This blog is the first in a new series on Institutionalinvestor.com entitled Global Market Thought Leaders , a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is AllianceBernstein, who will be providing analysis and insight into equities.

Fear that inflation will raise its ugly head after a quarter century of quiescence has led many investors to reevaluate their need for inflation protection. Others, however, think their equity holdings should give them an adequate hedge against inflation.

Our research shows that diversified equity portfolios can indeed overcome the impact of inflation—but only over very long time horizons. Over the short to medium term—say three months to seven years—equities have a poor record as a hedge against accelerating inflation.

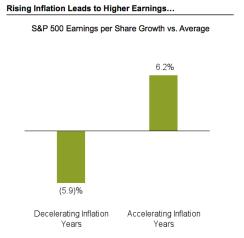

This result comes as a surprise to many investors. They correctly point out that as long as a company’s expenses don’t increase as fast as its revenues, a wider profit margin will translate into greater cash flows. Those conditions fit most companies at which wages are the largest component of expenses, because wages tend to rise more slowly in response to higher inflation than do other measures, such a s commodity prices.

|

|

There are exceptions. For example, in periods when inflation is extremely low or negative, rising inflation expectations tend to coincide with an increase in equity prices. Why? As inflation moves from abnormally low to more normal levels, economic uncertainty falls—and with it, many types of risk premiums.

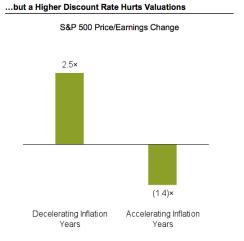

But most of the time—and for most stocks—higher discount rates more than offset higher cash flows. As a result, diversified equity indices in nearly every country we studied tended to fall when inflation accelerated.

Some equity sectors, such as natural resources and real estate, have historically done better than the market as a whole when inflation has picked up; some even benefited from rising inflation. Why? These sectors typically have such high fixed costs that when inflation accelerates, the benefit of margin expansion outweighs the damage from higher discount rates.

In short, we think there are many reasons for investors to continue to hold a large allocation to equities, but inflation protection shouldn’t be one of them. If investors want to start protecting their portfolios from inflation before accelerating inflation makes such protection too expensive, they should substitute real cash, real bonds and real assets (short- and intermediate-term inflation-linked debt and commodities, real estate and shares in commodity-related companies) for some portion of their cash, bond and equities holdings.

Seth Masters is Chief Investment Officer—Asset Allocation at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio management teams.