Economic Overview – Cautiously Optimistic

The first half of 2023 was a whipsaw of economic and real estate data that turned from gloomy to bright and back again. As the fog lifts, the case for a soft landing has become clearer. The most notable change over the past few months has been meaningful progress on inflation, which seems to be moderating, down considerably from its 8.9% peak last year to around 3% where it currently stands.

Consumers and businesses are beginning to show signs of optimism in the face of decreasing inflation and resilient labor markets. The Conference Board’s consumer confidence index has exhibited steady, if bumpy, improvement over the year. Additionally, both the second and third quarter GDP reports showed healthy growth in business investment, an indication that businesses feel better about the near-term future.

Despite these encouraging markers, not all data over the past several months has been positive. Fitch downgraded the U.S. federal government’s AAA credit rating to AA+ in August, citing concerns over fiscal governance and rising deficits. The resumption of student loan payments in October could begin to create an economic headwind which could weigh on consumer spending and thus, real estate demand in early 2024.

Data showing increasing credit card usage and receding checking account balances also point to possible weakening household solvency. Lastly, interest rates across the economy remain near the highest level on record after a series of rate hikes this year, and financing costs will likely be a drag to growth in the near term.

Similar to the economic outlook, real estate capital market conditions remain challenged, but we believe the market is beginning to show some bright spots.

Capital Market Conditions

Early signals in the real estate capital markets suggest that transaction activity is poised to recover. The wide bid-ask spreads that have driven transaction volumes back to COVID-19-era lows are partially a result of monetary policy uncertainty. Recent month-to-month data show that monetary policy uncertainty might be peaking. According to a forecast by MetLife Investment Management (MIM), the Fed has completed its rate hike cycle. MIM expects the 10-year Treasury to end 2023 in the 4% range, and to remain near or slightly below that level through the end of 2024. Stability in the rate environment has the potential to drive transaction volume back up. This view is generally in line with market consensus.

The often-illiquid office sector is also beginning to see capital markets improvement as buyers and sellers tighten the bid-ask spread and the numbers of trades modestly grows.1 This is evidenced by the amount of time office assets for sale are sitting on the market, which peaked in late 2021, and has been slowly but steadily improving.2 Lastly, MIM believes that real estate equity is offering fair-to-attractive relative value in the spot market. This, coupled with recovering public markets that have helped heal the denominator effect on commercial real estate, should continue to draw in investors to the sector in our view.

Filling Up the Capital Stack

Spreads for higher-yielding debt and preferred equity have widened this year, mainly as a result of declining property values, stress in the banking sector, and sustained weak fundamentals in the office sector. However, in our view these pressures have created opportunities for investors.

Decreasing property values have made it increasingly difficult for borrowers to source new loans or refinance at maturity from traditional lending sources, leading borrowers to seek other sources of capital. The extent to which this is occurring leaves opportunity for higher-yielding debt and preferred equity investing.

Stress in the banking sector, we believe has also created opportunity. The combination of real estate market turmoil and interest rate-related banking stress has caused regulators and bank executives to increase capital reserves, sidelining banks. Lastly, many lenders remain reluctant to increase exposure to stressed real estate segments like the office sector, retail, and more complex property types like hotels. As a result, these property types are likely facing a liquidity gap, pushing up yields even for senior first-lien mortgages.

Sector Outlooks

Fundamentals in general remain healthy outside of the office sector, which could see vacancies rise further next year.

- Apartments: The apartment sector is being impacted by a large influx of new supply, though healthy consumers and a still-tight for-sale housing market has kept rent growth positive for the year thus far in 2023. Larger-format rentals, including single-family rentals, manufactured housing, and apartments with a greater concentration of 2-and 3-bedroom units are of particular interest as trends like hybrid work stick around.

- Retail: Despite high-profile retail bankruptcies in 2023, store openings are handily outpacing store closings. This may be due to a combination of healthy consumer spending and an increase in demand for discounters and off-price stores that are e-commerce resilient. A combination of accelerating demolitions and a declining supply pipeline coupled with positive demand conditions have helped to balance fundamentals in the sector, driving retail vacancy to the lowest level on record.

- Industrial: After a two-year streak of robust fundamentals, the sector shows signs of moderating. Industrial is being affected by a simultaneous moderation in demand back to normal levels and a large supply pipeline. Fallout from inflation, higher interest rates and the regional banking crisis are also pushing up construction costs and causing supply growth to moderate. Still, despite moderating fundamentals, vacancy remains well below its historical average, which should continue to drive healthy income growth for industrial in the near term in our view.

- Offices: The office sector posted another period of negative net-leased space despite positive office-using employment growth last quarter; although, as has been the case for the past two years, lower-quality assets accounted for the bulk of weakening demand. A number of Fortune 500 firms have enacted forceful return-to-work policies, and MIM believes investors should consider the possibility that weak office leasing is now more a function of an uncertain economic outlook rather than downsizing due to remote working.

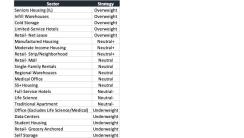

- Alternatives: According to a report by MIM and as seen in Figure 1, favorable opportunities may exist in infill industrial, limited-service hotels and residential alternatives (seniors housing, manufactured housing and moderate-income housing.)

Figure 1 | Property Type Overweight / Underweight Guidance

Source: MIM

Source: MIM

Conclusion

Despite the risks, the real estate market presents opportunities for well-capitalized investors in our view. In the office sector, negativity around the overall outlook may be peaking, which could mean spot-market prices are near a trough. In the residential sector, larger-format rentals continue to outperform. Retail and industrial are experiencing healthy fundamentals at the same time – which has not happened in over a decade. Real estate capital markets remain challenged, but we believe unlevered equity assets are offering favorable relative value. Debt markets remain dislocated as a result of a pullback from banks, which is creating strong opportunities for senior mortgage, mezzanine, and preferred equity investors, in our view.

1 NCREIF, RCA. 3Q 2023.

2 CoStar. December 2023.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

Examples described herein are intended to help illustrate certain investment concepts/processes and is not intended to represent actual past, or expected future, performance of any security, investment product or investment strategy.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission (SEC) registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

In the U.K. this document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the U.K. Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the U.K. This document is only intended for, and may only be distributed to, investors in the U.K. and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the U.K.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.

For Investors in Hong Kong SAR: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (CthI) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/ third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC, MetLife Investment Management Europe Limited, Affirmative Investment Management Partners Limited and Raven Capital Management LLC.

L1223037097[exp1225][Global]