The heat in the pressure cooker that is the bond market may be starting to reach a boiling point. Following years of artificially elongated global yield compression, it would appear that pressure valves are beginning to give. As investors start to realize the limitations of global central banks in maintaining complete dominance over fixed-income market pricing, the razor-thin margins of safety in bonds are becoming evident. With negative real returns, virtually no coupon income and significant duration risk in many types of traditional fixed income, investors can lose money very quickly.

With the Federal Reserve potentially raising interest rates this year for the first time in nine years, we may now be at an inflection point. From 2004 to 2006, when the Fed raised rates from 1 percent to 5.25 percent, market expectations undershot both the timing and the magnitude of each increase, causing interest rates to move higher and resulting in losses for investors holding short-term debt. As we embark on what may be the next tightening cycle, investors need to look beyond traditional fixed income to protect their portfolios. They need to consider an absolute-return approach (see chart 1). That means having the ability to be tactical and selective in exposure to interest rate and credit risk and able to access noncorrelated sources of return; to take a systematic approach to hedging to mitigate drawdowns and manage risk with a focus on capital preservation; and to construct portfolios that can produce returns, regardless of the market scenario or cycle.

As a practical example of this absolute-return approach, the fall in oil prices has created opportunities to generate returns in traditional and alternative credit. Panic selling and outflows in late 2014 resulted in attractively low prices for U.S. high-yield debt, providing an opportunity for us to add to exposure. Since then, the broader U.S. high-yield market has returned approximately 4 percent.

At the time of the oil price fall, high-yield energy bonds also sold off, regardless of underlying credit fundamentals. This created an opportunity to add to the sector through traditional cash bonds, as well as short positions via credit default swaps. We’ve opportunistically increased our allocation in the high-yield space by as much as 15 percent over the past six months. We look for three characteristics when searching for value in this space: compensation rewarded in the form of better yields, lower correlations for the delivery of better risk-adjusted returns and a premium for liquidity.

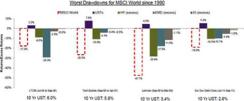

It’s evident most categories of fixed income were not providing the hedge needed during falling equity markets (see chart 2). The only asset class that was functioning was Treasuries, largely because yields were starting from a higher base. With U.S. Treasury yields now around 2 percent and German Bunds at 1 percent, government bond yields no longer provide any cushion, and with rates already at or near zero today, this eliminates the ability for traditional bonds to act as a hedge when equities fall. Investors would be well served to consider a strategy that is noncorrelated to the direction of interest rates, and that can be a true diversifier to equity risk.

Another interesting example is the nonagency securitized segment, where we can access returns supported by improving consumer confidence in the U.S. without undertaking significant interest rate exposure. We’ve played this through beta exposure to seasoned prime and Alt-A legacy nonagency mortgage-backed securities that are supported by strong technical factors and likely to do well as U.S. home prices rise.

Perhaps most important, as volatility levels in the bond markets have moved higher, our allocation to cash has moved meaningfully lower as we deploy that cash. Previously our high cash holdings reflected our priority of capital preservation and hedging in an environment of limited opportunities, but today we stand ready to capitalize on a rapidly shifting opportunity set. Whereas volatility can scare traditional fixed-income investors away from the store, we welcome it as an opportunity to go shopping at a discount.

Bill Eigen is head of absolute return and opportunistic fixed income at J.P. Morgan Asset Management in Boston.

Get more on fixed income.