter a recessionary period (be it light or longer-lived) clients will rush to skilled and experienced managers to get deals done or add them to deals in an attempt to save poorly-pieced-together loans agreed upon in easier money times. Direct lending funds with experienced personnel to work out these problems that also maintain high recovery rates will be able to better weather the credit storm, but will also re-position the value-add that many active managers combat.

This puts managers in a position to demonstrate true value-add to their clients and future loan agreements. Perhaps this period of stressed private credit borrowing will prove to clients that experienced, well-structured loans with fair covenants will benefit them longer-term, and the most efficient use of that relationship is with an experienced lending manager.

There is opportunity in “good company, bad balance sheet”

Overall market instability has stressed a number of companies that made some mismatched investments during easier monetary periods. Special situation investing is a strategy pursued by some investors seeking to profit from distressed or urgent needs of financing in order to stay afloat. The special situations investor expects to eventually profit from the loan as the underlying company rebounds following financial help.

Today, higher costs of capital and stricter financial conditions have the potential to stress good value companies. Good businesses that perhaps made a mistake or were already in a tenuous position that simply needed minimal financing to recover were especially exposed during the last year.

This presents an interesting opportunity for special situation investors. There are numerous companies on the market today that go by the old adage “good company, bad balance sheet” that are ripe for private credit market investors. These companies hold fundamental value but might have accounting errors or a couple of bad investments on their hands. The problems might be easily remedied with an infusion of capital, but the company itself isn’t able to rebound on their own. Oftentimes, the situation is as simple as improving cash flows or reducing leverage.

Further, the risk/reward in this market can provide special situation investors with portfolios of uncorrelated investments that at their core might present good value but due to market conditions are trading at a deep discount. The best investments in this category will be companies poised to perform during recessionary and inflationary periods and were successful before, but happened to fall victim to the same turbulence others did over the past 18 months. These investments will allow for lower prices and attachment points, potentially leading to greater margin for the private debt investor who chooses them wisely.

The private credit markets are in a transformational period, but overall remain robust enough to survive the evolution of the next anticipated market downturn/recessionary period. Investor interest is still strong, and lending managers are able to simultaneously have the upper hand in negotiations and demonstrate much needed value propositions as investors look to navigate default risks and high interest rates.

1 Based on S&P speculative grade index historical default rates and NBER recessions going back to 1982.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance.

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested.

An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. An investment in such securities or vehicles which invest in them, should be viewed as illiquid and may require a long-term commitment with no certainty of return. The value of and return on such investments will vary due to, among other things, changes in market rates of interest, general economic conditions, economic conditions in particular industries, the condition of financial markets and the financial condition of the issuers of the investments. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor's ability to dispose of them at a favorable time or price. The value of most bond funds and credit instruments are impacted by changes in interest rates; bond prices generally move in the opposite direction of interest rates. Investing in lower-rated or high yield debt securities (“junk bonds”) involve greater credit risk, including the possibility of default, which could result in loss of principal – a risk that may be heightened in a slowing economy. Investments in derivatives involve costs and create economic leverage, which may result in significant volatility and cause the fund to participate in losses (as well as gains) that significantly exceed the fund’s initial investment in such derivative. Reduced liquidity will have an adverse impact on such securities’ value and on a portfolio’s ability to sell such securities when necessary to meet the portfolio’s liquidity needs or in response to a specific market event. Diversification does not guarantee a profit or protect against a loss.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.