Has the safety trade gone too far? Our research suggests that it has. Since the eruption of the global financial crisis, investors have rushed en masse into the stocks of predictable, fundamentally stable companies and out of the stocks of more volatile, economically sensitive firms. In the emerging markets, where the flight to safety has been particularly intense, stability now looks much too expensive and risk looks much too cheap.

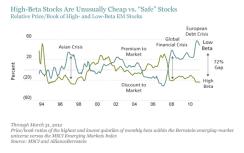

The magnitude of this gulf is illustrated by the display below, which plots the price-to-book value multiples of the lowest and highest beta quintiles of emerging-markets stocks versus the multiple of the emerging-markets index since the end of 1994. Beta is the degree to which a stock moves in tandem with the overall market.

By our analysis, the lowest beta quintile traded at a whopping 48 percent premium to the MSCI Emerging Markets Index at the end of March 2012 — dwarfing the average 8 percent premium since 1995 and representing twice the premium seen during the Asian currency meltdown of 1997–1998. Meanwhile, the highest-beta quintile traded at a 24 percent discount, much steeper than the average 3 percent discount and comparable to levels reached in the 1997–1998 period.

As this research shows, emerging-market investors generally prize stability, and have typically awarded it a premium over time. In turn, they generally want more compensation for investing in higher-beta stocks — hence, the discount over time. While the high-beta discounts to the market and to its low-beta counterpart tend to expand during times of great market stress, they have been unusually severe and persistent in the current crisis.

But, as this analysis also shows, such schisms are cyclical — and have typically presaged periods of strong outperformance for high-beta stocks. This was true following the Asian crisis, the bursting of the technology bubble and the 2008 market collapse. For example, the highest-beta quintile outperformed the market by 47 percent in the year after the valuation gap between high- and low-beta stocks peaked at around 57 percent in September 1998. In the year after the spread reached another high point in March 2009, high-beta stocks outperformed by 40 percent.

Not surprisingly, the lowest-beta group tends to be dominated by consumer-staples, telecom and utility firms, and the highest-beta group by firms in resources, financials and other cyclical sectors. Given our value bent, it is also not surprising that our research has been increasingly uncovering attractive portfolio candidates among the stocks in the higher-beta sectors while cautioning against the ‘safe’ stocks in the lower-beta sectors, which we believe have become excessively valued amid the investor fixation on near-term earnings certainty.

We do not consider valuation in isolation, however. Our investment process carefully weighs near-term risks, as well. What makes the beta gap particularly provocative today is that there is little difference in the balance-sheet quality between the high- and low-beta quintiles. Such differences had largely justified paying for safety following the late 1990s Asian crisis, when many high-beta companies had built huge debt burdens financed largely by foreign currencies just before their own currencies collapsed.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Henry D’Auria is chief investment officer of Emerging Markets Value Equities at AllianceBernstein.