Would you invest in a company that only sold to 1 out of 80 leads? Or a company that typically took one year and 3 professionals just to close a single client?

In fact, you've already invested in that company: your private equity fund. According to our data, the median investor in private companies reviews over 80 opportunities in order to make 1 investment. The median private equity fund required 3.1 investment team members to close one transaction in one year. By the standards of most traditional sales processes, private equity origination is a very inefficient and labor-intensive process...despite the fact that an effective deal origination process is fundamental to successful investing. This is particularly surprising given that private equity funds who employ a pro-active origination strategy have consistently higher returns, driven by both greater quantity and higher relevance of incoming investment opportunities.

We recently completed the first-ever study of how private equity and venture capital funds originate new investments. We drew on our personal work experience with leading institutional investors, in-depth interviews with over 150 funds, and our proprietary dataset of their origination practices.

Based on our study, we have identified five recommendations to improve the volume and relevance of dealflow.

1. Build a specialized outbound origination program.

Investors with dedicated, large-scale sourcing teams are almost all top-quartile performers across stage, vintage, and sector. Professors Henry Chen, Paul Gompers, Anna Kovner, and Josh Lerner found in a research paper that the best performing VC funds are based in the major venture centers (Silicon Valley, Boston, and the New York area), but their best investments are outside of those geographies. The non-local deals outperform by 4-5 percent.

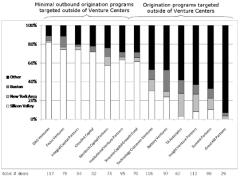

Exhibit 1: Leading Late-Stage Technology Investors' Portfolio by Geography, 2001-1Q2010

Notes: Only for IT & related sectors. Battery & Sequoia data only include late stage/growth equity deals.

Exhibit 1 is a case study of the geographic diversification of the largest late-stage technology venture capital / growth equity investors. The funds with sophisticated non-venture center outbound origination programs have almost all have been able to raise funds equal or larger than their preceding fund in the economically challenging period 2007-2010.

They are typically among the top quartile performers. By contrast, most of the funds on the left with a local focus have not raised new funds since late 2005.

2. Create opportunities, instead of waiting for opportunities to appear.

A number of the funds we studied use an origination approach that allows them to proactively co-create companies or opportunities. VCs such as Benchmark Capital and General Catalyst Partners work with Entrepreneurs-In-Residence (EIRs) to develop their ideas, giving them an advantaged position to lead an investment in any resulting company.

Private equity funds such as Castle Harlan partner with leading corporations when bidding on investments, allowing them to bring unique value and resources vs. other possible investors. Frontenac Company uses a "CEO1ST" strategy, partnering with "deal executives" to source investments in these executives' focus industries.

3. Use deal signals to look for targets which are both attractive investments and are likely to welcome an outside investor.

In order to filter the universe of companies, some investors specifically reach out to companies flashing relevant "deal signals". These investors are exploiting the wealth of information about private companies available online. For example, an increase in Internet traffic is usually a sign of customer traction. A family-run company that hires an outside manager is flashing a signal that the firm may welcome an outside investor.

4. Openly discuss your strategy, leveraging social media.

Historically, institutional investors kept their investing strategy very discreet. However, today about 10-15 percent of the 1,000 active venture capitalists blog, according to Jeff Bussgang, General Partner, Flybridge Capital Partners. These investors have found that openly discussing their investment theses increases their perceived expertise and trustworthiness, and thus generates dealflow. HealthPoint Capital has made their blog a destination for M&A/investing information in their target industries.

5. Focus on co-investing with the best investors in your target vertical.

VCs that are better networked at the time a fund is raised subsequently enjoy significantly better fund performance, as measured by the rate of successful portfolio exits over 10 years. Network “centrality” may be a better predictor of future performance than experience or exits. One standard deviation improvement in network centrality improves probability of successful follow-on round or exit by 5.8 percent and performance by ~2.5 percent

We recommend you market yourself as the go-to co-investor for target sectors by developing proprietary insights and a deep network of key partners and talent.

The full research study will appear in the 2010 Winter issue of the Journal of Private Equity. More data from this research project is posted at http://teten.com/deals and at http://www.teten.com/executive.

David Teten is CEO of Teten Advisors (Teten.com), an investment bank which uses a proprietary technology platform to source transactions for private equity funds, in New York, NY. Chris Farmer is Managing Partner, Ventures with Ignition Search Partners (IgnitionSearchPartners.com), which advises executive teams and investors on team building, developing Entrepreneur in Residence programs, and talent-driven origination strategies, in Boston, MA.