Contributors

Anu R. Ganti, CFA, Senior Director, Index Investment Strategy

anu.ganti@spglobal.com

Craig J. Lazzara, CFA, Managing Director, Global Head of Index Investment Strategy

craig.lazzara@spglobal.com

“Courage is reckoned the greatest of all virtues; because, unless a man has that virtue, he has no security for preserving any other.” – Samuel Johnson1

EXECUTIVE SUMMARY

Never wish to show courage, a wise man once counseled; courage can be displayed only in circumstances where one’s natural instinct is to be afraid, and fear is an unpleasant emotion. This principle, with obvious qualifications, applies to investment management. Successful portfolio management can require holding positions when one’s natural instinct is to sell.

ONCE UPON A TIME

It is Dec. 31, 1999. You are a professional portfolio manager pondering long-term stock selections for your clients. You share Warren Buffet’s view that “Our favorite holding period is forever,”2 and you decide to ask each of your four favorite Wall Street forecasters to recommend a stock to hold indefinitely. They obligingly recommend four different names, denoted for now as Stocks A through D, which you carefully consider.

You’re well aware that some recommendations work out better than others. What might cause you to lose confidence in any of these four stocks? Since you will be buying the stocks in the expectation that they will go up, and in fact will outperform the market, a period of disappointing returns might weaken your determination to hold forever.

While contemplating all this, you have been holding a very old bottle of wine that a friend gave you for your last birthday. You open the bottle, thinking that a taste might help resolve your perplexity. As you remove the cork, suddenly vapor spews out and a genie emerges. In gratitude for your having released him, he offers you a wish.

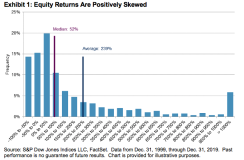

Of course, what you wish is to know which of the four stocks will be the best performer for the next 20 years. Unfortunately, our genie has been corked up with the wine for a bit too long. He knows a good bit about volatility but very little about the returns of individual stocks. The genie does know that the market will go up in the next 20 years, and that individual stock returns will be highly skewed, as Exhibit 1 illustrates. The median stock in the S&P 500® will appreciate by 52%, well below the average appreciation of 239%. Only 267 of the 1,010 stocks that will appear in the S&P 500 for the next 20 years will beat the average.3

Having been made aware that a relatively small number of stocks will determine your success or failure, you’re happy to have whatever specific information you can get, and ask the genie to tell you what he knows about the four recommendations.

IN VINO VERITAS

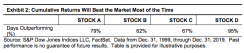

Although our genie can’t tell us which stock will be the best performer, nor indeed whether any of them will outperform the market averages, he does know something about the frequency of outperformance. Suppose we buy each stock at Dec. 31, 1999’s closing price and hold for the next 20 years. Those 20 years will encompass 5,031 trading days. On how many of those days will the cumulative return of each position exceed the cumulative return of the S&P 500? Exhibit 2 tells us the answer.

This is a great comfort to you, of course, since you realize that regardless of which stock you buy, when your clients look at their since-inception returns, they will usually see outperformance. Stock D is particularly impressive, and A also stands out.

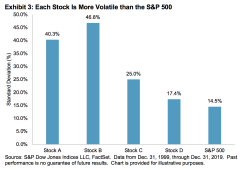

The genie next reveals the future volatility of each stock, measured simply by the standard deviation of monthly returns. This revelation is pictured in Exhibit 3.

All four will be more volatile than the S&P 500, with standard deviations ranging from 17.4% (stock D) to 46.8% (stock B).

You’re a bit nervous about the high volatility level of A and B, but of course you know that most stocks are more volatile than the market as a whole; these data don’t cause you to lose confidence in any of the forecasters.

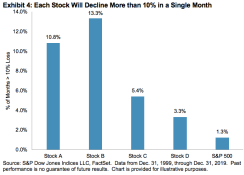

The genie next tells you about the frequency of large losses. Will any of the four stocks decline more than 10% in a single month? Exhibit 4 shows that they all will.

Stocks A and B are substantially more likely to have large one-month losses than are stocks C and D, as we might have predicted from Exhibit 3’s standard deviation data. You remain confident in the four stocks, although perhaps a little less about stocks A and (especially) B.

CUMULATIVE LOSSES

The genie reminds you that some loss periods don’t correspond neatly to a single calendar month. He then presents Exhibit 5, which shows the maximum peak-to-trough loss each of the stocks will endure.

The S&P 500 will, at some point in the next 20 years, decline by just over 50%. Stock D will be more stable than the market, while stocks A and B will experience even larger drawdowns.

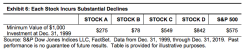

And, the genie reminds you, the drawdown story might feel even more harrowing than Exhibit 5 reveals. Suppose your clients invest $1,000 in each stock. What’s the minimum value they’ll have in each position?

The $1,000 your clients might invest in Stock A, in other words, will one day be worth only $275, as Exhibit 6 illustrates. $1,000 invested in Stock B will one day be worth only $78. Stocks C and D also experience declines, but of much less severity, which is also true for the market as a whole. Even if you’re still confident that each stock will be worth more than $1,000 over the long run, before you get to the long run there may be some difficult client meetings.

THE COURAGE OF YOUR FORECASTERS’ CONVICTIONS

Stocks A and B, by every measure, seem substantially more volatile than Stocks C and D. Knowing this, are you still willing to buy A and B for your clients? You know that stocks fluctuate, but you also remember that most stocks underperform the market over time.4

When the $1,000 you invested in Stock A is worth only $275, will you still have faith in the forecaster who recommended it? More importantly, will your clients still have faith in you? It would be entirely understandable if, at some point between $1,000 and $275, you decided that the forecaster was, if not wrong, at least no longer worth the trouble of defending.5

Knowing what you now know about the risk of the four recommendations, would you be willing to buy and hold all four names? If not, which ones would you eliminate?

20 YEARS LATER – THE NAMES REVEALED

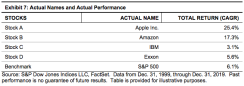

It’s now Dec. 31, 2019, 20 years after your interactions with the forecasters and the genie. It’s time to evaluate how well each of the forecasters did, and how well you would have done to have taken their advice. Exhibit 7 tells us the actual identity of the four stocks and their total return for the 20 years ended Dec. 31, 2019.

Stock A, Apple Inc., was the best performer in the S&P 500 for the 20 years in our study, and Amazon (stock B) wasn’t far behind. Stocks C and D, better known as IBM and Exxon, both underperformed the market. On every risk dimension, the two best performers were the more volatile holdings. This is important, because volatility tests an investor’s conviction—if every stock you bought always went up, you’d never wonder whether you’d made a mistake. When you’re losing money on what you thought would be a winner, doubts inevitably creep in. What Exhibit 7 and the earlier volatility evidence suggest is that sometimes the stocks you will have most wanted to own are the hardest to hold.

This psychological difficulty is compounded for professional asset managers. You might well be willing to take a flutter on A and B with your own money, but you’re also a fiduciary for your clients, and of course your firm’s compliance and risk managers will be looking over your shoulder. Even if you remain confident in A’s and B’s long-term prospects, you may also believe that convincing your clients to share that confidence is an insurmountable task. “Sometimes you sell your duds so you don’t have to talk about them anymore—to the firm’s risk manager or to your clients.”6 This is why “professional investors tend to move the fastest when a market suddenly turns…The biggest risk they face is being so out-of-step with the market that their clients fire them.”7

THE MORAL OF THE STORY

Stock selection is difficult. Data from many sources over many years have demonstrated that successful active management is rare. A number of reasons—the professionalization of investment management, high costs, etc.—help to explain the persistent failure of active management to produce positive relative returns.8 The difficulties faced by active managers, in other words, are not coincidental—they arise for good reasons, and are therefore likely to persist.

This paper’s simple example adds to our understanding of the challenges of active management. Over long horizons, most stocks underperform the market as a whole. The challenge for an active manager is not limited to identifying the relatively small number of long-term winners. Success also depends on holding on to them when they go through painful periods of underperformance. Conviction and confidence are not enough to win the day—courage is also needed, and most needed precisely when it’s hardest to muster.

Register to receive our latest research, education, and commentary.

1 See Boswell’s Life, April 5, 1775.

2 See, inter alia, https://www.brainyquote.com/quotes/warren_buffett_129835.

3 See also Bessembinder, Hendrik, “Do Stocks Outperform Treasury Bills?” May 2018. Yes, this article hadn’t been written in December 1999. You accepted the genie; why are you quibbling about a date?

4 See Ganti, Anu R. and Craig J. Lazzara, “Shooting the Messenger,” S&P Dow Jones Indices, December 2017, pp. 9-10.

5 Stock market forecasting is notoriously difficult, as any reader of our SPIVA® reports will recognize.

6 “The agonies of stock-picking in a falling market,” The Economist, March 21, 2020. Emphasis added.

7 Zwieg, Jason, “The Pros Have to Sell Stocks Now. You Don’t.,” Wall Street Journal, Feb. 26, 2020.

8 See, e.g., Ganti and Lazzara, op. cit.