Few should feel sorry for asset managers, whose profit margins continue to hover at about 40 percent. But the traditional drivers that have fueled growth for at least three decades aren’t working anymore, and that is leaving the industry rethinking the range of products it offers, its relationships with clients and its cost structure. Total assets under management overseen by firms in the II300, Institutional Investor’s annual ranking of the U.S.’s top money managers, were little changed in 2015, rising a scant 0.39 percent year over year, to $45.3 trillion.

To view the full list, click on America’s Top 300 Money Managers in the navigation table at right. Subscribers can access additional data, including regional rankings and details on the firms’ portfolio mixes.

J.P. Morgan’s Kenneth Worthington, the top-ranked analyst in Brokers, Asset Managers & Exchanges on II’s All-America Research Team for two years running, points to a number of factors weighing on firms. U.S. equity markets haven’t been strong since 2013, he notes, and their performance has been well below levels that investors had come to expect before the financial crisis of 2008. Conditions outside the U.S. have been even worse.

“A big source of growth that asset managers have become dependent on hasn’t been working for them,” the New York–based researcher explains. He also singles out deteriorating organic growth. Before the technology bubble burst in 2000, money management firms expanded via increased sales and improved productivity at a rate of 8 to 9 percent per annum. After 2000 the rate slowed to 6 percent — and these days it’s down to about 1 percent. “Even that 1 percent is not evenly distributed,” he observes. “Passive management is growing and active investing is shrinking.”

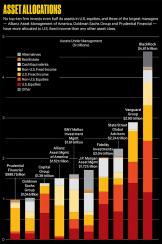

New York–based BlackRock, which operates the mostly passively managed iShares exchange-traded fund family, secures the top spot on the II300 for a seventh consecutive year, with roughly $4.6 trillion in assets — down slightly from its total the year before. Vanguard Group of Malvern, Pennsylvania, repeats in second place, with $2.9 trillion. It is also the year’s biggest gainer, having grown its AUM by more than $187 billion, or roughly 6.9 percent.

Kevin Jestice, head of institutional investor services at Vanguard, says inflows have benefited the firm broadly, including in its ETFs and target-date funds, which use index strategies. In addition, the firm has continued to grow internationally and on the institutional side of the business. “Who doesn’t want high-quality service at a competitive price,” Jestice quips.

Investors have been focused on paying reasonable fees for a number of years, but low expected returns are adding even more urgency to their concerns. Northern Trust Asset Management in Chicago thinks its factor-focused approach will be a big draw. These techniques — sometimes called smart or strategic beta — are rules-based and use systematic methods to get exposure to stock styles like value or growth or characteristics such as quality. Fees are generally a fraction of what an active fund would charge.

Bob Browne, CIO, says when investors expect returns between 5 and 6 percent — Northern’s own forecasts — it’s hard to justify a fee of 1 percent, or 20 percent of the total gain. Northern Trust has been an early mover in factor-based investing, which totals approximately $15 billion and includes the FlexShares ETF line. Browne says the firm is pouring resources into the effort and is hoping its established track record will differentiate it from an increasing number of competitors.

“Asset management will go through material changes,” he says. “Lots of traditional players who have had success in traditional active management will face challenges.”

He knows whereof he speaks. Northern Trust slips two rungs on the roster, to No. 13, with $875.3 billion (down from $934.1 billion), in part because investors withdrew money from actively managed funds.

“An asset manager with a three- to five-year track record, which we have, will monetize its efforts in factor-based investments over the next three years,” Browne believes. When performance records for active funds eventually turn around, he adds, asset managers will be confronting a potentially smaller pool of money as clients will have moved on to passive and factor-based strategies. “There will still be active funds, but there won’t be a place for mediocrity anymore,” he contends. “The rewards will go to a small number of players.”

It’s no surprise that investors are increasingly looking to manage volatility given the overall market environment. Lori Heinel, chief portfolio strategist at State Street Global Advisors, the asset management arm of Boston’s State Street Corp., says SSGA is seeing a significant uptick in institutional investors wanting to incorporate tactics in their portfolios to soften the effects of volatility. These efforts dovetail with smart beta strategies, which are also growing at the firm, she reports.

“In aggregate, the duration of your portfolio may be too long, or you may have exposure to regions or markets you don’t like,” Heinel says. “You might want to just hedge bad outcomes with a simple inflation or market hedge.”

Institutional and retail investors, through ETF model portfolios and target-date funds, are also increasingly hiring SSGA for custom work such as implementing completion strategies, she adds. SSGA will analyze a portfolio to determine factors that may be over- or underrepresented and then employs a realignment strategy.

SSGA retains the No. 3 spot on the II300 even though its AUM total declines by some $203 billion, to $2.2 trillion. Among other issues, it has been hit by redemptions from Middle Eastern sovereign wealth funds pulling money to support their economies after the price of oil fell last year.

Whereas institutional investors once hired dozens of small boutique managers that specialized in particular styles, now many of them are gravitating toward firms that offer an array of fund options, deep research and can handle the rising cost burden of providing robust systems. Fidelity Investments, whose $2 trillion in assets puts it at No. 4 again this year, has been a beneficiary of money managers’ favoring big brand names.

“More pension plans are asking, ‘How do we put our challenges and burdens on you?’” notes Derek Young, president of global asset allocation at Fidelity Investments in Boston. “They want to include us in their strategic thinking and help them solve their problems, whether for income or [liability-driven investments].”

This may be a sign of coming consolidation in the industry. “There’s too much capacity in the system, and it’s limiting the growth of the major players,” according to J.P. Morgan’s Worthington. “It’s hard to generate alpha and hard to distinguish yourself from competitors.”

Follow Julie Segal on Twitter at @julie_segal.