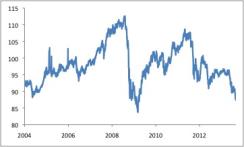

Emerging-markets assets have suffered considerably since the Federal Reserve began talking earlier this year about the gradual reduction of monetary stimulus. Emerging-markets currencies in particular have taken it on the chin. As chart 1 shows, the aggregate emerging-markets exchange rate in nominal terms has depreciated by nearly 10 percent since May. That move has come despite essentially no weakening in the most important emerging-markets currency, the Chinese renminbi. Several high-profile currencies have tumbled considerably more, including the Indian rupee (22 percent) and the Indonesian rupiah (17 percent). Even the Mexican peso, a market darling at the start of 2013, has slipped roughly 11 percent since the second quarter. With this year’s round of turbulence following on the heels of slides in 2011 and 2012, emerging-markets currencies have unwound nearly all of their appreciation from their 2009 trough.

Chart 1: EM FX Index

Source: Bloomberg; data through August 30, 2013

The connection between Fed tightening and this bout of currency depreciation has shone a spotlight on emerging-markets current-account deficits, a typical culprit in past foreign exchange crises. As global credit conditions tighten — with the prospect of higher developed-economy interest rates dampening capital outflows bound for developing countries — funding for current-account deficits becomes scarcer, forcing a combination of slower emerging-markets growth and competitiveness-boosting currency depreciation to narrow those shortfalls.

This narrative, however, does not entirely explain the present episode. With emerging-markets GDP growth having run below its underlying trend since mid-2011, current-account deficits have not widened much in aggregate in the past couple of years and do not look large by longer-term standards. Indeed, by almost any metric, emerging-markets economies do not appear to be overheating.

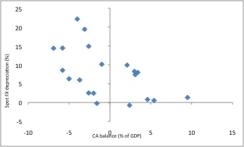

Indeed, in a cross-country sense, current-account deficits and forex depreciation during the past few months do not display a strong link. Chart 2 shows, for a sample of 20 emerging-markets economies, the projected current-account deficit for 2013 as a percentage of GDP, along with the nominal depreciation of the currency against its main natural trading partner (either U.S. dollars or euros, or a basket of the two in the cases of Russia and Turkey) since the beginning of May. The chart suggests some connection but also implies that there is more to the story. Indeed, a simple regression of forex depreciation on the current-account deficit produces an adjusted R-squared of just 0.25. The biggest fall has come in India, with a fairly moderate current-account deficit at 4 percent of GDP. Several countries with significantly larger current-account gaps have experienced less depreciation, and a few developing economies that are running current-account surpluses have seen their currencies slide fairly sharply.

Chart 2: Emerging-Markets Current-Account Balance and Foreign Exchange Move Since May 1

Most likely, emerging-markets economies are experiencing not only a flow adjustment but also a stock problem. The easy global money atmosphere of the past several years likely encouraged greater capital flows into developing economies than would otherwise have been the case. Though those flows did not look particularly impressive at the time — and indeed did not produce large-scale currency appreciation of the sort observed in the mid-2000s — they occurred despite sluggish emerging-markets growth, stagnant commodity prices, narrowing corporate profit margins and specific problems in several large developing economies.

Were it not for abnormally low interest rates in nearly all developed-market economies, this backdrop means that emerging-markets countries likely would have received considerably less capital than they did. Now, with risk-free rates on the rise globally, some of that money is coming home. Not only do emerging-markets economies need to run narrower current-account deficits, they must also finance the unwinding of some portion of the stock of foreign investment built up in recent years.

This stock adjustment helps to explain some of the specific points on chart 2. Like India, Brazil has seen its currency weaken by upward of 20 percent despite a reasonable current-account deficit, roughly 3 percent of GDP. In both cases high local interest rates helped attract flows into local bond markets in recent years despite concerns about these countries’ medium-term paths. Indeed, in both cases potential growth rates appear to have slowed noticeably in the past three years, thanks in part to government policy stances perceived as unfriendly to private investment. As growth-inflation trade-offs have worsened, large interest rate differentials have sustained capital inflows. With rates grinding upward in the developed world, that pure yield-seeking money is exiting these economies.

As a group, the Association of Southeast Asian Nations stand out on the chart. Malaysia, the Philippines and Thailand all boast current-account surpluses but have experienced currency depreciation of 8 to 9 percent. Indonesia, with a modest deficit, has suffered one of the largest currency falls. As a common factor, all of these economies have gone through credit booms in the past few years, with domestic demand benefiting from rapid bank credit expansion — funded in part via capital inflows. Strong growth stories against a generally weak emerging-markets background in turn have promoted further inflows to local equity and bond markets (in the first months of 2013, stock markets in these countries posted significant gains even as overall emerging-markets equities struggled). Some of those inflows are now reversing, and capital-account deficits are outweighing the effect of ongoing current-account surpluses and forcing foreign exchange adjustments.

The Central European economies also look conspicuous, for the opposite reason. Their currencies have displayed great stability in recent months, despite a worse overall current-account position than, for example, the Asean countries. (Hungary, however, is running a very large surplus.) Two factors likely are supporting these exchange rates. First, the revival of euro area growth is boosting Central European exports, and current-account run rates may have improved relative to the projected full-year outcomes shown in the chart. Indeed, Poland has recorded current-account surpluses in recent months.

Second, that same phenomenon — the improved atmosphere throughout Europe — is likely encouraging at least some capital inflows to Central Europe, a region that has suffered two debilitating recessions in the past five years and that has hardly been in favor among international investors until recently. At the moment, Central Europe is probably enjoying the most favorable marginal shift in perception of any region within the emerging world.

Compared with past currency-crisis episodes, emerging-markets economies appear to face less current-account vulnerability this time around. Most are running only moderate deficits, and the foreign exchange weakness that has already occurred should suffice to shrink these gaps to sustainable levels in most cases. But emerging-markets currency depreciation in 2013 appears to reflect capital flow reversal as much as or more than it does the shrinking availability of current-account financing. This need to unwind a portion of the stock of foreign investment built up during the global easy-money regime means that the present phase of emerging-markets currency weakness may persist for a while and wind up amounting to more than current-account figures alone would imply.

Michael Hood is a market strategist for J.P. Morgan Asset Management.

Read more about foreign exchange.