Given investors’ steady appetite for alternative investments and their growing experience and comfort with ETFs, liquid alternative ETFs are emerging as a natural fit for institutional portfolios. In particular, liquid alt ETFs have the potential to help institutional investors address several vexing challenges related to alternative investments, including the frequent transitions between alternative managers and the high costs and limited transparency of fund-of-funds allocations.

Fresh Research

In a new study commissioned by IndexIQ, Greenwich Associates projects that institutional investments in liquid alternative ETFs will more than double in the next 12 months, based on feedback from 107 senior fund professionals at large U.S. institutions. One of the key conclusions drawn from this research is that liquid alt ETFs are in their very early stages in the institutional marketplace. Drawing on data on institutional demand for alternatives classes and adoption rates of ETFs in other asset classes, the paper projects a trajectory of further long-term growth for liquid alt ETFs in institutional portfolios.

Increased allocations to alternatives

Over the past decade, U.S. institutional allocations to alternative asset classes have grown from an average of 19% of total assets to 26%. Current allocations by U.S. institutions represent something on the order of $5 trillion in assets. Globally, some projections put institutional investments in alternative assets at as much as $20 trillion by 2020.

U.S. endowments and foundations have been at the forefront of alternative investing since David Swensen and Dean Takahashi developed what came to be known as the “Yale model” in the 1990s. In keeping with that tradition, among the institutions participating in the study, endowments and foundations have the largest allocations to alternatives at 29% of total assets, followed by family offices at 28%. However, the most notable number from the research might be a 26% average allocation to alternatives among public funds. With their much larger asset base and widespread underfunding issues, U.S. public pensions have become some of the most aggressive and important users of alternatives.

Use of liquid alts

Liquidity is by far the biggest reason institutions give for using liquid alternatives, with three-quarters of study participants naming it as a primary benefit. However, institutions cite a range of additional advantages as well. First, they say that by facilitating easier access to a range of alternative asset classes, liquid alts enhance portfolio diversification. Next, relative to other alternative investments, liquid alts provide an important level of transparency. Liquid alts also have attractive fee levels.

As a result of all these factors, institutions see them as having the potential to improve a portfolio’s risk/return profile. In many of these areas, liquid alts compare especially favorably to another common vehicle used by institutions for alternatives exposures – funds of funds. Of course, institutions see drawbacks as well. Institutions are concerned about the liquidity of liquid alts during periods of market stress, for example, an issue that echoes concerns raised previously about exchange traded funds generally, particularly in credit markets.

Learn more from the full report.

However, after a decade of growth in bond ETFs that has spanned periods of sometimes intense credit market volatility, many institutions have become more comfortable with the structure – as evidenced by the increasing use of ETFs by institutions in both equity and fixed-income portfolios. As institutions build a similar track record with liquid alternatives, their peers will be watching closely.

Benefits and applications of liquid alt ETFs

For the most part, institutions in the study say they’re attracted to liquid alt ETFs by the same benefits that make liquid alts appealing in general: enhanced liquidity, improved portfolio diversification and heightened transparency. However, when it comes to the liquid alt ETF, institutions are considerably more likely to cite attractive fee levels as a reason for investing. Institutions also have some of the same concerns with ETFs that they voice for liquid alt vehicles generally, including issues about liquidity in times of market stress.

Institutions currently investing or considering an allocation to liquid alt ETFs are using these vehicles for four main purposes: to assist in alternative manager transitions and other tactical adjustments; to achieve cheap beta market exposure; to replace long-term core holdings for strategic purposes; and occasionally to achieve greater tax efficiency.

Alternative Manager Transitions

The single most common application for liquid alt ETFs in institutional portfolios to date has been in alternative manager transitions. Among current users of liquid alt ETFs nearly 85% overall and more than 90% of public funds use the funds in alternative manager transitions.

At any given moment, about 5% of the typical alternatives portfolio is undergoing a manager transition. Given the complexity of these strategies and relationships, these transitions tend to be multifaceted and lengthy. As a study participant from a public fund explains, “If we’re redeeming from a hedge fund manager and looking for a replacement for them, it could take months to do our due diligence.”

Tactical Portfolio Adjustments

Institutions in the study also employ the funds widely as a means of implementing other tactical adjustments to their portfolios. That’s especially true for public funds and endowments and foundations. Study respondents from these two groups are particularly active users of liquid alt ETFs in making tactical changes to fixed-income portfolios, where the liquidity and ease-of-use make these vehicles versatile tools. Public funds are also the heaviest users of liquid alt ETFs for short-term tactical functions in equities, real estate, hedge funds, and other alternative asset classes. “Overall, we are focusing on risk/return, liquidity, and cost,” says a representative of one public fund, explaining that institution’s use of liquid alt ETFs.

Alpha/Beta Separation

In terms of specific applications, 57% of current public fund investors and half of the corporate funds are using liquid alt ETFs to obtain strategic investment exposures as part of alpha/beta separation strategies. “If you run alpha/beta separation you need pretty strong liquidity,” says a representative of a U.S. endowment/foundation, explaining his use of liquid alt ETFs. “It allows you to manage your cash more effectively if your assets are liquid as well.” ETFs can also be a cheap source of market exposure – for example, as a replacement for cash bonds.

Core Investment Exposures

A majority of institutional investment in liquid alt ETFs is used to obtain long-term investment exposures and accomplish other strategic portfolio functions. In hedge funds, real estate, and other alternative categories, more than 60% of institutions say they are more likely to employ liquid alt ETFs for a year or longer for strategic purposes. More broadly, nearly a third of current alternative ETF investors overall say they use liquid alt ETFs to obtain core long-term investment holdings.

Funds-of-Funds Replacement

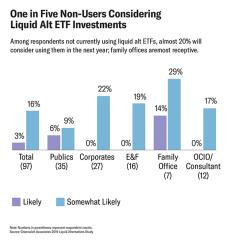

In addition to these common applications, many institutional investors are also considering the use of liquid alt ETFs in place of funds of funds. In fact, almost 1 in 5 study participants is considering replacing a portion of their funds-of-funds allocation with liquid alt ETFs in the next 12 months.

Growth Projected

Greenwich Associates has been tracking the use of ETFs in the institutional market since 2009. Over that time, it has documented a consistent pattern that has unfolded across institution type, geographic region, and asset class: Institutions start with small investments in ETFs, generally for a single, specific tactical task like a manager transition. In short order, they discover that ETFs are not only effective in these tasks, they are also incredibly flexible. Over time, institutions start adopting ETFs into a list of increasingly strategic portfolio functions. Ultimately, they are used across asset classes and portfolios as both a versatile tool for short-term adjustments and functions, and as a primary means of obtaining long-term strategic investment exposures.

In the view of Greenwich Associates, liquid alt ETFs will follow a similar trajectory and that the funds right now are only at the very beginning of this process. Almost 20% of institutions not currently investing in liquid alt ETFs say they will consider using them in the year ahead. This cohort includes large public pensions and the significant and growing number of family offices that has the potential to increase assets in the category quickly. Meanwhile, roughly 1 in 10 current investors plan to increase allocations to liquid alt ETFs in the next year. Not a single study participant plans to reduce a current allocation.

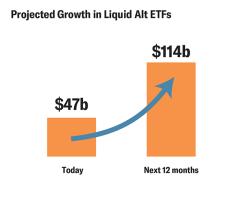

Based on these findings, Greenwich Associates projects that, over the next 12 months, institutional investment in liquid alt ETFs will climb to approximately $114 billion – roughly 2.5 times current allocations.

About risk

There are risks involved with investing in any such products, including the possible loss of principal. Investors in the Funds should be willing to accept a high degree of volatility and the possibility of significant losses.

“New York Life Investments” is both a service mark, and the common trade name, of the investment advisors affiliated with New York Life Insurance Company. IndexIQ® is an indirect wholly owned subsidiary of New York Life Investment Management Holdings LLC and serves as the advisor to the IndexIQ ETFs. ALPS Distributors, Inc. (ALPS) is the principal underwriter of the ETFs. NYLIFE Distributors LLC is a distributor of the ETFs. NYLIFE Distributors LLC is located at 30 Hudson Street, Jersey City, NJ 07302. ALPS Distributors, Inc. is not affiliated with NYLIFE Distributors LLC. NYLIFE Distributors LLC is a Member FINRA/SIPC.

Liquid alternative investments (or liquid alts) are mutual funds or exchange-traded funds (ETFs) that aim to provide investors with diversification and downside participation through exposure to alternative investment strategies.

Greenwich Associates is not affiliated with New York Life Insurance Company or any of its subsidiaries.

1837977