As investors seek to add downside protection and generate alpha amid rising inflation and other market challenges, growth-oriented U.S. stocks still dominate many institutional investment strategies. But portfolio managers from Mackenzie argue that this approach may be ignoring an equity category that adds diversification and has historically offered strong gains in past economic conditions similar to those we’re seeing now: international small caps.

We asked Martin Fahey, Senior Vice President of Investment Management and Head of Mackenzie’s Europe Team, and Bryan Mattei, Vice President and portfolio manager on the firm’s Asia Team why they believe most institutional investors should consider increasing their international small cap exposure now. Fahey, lead manager for the Mackenzie International Small Cap strategy, has two decades of experience managing international small caps. He and Mattei have been managing Mackenzie’s small cap strategy for eight years.

Why do you think adding exposure to international small caps could be increasingly important for institutional investors?

Martin Fahey: Diversification is going to be more important for many U.S. investors going forward. We see many similarities between the current market and that of the late 1990s and early 2000s, when investors fell in love with tech, media, and telecom. Many U.S. investors are once again over indexed in U.S. stocks – and particularly growth stocks, which have led the charge. In a period of higher inflation and higher bond yields, we think it generally makes sense to increase exposure to international assets – because they’ve historically outperformed U.S. assets in these periods.Bryan Mattei: Institutional investors need to realize that if they’re overweight in the U.S., it means they’re likely overweight growth. From a market composition perspective, the U.S. is much more growth-oriented than international markets. Growth industries such as technology, communication services, and healthcare are much larger components of the U.S. market than they are of European and Asia Pacific markets. In a rising interest rate environment, we think that will lead to multiple compression – with growth companies obviously more at risk because of their higher multiples.

Secondly, most institutional investors are under exposed to international small caps, as they tend to get most of their international exposure through global managers who are typically large-cap biased.

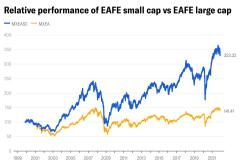

It is important to note that generally, over the long term, international small caps have significantly outperformed international large caps. We don’t see this in the U.S., however, where the Russell has lagged the S&P because of the tech giants. But countries like Japan and Europe don’t have as much exposure to FAANG-type stocks. International small capitalization stocks have substantially outperformed International large capitalization stocks over the long term.

Source: Bloomberg

What benefits do international small caps offer over U.S. small caps?

Martin Fahey: International small caps are much more diversified. While U.S. small caps are predominantly exposed to the U.S. economy, international small caps are far more likely to have exposure to several markets in the world. One reason for this is quite simple: a company that’s grown out of a small economy – like Ireland, Sweden, or Hong Kong – must become international much quicker than a U.S. company to grow. And that’s exactly what we see happen, over and over. These small caps are just more likely to be international, and as a result they’re more diversified. They also have a tendency to pick up on global trends much faster than a U.S. domestic small cap company.Additionally, from a longer-term point of view, the differences between U.S. and international small caps are quite extreme in the starting point for valuations. Small caps in the U.S. tend to be much more expensive on any metric and the differentials are quite substantial.

What misconceptions do even some sophisticated investors have about international small caps?

Martin Fahey: There’s some misperception that small U.S. companies will have better financial reporting and better governance. We have a different view. First, while the U.S. obviously has high reporting standards, the developed markets we invest in – such as the UK, Japan and Scandinavia – have very high-quality reporting. Secondly, we find that corporate governance is actually stronger for small companies in these markets than it is for many U.S. companies of comparable size. For example, many U.S. companies don’t separate the function of CEO and Chairperson, which often complicates governance and potentially concentrates too much power into the hands of one individual. This tends not to be an issue in international small cap markets where there is usually a clear separation between the CEO and the Chairperson roles.What broad opportunities are you seeing now in international small caps?

Martin Fahey: Certainly, automation is a big one. The pandemic has sped up investments in automation and IT infrastructure. And energy and materials are opportunities due to the inflationary environment.Of course, we need to mention that the pandemic has created significant challenges for international small caps, just as they have for large caps across the world. Supply chain shortages and the big pickup in inflation have coincided with increases in commodity prices and a massive rise in wages, particularly in low-wage sectors. But these challenges haven’t changed the fundamentals. Our main focus remains to continually look for and find companies with strong management and excellent growth potential.

The Mackenzie International Small Cap strategy has been in existence for nearly two decades…

Martin Fahey: Our International Small Cap strategy has a track record of almost 19 years with a very experienced portfolio management team and a highly disciplined investment process. As for our objectives, in general we seek to add about 200 basis points of outperformance before fees per annum over the longer term. As of now, the total AUM of the strategy is about 1.1 billion Canadian dollars.We have a focused, bottom-up strategy for choosing stocks for the strategy, driven by a process that’s dedicated to uncovering undervalued businesses with above average management teams. Having people on the ground in both Europe and Asia is a real competitive advantage in achieving this. Finally, we’re very conscious of the risk management of the portfolio.

Can you say more about your strategy for choosing international small caps?

Martin Fahey: Our focus is to find companies that are going to be bigger in three to five years’ time. And by bigger, we mean in terms of earnings per share, free cash, or dividends, not in terms of sales, or EBITDA or EBIT – because a lot of companies can achieve that by just making acquisitions. That’s not what we’re looking for. We’re looking for those companies that are going to create shareholder value. And the best way to do that is to find those companies that are growing their free cash flow, earnings per share, dividends, or buybacks.So that’s really our focus in building our portfolio. We want companies that will be mid caps and large caps in five to ten years’ time.

Bryan Mattei: Our approach to portfolio construction is a competitive advantage. Bottom-up stock picking is extremely important, as Martin said. It’s the core of what we do. How we put those stocks into a portfolio is almost equally important. We focus on constructing portfolios that maximize exposure to our best ideas, but seek to minimize exposure to factor risk – including style risk, like growth and value.

Consistently, over 80% of our contribution to active risk comes from our stock selection – not from taking outsized country, sector, or style bets – and I particularly emphasize style bets, because right now many people are questioning the growth-value argument. I think we sleep a lot better at night, because we know our performance isn’t likely to be driven or determined by the way that plays out. Our performance has been based on how our individual ideas perform over the long term.

Mackenzie is known for having an unusually vigorous process of researching the management caliber and growth potential of the companies it’s considering for its portfolio. Can you offer more details on that process?

Martin Fahey: Sure. When we look at the valuation of companies, we’re very careful to include things that other firms might overlook. Just for one example, we look at off balance-sheet items which have historically been ignored – like pension deficits or contingent liabilities. We’re always looking for the weakest link in a particular company, not just on the operational side and in qualitative aspects, but of course also on the financial side. Obviously, if a company is over leveraged, that’s a weak link. We saw that during the pandemic when a lot of companies had to raise capital.Secondly, we focus closely on management assessment and we often spend a lot of time with the management team. We couldn’t travel to be on site during the pandemic, naturally, but we coped well with virtual meetings. Having extensive knowledge of management teams is invaluable to us.

We believe it’s extremely important to meet with management teams in person, so we resumed traveling as soon as we could to perform on-site research. We recently we sent teams to Spain and Paris, and we plan to visit a number of companies in England soon. When you combine this process with our many years of knowledge and experience in assessing companies, that’s what gives us our competitive edge.

I would think that few small-cap companies expect to get that degree of attention and scrutiny, in any market…

Bryan Mattei: Small cap companies, particularly in Asia and Europe, are very under-researched. There may be 50 analysts covering Google, reducing the potential for the company to surprise. But some of the smaller companies we research may have only one or two analysts covering them, and it’s certainly not their top priority. We are less reliant on the sell side for gathering information and staying on top of companies. This is another reason we try to do much more due diligence. The information for small caps just isn’t as publicly available and isn’t as scrutinized as it is large companies. Therein lies the opportunity.Martin Fahey: Our research process works well for both large cap and small cap companies, but for smaller caps we have to spend even more time getting to know the management teams. As Bryan said, the important information doesn’t come to you as easily as it does with larger caps. You have to go out and find it.

At the heart of it, it seems like being included in your portfolio is a strong vote of confidence in a small cap’s management team and the leadership capabilities you’ve directly observed, which goes beyond their financials…

Martin Fahey: It is. I’ve been with the greater IG Mackenzie since 1993 and managed small cap strategies for almost 20 years. We’ve kept the same core investment process for many years. We’re always looking to improve it and tweak it, but it’s the same relentless focus on performance. By focusing on keys like management compensation, the culture of the company, the separation of roles, and what they’ve delivered in the past, we aim to consistently choose companies that will create exceptional shareholder value. We have offered our investors a very stable, experienced portfolio management team, and they know that the companies we choose have strong management with good balance sheets – because we know from experience that these are the companies that are able to overcome difficult situations over time.Learn more about investment opportunities in international small caps.

This material is for marketing and informational purposes only and does not constitute an offer of investment products or services (or an invitation to make such offer). This material, including examples related to specific securities, is not intended to constitute investment advice or any form of recommendation. Investing involves risk and there can be no guarantee that any account will achieve its objectives, including any performance targets.