It is becoming clear that the effects of the COVID-19 pandemic will reverberate long after the outbreak has passed. Our “inescapable truths” are the economic and disruptive forces identified by Schroders before COVID-19, in which we predicted a slowing economy and unprecedented disruption, and implied active stock selection and risk management would be critical.

This report, we explain how sustainability will be fundamental to understanding this shift, focusing on six key areas that point to a changing role of the corporate sector in society. The full version of this report can be found on our site.

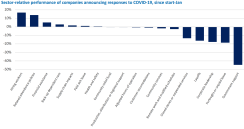

1. Re-writing social contracts: responsible “saint” companies have outperformed the “sinners”

The current consumer attention on companies’ roles in society – and the gap between “saints” and “sinners” – is likely to accelerate.

The “inescapable truths” predicted subdued growth and low inflation against a backdrop of disruption from populist politics, technology and climate change. How companies respond to an environment of considerable change will be critical, and investors will need to be more agile than ever.

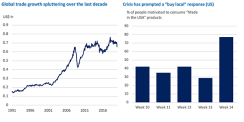

Unlike with the global financial crisis, where scrutiny was focused on the financial sphere, this crisis is prompting introspection and scrutiny of corporate behavior in general – with consumer sectors facing more scrutiny than most.

Those behaving responsibly towards their employees or redirecting capacity to social challenges to support public relief efforts have outperformed, according to our research.

We put together sector-relative returns to show the equity returns of companies taking different actions.

While performance is measured relative to sector peers to adjust for the different pressures facing each sector, we recognize that many actions may not be a direct cause of outperformance.

Source: Company announcements, JUST Capital, Schroders. Past performance is not a guide to future performance and may not be repeated.

However, the relationship between the responses to COVID-19 and the equity market’s appraisal of their value is telling. Those hiring workers, relaxing attendance policies or offering financial assistance, for example, have been appraised positively. We believe those companies with a longer-term outlook are likely to be those still standing once the crisis has passed.

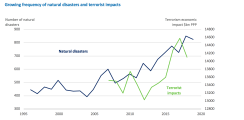

2. Companies must be better prepared for “black swan” events

Our Chief Economist and Strategist Keith Wade has observed that the economic effects of crises like pandemics can reverberate for as long as 40 years. Events such as terrorist attacks, political disruptions, natural disasters and other climate risks are coming thicker and faster, making so-called “black swan” events more frequent.

Their causes may be different, but the business effects are similar: supply chains are disrupted, movement slows and demand falters. Compounding the impact, industry supply chains have become longer, more diverse and with thinner inventory buffers.

In many cases companies will be forced to build “inefficiencies” into their supply chains and operations – some slack that has periodic value to compensate for its structural costliness. In other cases, smarter sourcing decisions and choices over where operations are located will help.

Source: Munich Re (left), Institute for Econonics and Peace (Right)

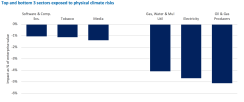

Emerging Asia and Latin America are the regions most exposed to pandemic risks, and the by sector, the next figure shows those the most exposed to physical climate risk are oil & gas producers and electricity

By combining companies’ geographic exposures with the risks each country faces, we can assess companies’ exposures to pandemic threats, physical climate risks, water stresses, and socio-political risks.

Source: Schroders 2020.

3. Political reprioritization: governments will come under pressure to tackle societal problems

The crisis will place growing pressure on governments to reverse the policies that have exacerbated growing inequalities within societies. There is clear evidence that the current crisis has hit poorer people harder than wealthier counterparts.

There are disadvantages in accessing healthcare, poorer underlying health and the need to continue working in poorly paid and badly protected jobs. On the other hand, the speed and stringency of the response in many countries underlines the capacity of governments to achieve significant social change quickly.

The crisis may prove a springboard to a round of political reform. Fiscal stimulus packages to help the economy through the crisis are already ripping up the rulebook. There is an opportunity to create stretching policy initiatives to tackle some of the worst societal problems.

Social pressure for political reform has been growing for more than a decade, particularly in developed economies. Indeed, rising populism is one of the identified “inescapable truths” of the next decade.

This crisis may provide the impetus to release that pressure through changes to political systems. Consideration of sustainability factors will be key for investors as concerns that have led to political upsets in recent years come under the spotlight. We expect health, education, employment and other welfare policies to attract more focus in the future, channelling public funds into investment opportunities in related sectors.

Those impacts are likely to be predominantly sectoral. By tracking trends in regulation across topics and sectors, we can help identify companies facing bigger risks. Companies in the publishing industry, for example, may already face greater regulatory risk than those in the pharmaceuticals and packaging sectors. We can see that the latter sectors may be ripe for regulatory change.

As investors, we can then analyse and question companies directly on their exposure and readiness for new regulatory pressures.

4. Employee protection: supporting vulnerable workers

As industries such as the restaurant and hospitality sector ground to a halt during lockdowns, job and wage security have since hit all-time lows. More than 80% of the global workforce of 3.3 billion has been affected by full or partial workplace closures. Lockdowns are expected to wipe out 6.7% of working hours globally in the second quarter of 2020, according to the International Labour Organisation. That’s equivalent to 195 million full-time workers.

Many of those job losses will be transient, but COVID-19 has highlighted gaps in employee protection that will receive continued scrutiny. An increasing number of workers are in casual or “gig” economy roles. An absence of basic benefits such as paid sick leave, healthcare or retirement provision have become major social concerns.

We expect the definition and responsibilities of employers will change as a result, as will the role of trade unions advocating on workers’ behalf.

In short, employees will have an increasingly powerful voice, particularly in industries that have historically been able to treat workers as dispensable resources to squeeze. The redistributive effects of unionisation are likely to prove increasingly important, with the share of major economies’ workforces in insecure roles rising.

We expect the crisis to drive a range of changes to industries. In particular:

Protection of contractors’ and gig workers’ rights such as via minimum or living wage rates, which are now being compounded in EU regulation likely to be paralleled globally. Companies that have already made commitments on living wages and benefits will be better placed.

Stronger employee bargaining and trade unions. Countries with higher levels of unionization have lower levels of inequality. Unions are likely to receive a boost in their already-stabilizing fortunes as policymakers’ focus on inequality rises. Countries, companies and sectors with higher union representation will likely be better placed to adapt.

Our proprietary ESG tools include a range of measures to assess companies’ readiness to adapt to the growing importance and influence of employees. Below we have ranked the most common benefits employees cite, as well as levels of satisfaction they report through popular employee review sites.

Our analysis suggests that corporates’ focus on basic benefits such as sick pay and health insurance will be increasingly critical to their licenses to operate. Companies that pay low wages will similarly face margin pressure as demands to pay sustainable incomes grow.

Workers’ satisfaction with their employers will provide an indication of the disruption companies face as the pendulum of power moves back toward employees.

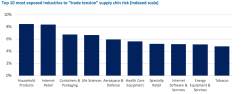

5. Globalization under pressure: long-term structural shifts in global supply chains

Supply chains have forcibly localized during the COVID-19 outbreak. Many countries have taken steps to secure domestic food supplies over exports, potentially leading to shortages in import-reliant countries. The US pharmaceutical and biotech industry has been exposed as vastly reliant on China for the majority of its key active pharmaceutical ingredients. Post-crisis, companies may begin, once again, to lean on their most trusted global partners, whatever their location. But the crisis is likely to resurface existing concerns on the over-complexity and opaqueness of global supply chains. Difficult discussions are re-emerging on trade barriers and border taxes.

Source: World Bank (left) Cognovi Labs (right)

The US-China trade tensions last year felt pivotal, but in fact accounted for less than a quarter of recent anti-trade measures.

All point towards long-term and structural shifts in global supply chains and headwinds to companies reliant on complex and diverse global value chains. Companies will need to build out their choice of suppliers, even if doing so raises costs and reduces efficiency.

Source: Schroders

Consumer products and internet retail sectors are the most exposed to existing trade tensions in the US, for example. On a company level, this allows us to analyze threats to supply chain disruption of some of our key holdings. Similarly, our assessment of supplier payment lead times shows the pharmaceutical and mining sectors among the slowest to pay their suppliers.

Companies need to have both visibility and agility in overseeing their supply chains, as well sufficient investment in technology systems to help manage their performance.

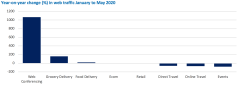

6. Technology adoption: driving workplace changes and new sales channels (but there are risks)

Digital life has been fast-tracked. The crisis has forced many corporate leaders to reprioritise remote working and to strengthen their digital tools in case of future lockdowns or other disruptions. Several new opportunities are emerging, both for growing categories such as video conferencing and for companies able to exploit the digital workplaces and channels that have quickly matured.

Businesses have become increasingly reliant on global travel to build relationships, a trend that looks threatened. Reflecting that shift, video conference provider Zoom currently has a larger market capitalization than the world’s seven largest airlines combined (as of June 2020).

The “new tech bubble” also saw a 74% rise in online purchasing during March 2020, and a rise in gaming. Consumers have spent around 65% more on video games compared to the same period last year.

Whether these new habits will last depends in a large part on security. Technology platform launches have been rushed out, causing potential shortcuts in data security protocols. Data security threats are heightened, and companies may be more vulnerable.

Source: SimilarWeb

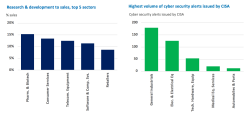

Companies with higher levels of research and development compared to their peers are likely to be at the forefront of deploying breakthrough technologies, as suggested in the blue bar figure below. Businesses taking those steps with a firm handle on data security and privacy will be at an advantage.

The volume of cyber security alerts (green bar figure) indicates the sectors most affected to date by security issues.

The different data sources available allow us to paint a risk management picture of companies across key affected industries and enable comparisons across peer groups. Companies that have invested in good data security technology and leadership will be the least exposed to fines and poor customer experiences.

Source: Refinitiv, Schroders (left) CISA (right)

Conclusion: Sustainability will be fundamental to progress

The COVID-19 crisis has been a structural whirlwind, with the potential to fundamentally transform how companies interact with their stakeholders for the better over the long term.

Through our proprietary analysis tools, we have the ability to draw upon global trend data and company data to assess which sectors and companies are likely to emerge less scathed, both from the crisis and other “black swan” events.

The COVID-19 crisis has highlighted the importance of ESG (environmental, social and governance) analysis, measurement, and engagement.

And as an active investor, we actively question those we believe are falling short of the ever-important expectations of stakeholders.

Schroder Investment Management North America Inc.

7 Bryant Park, New York, NY 10018-3706

For more information please visit our website at:

www.schroders.com/en/us/institutional/

Twitter: @SchrodersUS

Important Information: The views and opinions contained herein are those of the author and do not necessarily represent Schroder Investment Management North America Inc.’s (SIMNA Inc.) house view. Issued August 2020. These views and opinions are subject to change. Companies/issuers/sectors mentioned are for illustrative purposes only and should not be viewed as a recommendation to buy/sell. This report is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Information herein has been obtained from sources we believe to be reliable but SIMNA Inc. does not warrant its completeness or accuracy. No responsibility can be accepted for errors of facts obtained from third parties. Reliance should not be placed on the views and information in the document when making individual investment and / or strategic decisions. The opinions stated in this document include some forecasted views. We believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee that any forecasts or opinions will be realized. No responsibility can be accepted for errors of fact obtained from third parties. While every effort has been made to produce a fair representation of performance, no representations or warranties are made as to the accuracy of the information or ratings presented, and no responsibility or liability can be accepted for damage caused by use of or reliance on the information contained within this report. Past performance is no guarantee of future results.

Note that the values and references provided by the Schroders Sustainability tools herein are comprised of both qualitative and quantitative measures, and offer no guarantee of any future results. A quantitative model, such as the risk and other models used by the investment team requires adherence to a systematic, disciplined process. The team’s ability to monitor and, if necessary, adjust its quantitative model could be adversely affected by various factors including incorrect or outdated market and other data inputs. Factors that affect a security’s value can change over time, and these changes may not be reflected in the quantitative model. In addition, factors used in quantitative analysis and the weight placed on those factors may not be predictive of a security’s value. No investment strategy or technique can guarantee future outcomes or results, nor eliminate the risk of loss of principal.

SIMNA Inc. is registered as an investment adviser with the US Securities and Exchange Commission and as a Portfolio Manager with the securities regulatory authorities in Alberta, British Columbia, Manitoba, Nova Scotia, Ontario, Quebec and Saskatchewan. It provides asset management products and services to clients in the United States and Canada. Schroder Fund Advisors LLC (SFA) markets certain investment vehicles for which SIMNA Inc. is an investment adviser. SFA is a wholly-owned subsidiary of SIMNA Inc. and is registered as a limited purpose broker dealer with the Financial Industry Regulatory Authority and as an Exempt Market Dealer with the securities regulatory authorities in Alberta, British Columbia, Manitoba, New Brunswick, Nova Scotia, Ontario, Quebec, Saskatchewan, Newfoundland and Labrador. This document does not purport to provide investment advice and the information contained in this material is for informational purposes and not to engage in a trading activities. It does not purport to describe the business or affairs of any issuer and is not being provided for delivery to or review by any prospective purchaser so as to assist the prospective purchaser to make an investment decision in respect of securities being sold in a distribution. SIMNA Inc. and SFA are indirect, wholly-owned subsidiaries of Schroders plc, a UK public company with shares listed on the London Stock Exchange. Further information about Schroders can be found at www.schroders.com/us or www.schroders.com/ca. Schroder Investment Management North America Inc., 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.