Who stands to gain and who to lose from China’s shift to a market-driven system of credit allocation? That’s the crucial question facing policymakers in Beijing and investors on the mainland and around the world.

As we’ve already seen, a recent trickle of corporate defaults could turn into a sizable stream, or more, if state planners are serious about liberalizing interest rates and reforming a financial system that has showered inefficient state-owned enterprises (SOEs) with cheap credit. As the Chinese proverb says, You must kill some chickens to scare the monkeys.

The gorillas are going to resist like hell. The managers of the giant SOEs, with their vast networks of factories, party committees and patron client networks that climb up through the state and Communist Party structures in a vast tangle of influence and power, are dead set against marketized credit. So are the state-controlled banks, especially the Big Four, which now are among the world’s largest banks by assets and by far the biggest by branch or employee count.

“Financial repression has created economic rent that has been distributed to favored borrowers and nurtured vested interests,” observe the writers of China 2030: Building a Modern, Harmonious, and Creative Society. The 473-page tome was jointly written by the World Bank and the State Council’s Development Research Center (DRC) and released with considerable fanfare in 2013.

“Banks have enjoyed a comfortable business environment provided by high entry barriers, interest rate control and excess demand for credit, which allows credit rationing,” it states. “Officials’ power to control banks and their credit allocation is one source of their power over the economy and society. All these would work to mobilize resistance to financial reform and build a tendency of system inertia or regressing back to the old system.” The reader can almost hear the urgent voices of the DRC’s reformers Liu Shijin and Zhang Junkuo composing this paragraph; Liu and Zhang, both vice ministers of the research agency, are acknowledged as co-authors along with the World Bank team.

“No Chinese bank loan officer was ever fired for lending to an SOE,” said Frank Newman, former chairman and CEO of the Shenzhen Development Bank, as we sipped green tea overlooking Hong Kong’s gray-green harbor waters. “A system of market-based credit risk would require them to work hard and to face the consequences if they got it wrong. All the incentives work the other way,” he said.

When you ask why China is trying to price risk into credit, it’s amazing how quickly the conversation turns from technical finance to matters of raw political power. The deeper and more knowledgeable about China, the faster the cut to the chase. Which is why few of my usual China sources, government or private sector, are willing to go on the record about China’s great credit experiment.

“Xi and the so-called reformers in the Politburo are going to have to take on some of the most powerful centers of power in the country, to reform these SOEs,” argues a Beijing-based think tanker, who like most sources spoke on condition of anonymity because of the sensitivity of the topic. He suggests that the disciplining and purging of party members, which started with President Xi Jinping’s onetime rival to head the Politburo, Bo Xilai, and recently included Zhou Yongkang, the once-feared head of the security services, are part of this housecleaning process. “Zhou’s biggest crime wasn’t being egregiously corrupt,” the think tanker says. “The party leaders, or at least their families, are all feathering their nests with vast sums. Zhou’s biggest crime was sitting atop the huge power pyramid of the petroleum SOEs — and, of course, being allied with Bo Xilai.”

Many China watchers (including me) were puzzled when the leadership reshuffle dust settled last year to find Wang Qishan, widely regarded as a prominent economic reformer among the leadership, with new duties as secretary of the party’s Central Commission for Discipline Inspection. That’s far removed from his former post as vice premier in charge of economic, energy and financial affairs. But in the party discipline job, he’s the man in charge of the purges. In a recent act of quietly dramatic organizational redesign little noticed in the West, Wang arranged for the provincial party discipline functionaries to report directly to him in Beijing, thereby short-circuiting the party’s provincial chiefs and thus dramatically tightening the reins of power.

We have, in fact, seen this movie before: 15 years ago, to be exact. “Wang has some experience in this SOE moral hazard line of work,” said one Shanghai banker. “He knows where every single body is buried in the financial system.” He was governor of China Construction Bank, mayor of Beijing, party secretary of Hainan province — the ultimate Mr. Fixit. When the highflying Guangdong International Trust and Investment Corp. (GITIC) went broke in 1998, roiling global financial markets with the first big bankruptcy of a state-affiliated enterprise, then-premier Zhu Rongji summoned Wang, who was vice governor of Guangdong province, to preside over the messy cleanup. Creditors ultimately received about 12.5 cents on the dollar.

As it happens, I was in Shanghai when GITIC went bust, doing field research for my Ph.D. at Princeton and viewing the drama from a recently constructed Pudong hotel. I remember hearing complaints from indignant foreign bankers when Wang appointed a liquidation committee of government insiders and the Bank of China that put foreigners at the end of the line with all the other unsecured creditors, behind the priority claims of workers’ wages and taxes — precisely as set forth in China’s 1986 State Enterprise Bankruptcy Law. The numerous so-called comfort letters issued by Guangdong authorities to foreign bankers that implied a Beijing put for GITIC were instantly rendered useless for purposes other than wrapping fish or personal hygiene.

After GITIC, the rest of the other “red chip” ITICs, as the trade and investment firms were known, were cleaned up, at least in terms of their foreign obligations, though none as dramatically (or as costly) as GITIC. This was just one act in a more complex play that involved the recapitalization of the big state-owned banks; their partial listings and sales of minority stakes to foreign banks; and the creation of so-called bad banks, or asset management companies, to work off the dreck loans.

“In many respects the comfort letters issued for the ITICs were very similar to the implicit guarantees from the commercial banks for the wealth management products that they sell today,” says Michael DeSombre, a partner at Sullivan & Cromwell in Hong Kong who was directly involved in the GITIC restructuring. “Eventually the government will need to allow some failures to prove that WMPs are not risk-free deposits.”

So which enterprise or trust product chicken is going to be sacrificed for the tutelage of the monkeys? Who’s next after Shanghai Chaori Solar Energy Science & Technology Co. and Zhejiang Xingrun Real Estate Co.?

I quizzed an array of bankers, traders and economists on this point. They all agree that a default will involve a triangle: a borrowing firm in trouble, an overstretched credit trust and some anxious investors holding WMPs. But I heard several different candidates for the chicken list, each of which entails a different view of how decisions are made in China and what Beijing’s goals are in the first place.

“We think it will be the firms in those sectors with the greatest excess capacity,” suggests a Beijing-based Japanese banker. “China has firms with huge overcapacity in several sectors ranging from aluminum to steel to shipbuilding or petrochemicals. These sectors are going to have to be rationalized sooner or later. From an industrial structure policy standpoint, if some of these firms are allowed to go under, the government can hit two birds with one policy stone.”

“We will certainly see more defaults in 2014, especially in sectors where overcapacity in a major issue,” agrees Andy Liu Qiang, China analyst at Teneo Intelligence. “For example, the Zhejiang Huatesi Polymer Technical Co. filed for bankruptcy last month but may avoid a default in the end. Highsee Iron and Steel Group Co. is struggling under a 3 billion yuan ($482 million) debt. But I don’t see that additional defaults will cause contagion or pose a systemic risk unless a really major SOE in real estate associated with a local government financing vehicle runs into trouble. Until then, it is unlikely that the People’s Bank of China will react.”

Sullivan & Cromwell’s DeSombre sees wider motives in play. “Allowing small coal miners and smaller property developers to default is also consistent with the various environmental and affordable housing initiatives of the current government and thus can accomplish other policy objectives while improving credit allocation in the long term,” he says.

An alternative view contends that firms whose manager-owners are flagrantly corrupt, or flagrantly opulent, are most likely to be flushed down the credit drain. This will reinforce the moral lesson of Xi and Wang’s anticorruption campaign.

Yet a third view points the likely default finger at firms that have the least protection with the party-state power structure, those unable to ring up a provincial party secretary or even Beijing for help as the money runs out. This means firms with not too many employees, far away from a key urban area and generally out of sight.

A fourth and more logical view (at least to me) believes the best candidates for default are firms that get into basic business trouble or are merely incompetent or unlucky, rather than corrupt or politically vulnerable. “If you want the Chinese banking system to learn the lesson that poor credit leads to default, then you need to let firms go under whose credit problems could be analyzed ex ante,” says former banker Newman. “If they just blow up for some other reason, as a matter of industrial policy or some anticorruption campaign, there is no institutional learning.”

David Cui and his team of Chinese equity strategists at Bank of America Merrill Lynch in Hong Kong analyzed 12 potential trust defaults mentioned in Chinese media, and then reviewed the top 200 trust products by size in the database of China’s Wind Information Co. They found the trusts concentrated in three sectors: property developers, coal miners and local government financing vehicles, or LGFVs. The total outstanding credit of each sector coming due in 2014 or 2015 amounted to 52 billion yuan, 20 billion and 47 billion, respectively. Surprisingly, most of that credit is concentrated in just five provinces: Jiangsu, Shanxi, Inner Mongolia, Guangdong, and Tianjin; peak maturities fall in May and June 2014 and in the fourth quarter of this year.

“Coal mining could see the most defaults, as many of them are private and coal prices plummeted,” the analysts contended in a February note to clients. “LGFVs will have the most government support/intervention and may see limited defaults. Property trusts could diverge, as smaller developers with single-city operations in tier-3/4 cities could be in trouble, but large national developers should be fine.”

Allowing such defaults isn’t for the faint of heart. There is a contagion risk and a policy risk in launching China’s Great Credit Experiment. Each risk unfolds to a different clock, but both carry potentially grave consequences.

“If you are the PBOC, you want to minimize the spillover from any single default on the rest of its sector or locality,” says an economist friend of mine at a university in Shanghai. “You know, when the mah-jongg tiles knock each other over in a line. What you want to avoid at all costs is a full-blown credit crisis.”

This is what the “can’t get there from here” critics fear will happen because of the multiple pipes between the traditional and shadow banking systems. And this is where the “one system, two markets” defenders insist that a slow pace of reform is important. Above all, they warn, do not dismantle the state-owned banking sector or force it into a competitive market too quickly.

“Financial reforms that led to a sudden shift in the willingness of banks to roll over these loans — for instance, because a higher-cost-liability structure compelled them to seek higher-return assets — could result in widespread corporate and local government insolvency and a permanent collapse in land values that could ripple with malign effect through the rest of the financial system,” warns Arthur Kroeber, senior fellow at the Brookings-Tsinghua Center in Beijing and editor of the China Economic Quarterly, in a 2013 paper,“China’s Global Currency: Lever for Financial Reform.”

“The only significant risks of crisis would stem from policy blunders in the direction of privatizing banks and other institutions too precipitously, or opening China to short-term capital inflows and outflows prematurely,” says Albert Keidel, a senior fellow at the Atlantic Council who has watched the evolution of China’s financial system for decades, first as a consultant for the United Nations and the World Bank in the 1980s and 1990s and then at the U.S. Department of the Treasury.

“China’s commercial banks are not really banks. Despite their IPOs and foreign strategic investors, they are basically government-controlled deposit-taking institutions,” he explains. “Most of the banking system is thus in effect an extension of the central bank, which is of course in no way independent from policymakers. The high degree of continued government ownership and control is in effect a limitless pool of contingent assets hidden on the books of these so-called banks. This is not a system at risk of financial failure.

“I would tone down the Sturm und Drang of the choices facing China on financial sector reform,” adds Keidel. “They have done a lot in the past ten years, and they will do more in the next ten years, but the need for dramatic moves now to avoid a crisis precipice is just way over the top, in my humble opinion. It does sell hedging instruments to the corporate globe, however.”

Some market participants share this sanguine view. “I don’t expect large-scale defaults in China unless the first-world stock markets correct more than 10 to 15 percent, which I don’t expect. There will be individual firm defaults, but they are likely to be ‘good’ defaults, from bad business models, incompetence and so forth on a large scale,” says one Connecticut-based trader. “So a 2014 default is likely a one-off event unless trouble is brewing on a global scale. China is still a rigged game, and they [the authorities] have levers to pull and moves to make to contain contagion.”

Cui and his BofA Merrill Lynch analysts are similarly relaxed. “We believe that the most at-risk products involve private borrowers, unprofitable sectors, highly indebted regions that are less important economically nationwide and where local government commands little resources,” they wrote in their report. “As the market hears more subsequent events of trust defaults, coal miner or developer bankruptcies and higher bank nonperforming loans, there might be moments of panic and capitulations in the stock market.”

However, they conclude, “we don’t think it will lead to systematic risks in China. Assuming a 25 percent default ratio on trust loans, potential bad debt would be roughly 4.7 trillion RMB, or 6 percent of bank loans.” This has already been fully priced into the valuation of Chinese banks, they believe. Moreover, “from a long-term perspective, this should be a very positive milestone event to establish the ‘credit culture’ among Chinese depositors/investors, curb the shadow banking market, facilitate the cleaning up of zombie companies, reduce banks’ implicit guarantee of off-balance-sheet risks, channel money back into bank deposits and restore global investors’ confidence in China’s financial system and banks.”

“The ‘extend and pretend’ policies used by Japan in the 1990s and by Europe today demonstrate the ability of policymakers to defer pain almost indefinitely,” says one Connecticut hedge fund manager. “The Chinese policymakers clearly have even more control over the credit and banking system than their open-market colleagues in Japan and Europe and therefore have even more ability to manage timing of the ‘adjustment’ process. So I personally am not a believer in an imminent credit train wreck, just in a slow bleed to lower potential growth over time in China as reform and free-market liberalization are implemented. The current leadership is showing impressive skill in their execution of their reform agenda so far, and so inspire confidence that the liberalization of the credit system will be well managed.”

“Ultimately, ‘one system, two markets’ will lose its purpose and will no longer need to exist,” predicts Teneo’s Andy Liu Qiang. “Eventually it will be just ‘one system and one market.’ The government’s plans for reforming SOEs by promoting mixed ownership with private capital and migrating to sources of funding other than bank borrowing will change this model over time.”

The consensus of expert opinion, including those quoted above, suggests that there will be defaults in 2014, possibly quite a few of them, but that the risk of broader contagion is slim. What does the wisdom of crowds, or at least the judgment of markets, say about this risk?

Foreign creditors may be a small part of the puzzle, but they do vote with their trades on China’s overall credit rating. The price of a credit default swap on five-year China sovereign debt jumped to 99 basis points in mid-March, just after Chaori Solar’s default, compared with 63 basis points a year earlier. The price eased back to 89 basis points in mid-April.

But what do Chinese savers think? If our experts are correct, Chinese domestic anxiety about credit defaults presents the biggest risk of contagion. In order to gauge this, a former Princeton student of mine, Faaez Ul Haq, designed a software tool to extract the tone and volume of social media conversations in China over time. It uses natural language-processing techniques to search for key word patterns in the Chinese microblogosphere, sampling 1 percent of the conversations on Sina Weibo, the largest Chinese microblogging service with about 100 million posts per day. This is the same Sino Weibo that raised $286 million with an initial public offering on Nasdaq on April 16.

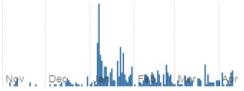

Strikingly, a search for Weibo posts with the character compound for “shadow banking” leaped from low background noise up to a sharp peak on January 7, when the State Council’s Directive 107, laying out measures to bring the shadow banking system under control, leaked to the public domain. The frequency of citations has eased since then.

But a search of Weibo posts for “credit default” ran low in January and February and then suddenly spiked after the Chaori Solar and Zhejiang Xingrun defaults on March 4 and March 16, respectively.

From these Weibo filters, it looks as if the State Council directive focused China’s blogosphere on shadow banking, and then the first actual credit defaults seized bloggers’ collective attention. Any subject that has the attention of tens of thousands of Chinese netizens is likely to catch the attention of party leaders, who themselves use Weibo to monitor the pulse of the public, given that reliable opinion polls on sensitive subjects are few and far between.

The political risk of the Great Credit Experiment is harder to judge and moves more slowly than the flash-crash of a financial contagion, but it could be even more threatening to those at the apex of the Politburo.

“The Big Four banks form the very core of the party’s political power; they work in a closed system with risk and valuation managed by political fiat,” conclude Carl Walter and Fraser Howie in their book, Red Capitalism. “Any material liberalization of this framework would strike at the heart of a system that is designed to benefit the party and these same oligopolies.”

In other words, in order to keep the economy growing and thereby maintain its legitimacy with the Chinese public at large, the party will have to risk undermining its own base of power. This is a steep challenge for any leader in any political system.

The first step for success is taking charge and eliminating all challengers. As Brookings-Tsinghua’s Kroeber observes in a March paper, “After the NPC: Xi Jinping’s Roadmap for China”, “Perhaps the biggest surprise of Xi’s first year was the speed with which he consolidated his power and signaled his policy intentions. He achieved this through two big housecleaning drives.”

A former CIA colleague of mine with long experience in China agrees. “Every cadre and every SOE manager in China has his head under his desk, hoping his name isn’t on one of Wang Qishan’s lists,” he mused over a cup of green tea in Hong Kong. “I’ve never seen it so tense, not for decades.” The newsstands from Beijing to Hong Kong are loaded with magazines about the infighting, with glossy cover photos of a smiling, confident Xi Jinping (clearly enjoying a triumphal, almost imperial tour of Europe), a glum Bo Xilai and an even grimmer Zhou Yongkang.

|

In China 2030, Liu and Zhang and their DRC colleagues warn that “China could conceivably sustain high economic growth for a while longer even without fundamental reforms in the financial sector. Eventually, these distortions and imbalances would undermine social stability, slow productivity growth, and erode competitiveness. The potential debilitating effect of a future forced financial liberalization, and lack of an integrated approach and concerted actions on the part of the government, can only serve to exacerbate the negative consequences.”

I can imagine the unhappy faces of the members of the Politburo Standing Committee absorbing this stern economic medicine, only to have Liu & Co. raise the ante again, this time to politics, as they further advised: “Financial reform can progress successfully only when accompanied by institutional and organizational reforms. Liberalizing market rules without changing old institutions can deepen distortions.”

Brave words. As Walter and Howie conclude in Red Capitalism, “All institutional arrangements in China are impermanent; everything can be changed as a result of circumstances and the balance of political power. All institutions are in play, even the oldest and most important.” Except, of course, the Communist Party of China.

James Shinn is lecturer at Princeton University’s School of Engineering and Applied Science (jshinn@princeton.edu) and CEO of Teneo Intelligence in New York City. After careers on Wall Street and Silicon Valley, he served as national intelligence officer for East Asia at the Central Intelligence Agency and as assistant secretary of defense for Asia at the Pentagon. He serves on the advisory boards of Kensho Technologies, a Cambridge, Massachusetts–based data analytics firm, and CQS, a London-based hedge fund.