Amid growing concern about political risk and economic growth, it has been another tough start to the year for emerging-markets equities. But we believe the seeds have been sown for a recovery that can best be captured through a selective investing approach that avoids the risks of a benchmark.

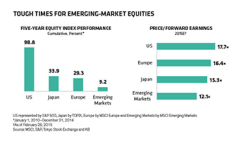

Emerging-markets equities have struggled. For the five years leading up to 2014, emerging-markets equities underperformed their developed-market peers by a wide margin, leaving valuations very low (see chart 1; click to enlarge).

Should investors stay away? Not just yet. There are still plenty of good reasons to have an allocation to emerging-markets equities. For example, the strong U.S. dollar and low oil prices are likely to fuel earnings profitability. Weakness in several key emerging currencies — including the Brazilian real, South African rand and Turkish lira — makes many developing-markets companies look more competitive. And China is the world’s largest net importer of petroleum and other liquid fuels, so cheaper oil will be a godsend for its burdened economy. Many other developing economies, including India and South Korea, are also net oil importers and will benefit from lower energy costs too.Global liquidity could also help. Money pumped into markets by the European Central Bank and the Bank of Japan could help mitigate the impact on emerging-markets stocks of a potential Federal Reserve rate hike.

So what could be a catalyst for rerating cheap emerging-markets stocks? In our view at AllianceBernstein, a pickup in Europe combined with a sustained recovery in the U.S. could lead to a revival in emerging-markets demand — and an earnings recovery from very low consensus estimates, currently at 4 percent for 2015. In this environment, we think, investors who can identify companies with specific advantages are likely to be rewarded. Examples include IT firms in India, textile manufacturers in China and Taiwan and food companies in Mexico that export to the U.S., all of which should benefit from the present favorable currency conditions.

But even in an earnings recovery, we don’t expect a return to double-digit market growth. Many things have changed in recent years that make a repeat of the explosive equity gains in emerging markets unlikely. We think that, as a result, buying the benchmark isn’t the right way to go. In fact, the emerging-markets index doesn’t have a great track record versus active managers. Last year the MSCI Emerging Markets benchmark ranked in the 69th percentile of active managers. It hasn’t done much better for much of the past decade. In other words, a median-performing emerging-markets manager would have consistently beaten the benchmark over the past ten years (see chart 2; click to enlarge).

Benchmarks are likely to be especially vulnerable, in our view. Political risk is rising in Brazil, Russia and Turkey, whereas China is facing a deceleration in economic growth. Passive exposure to emerging markets will force investors to take big positions in regions facing significant headwinds.

Active management offers distinct benefits. Emerging markets are still much more inefficient than developed markets, so there’s fertile ground for finding stock-specific opportunities that can beat the market. By staying active, the messiest parts of emerging markets can be avoided. And by taking a selective approach focused on developing high conviction in individual stocks, balanced by risk management, we believe investors can prepare for a potential recovery and beat the emerging-markets benchmark blues.

Sammy Suzuki is portfolio manager for emerging-markets core equities and the director of research for emerging-markets value equities, and Morgan Harting is an emerging-markets portfolio manager, both at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.