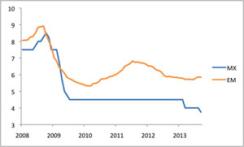

While it did not come as a total shock, Banco de México’s (Banxico) September 6 rate cut nonetheless went against consensus expectation as well as market pricing. Banxico has reduced rates twice this year, with this 25-basis-point move following a 50-basis-point reduction in the policy rate in March, as Chart 1 shows. The easing has responded primarily to cyclical considerations, but in a more structural sense it also illustrates a reduced “fear of floating.”

Chart 1: Policy Interest Rates, Mexico and Emerging Market Aggregate (%)

The Mexican peso has come under significant depreciation pressure over the past few months, and until recently Banxico would have been reluctant to risk adding fuel to the fire by cutting local interest rates. The authorities, however, have grown more comfortable with true exchange rate flexibility, a development echoed elsewhere in the emerging markets.

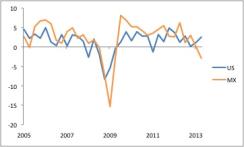

The cyclical argument for easing became more obvious with the publication of second-quarter GDP figures. The Mexican economy shrank outright in the second quarter, with GDP contracting 2.9 percent from quarter to quarter, on a seasonally adjusted annual rate. That decline followed only a marginal increase in the first quarter of 2013 of 0.1 percent. Even compared with the U.S., Mexican growth has disappointed recently. After a more intense down-and-up move during the recession and its aftermath, Mexico outperformed the U.S. through late 2011. Since then, as seen in Chart 2, Mexican growth has slowed, and its average pace over the past eight quarters has only matched that of the U.S.

Chart 2: Mexico and U.S. Real GDP (% q/q, saar)

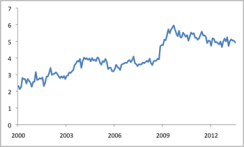

This disappointing growth trajectory appears to have left the economy with considerable slack. As Chart 3 shows, the unemployment rate in seasonally adjusted terms has been hovering around 5 percent all year (4.9 percent in July, the most recent reading), about 1.5 percentage points above the prerecession norm.

Chart 3: Mexico Unemployment Rate (% of labor force, sa)

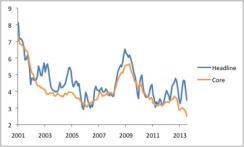

Inflation has correspondingly slowed significantly. Until December 2012, core inflation had never run below the 3 percent midpoint of Banxico’s inflation target. It has now spent seven of the past eight months below that mark, hitting a record low of 2.5 percent in July. Data for the first half of August showed further improvement (see in Chart 4).

Chart 4: Mexico Consumer Prices (% y/y)

Recent survey data indicate reduced inflation expectations. As a result, the implied ex ante real policy interest rate has been moving upward, an undesired development given the economy’s cyclical position.

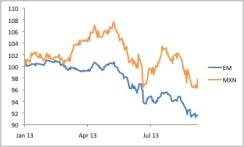

Banxico has thus been looking at a fairly impressive list of factors to justify easier policy: growth at least temporarily in negative territory; plenty of slack in the economy; and core inflation below the target, reinforced by stable-to-declining expectations. Recent market developments, however, have created a possible disruption. The Mexican peso had been under depreciation pressure since early August. While not particularly large even by recent standards, that move came on top of weakness in May and June. By September 5, the dollar had gained more than 10 percent against the peso, and the currency was showing no clear sign of stabilization. As shown in Chart 5, having been something of a darling earlier in the year, the peso was hit harder than the emerging-markets foreign exchange aggregate during the recent Federal Reserve–motivated sell-off.

Chart 5: MXN and EM FX Index (Jan. 1, 2013 = 100)

Emerging-markets policymakers have traditionally defended their currencies against sudden and significant weakness for two reasons. First, heavy external indebtedness meant that forex depreciation created balance-sheet shocks that damaged creditworthiness, especially when the sovereign itself was the hard-currency borrower. Second, limited central bank credibility generated a strong pass-through from forex moves to inflation. While the peso’s recent depreciation did not reach the point that might have once prompted a rate hike from Banxico, its move until recently would very likely have dissuaded the monetary authority from easing. After all, emerging-markets currency weakness since May has come largely as a result of higher U.S. interest rates, and further reducing the carry might be expected to generate additional depreciation pressure.

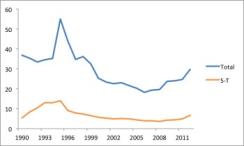

But conditions have changed, for two reasons. First, Mexico’s external balance sheet has improved. Both total and short-term external debt ratios stand below levels observed, for example, in the mid-1990s (when the peso’s devaluation nearly resulted in sovereign default; see Chart 6). Although external liabilities have risen in the past year, this mostly reflects diffuse private-sector borrowing. Forex losses thus do not concentrate themselves on one or a small number of debtors and are much easier for the economy to absorb. Second, Banxico has gained credibility over time. Its constant reiteration of the inflation target, along with its reluctance to ease during recent cyclical weak patches, has anchored inflation expectations more firmly than in the past. Temporary shocks to headline inflation have quickly mean-reverted as core inflation has moved lower. Under these circumstances, and considering the economy’s significant slack, forex pass-through should pose less of a threat. Stronger credibility thus gives Banxico more room to maneuver in dealing with cyclical weakness and allows the currency to serve as more of an equilibrating mechanism: It can depreciate freely when external conditions worsen, boosting competitiveness without resulting in a financial shock.

Chart 6: Mexico External Debt (% of GDP)

Reduced fear of floating appears to characterize emerging markets as a group, not just Mexico. As Chart 1 suggests, the recent spell of currency weakness has not prompted across-the-board rate hikes. Indonesia has raised its policy interest rate, and central banks in India and Turkey have squeezed liquidity to force short-term market rates significantly higher. These cases, however, represent exceptions. In other emerging economies, even where currencies have depreciated significantly, policymakers have stood pat. And international reserve data suggest that many central banks have engaged in less forex-market intervention than in the past.

If fear of floating is truly fading, the availability of greater exchange rate flexibility will represent a significant long-term benefit for emerging-markets economies, helping to smooth business cycle fluctuations without adding to the risk of financial shocks.

Michael Hood is a market strategist for J.P. Morgan Asset Management.

Read more about foreign exchange. Get more from J.P. Morgan Asset Management.