The decision by the People’s Bank of China (PBOC) early this year to weaken the renminbi came as a shock to many investors who expected the currency to maintain a long-term path of appreciation. After all, the renminbi had been strengthening against the U.S. dollar for nine years, and its trajectory was consistent with the government’s stated aim of internationalizing the currency.

For close observers, however, the move wasn’t unprecedented or necessarily at odds with Chinese policy. The PBOC had made a similar move in mid-2012, lowering the rate at which the renminbi was fixed each day against the dollar. A six-month period of slight depreciation followed; during that time, the PBOC widened the band around the fix in which the renminbi could trade. Eventually, the currency resumed its upward climb.

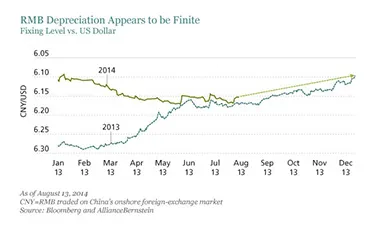

This year’s episode appears to have been following a similar script. In January the PBOC began weakening the renminbi by lowering the daily fix versus the dollar; then in mid-March the central bank announced that the trading band would widen from plus or minus 1 percent to plus or minus 2 percent. This guided weakening helped to defuse market speculation that the renminbi was a one-way bet. The wider trading band was in line with the policy of moving to a market-driven exchange rate.

In the same way that the PBOC’s actions don’t necessarily signal an end to the policy of managed renminbi appreciation, the currency’s fundamentals don’t make a case for it being overvalued — or even fairly valued. China’s trade balance — the main driver of its balance of payments surplus — hit record highs of $47 billion in July and $49 billion in August. The country’s accumulated foreign exchange reserves are about to exceed $4 trillion, having increased by more than 500 percent since 2005; during that time, the renminbi has appreciated by only 30 percent or so. This mismatch helps the PBOC contain the risk of cheap money and credit bubbles in the domestic economy. It also suggests that the renminbi is undervalued.

The expansion of China’s foreign exchange reserves and balance of payments surpluses has put the country under pressure from the international community to strengthen the currency more quickly. China’s response has been to guide the renminbi higher over any rolling 12-month period while allowing short periods of weakness in an attempt to inject some two-way volatility into the currency. Presumably, this is because it’s easier for China to engage with its international counterparts if it can honestly point out that currency policy is still on a path of appreciation at all times throughout the year.

In this context, we regard the renminbi’s depreciation year-to-date (see chart) as finite and implying a likely recovery, rather than further weakness. If one believes — as, in our view, the evidence suggests — that China hasn’t changed its stance on the currency, then the renminbi’s performance on a rolling 12-month daily basis should be flat to positive. If that’s the case, this year’s depreciation has reached a point relative to last year’s performance, illustrated by the blue line in the chart, at which the daily fix may strengthen, reversing the recent trend. This would enable the renminbi to resume its steady appreciation on a rolling 12-month daily basis and keep the positive currency policy intact.

In other words, the PBOC’s desire to maintain an appreciating currency is likely to result in an end-of-year rally in the renminbi.

Hayden Briscoe is director of Asia-Pacific fixed income at AllianceBernstein in Hong Kong.

See AllianceBernstein’s disclaimer.

Get more on foreign exchange.