This blog is the first in a new series on Institutionalinvestor.com entitled Global Market Thought Leaders, a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is AllianceBernstein, who will be providing analysis and insight into equities.

Fear is a funny thing. It’s an emotional response to a situation, yet in the markets, many of our worst fears are induced by hard, rational statistics.

In China, a deluge of data appears to prove that the economy is about to collapse. Who can argue with high inflation, slowing industrial production, weakening property sales and power shortages? It’s all in the numbers, right?

I’m not so sure. While there’s no shortage of worrisome statistics, I prefer to look beneath the surface.

For example, our regional analysts aren’t unnerved by weakness in the Chinese auto or steel industries. Both are subject to significant inventory changes that can prompt short-term aberrations. Instead, our analysts look at things like cement production and power generation, which point to solid underlying economic activity, despite recent power cuts.

The point is that newspapers choose the scariest indicators, but investors should look for the most reliable data.

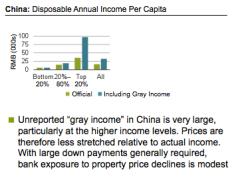

I’m not saying that homes are cheap in China (neither are stocks, by the way). I am saying that context is crucial. Don’t just look at Beijing and Shanghai—where property prices are the most inflated. This is a country of a billion-plus people. In some smaller cities, property markets are much healthier, yet shares in regional construction companies are being tarnished by indiscriminate fear.

Of course, China faces real challenges. It has too much investment-led growth, too little consumer-led growth, too much state control and a perennial currency problem.

But even if China’s GDP growth slows to a more sustainable 8%–9%, I don’t think the end is near. Yet, since fears of a Chinese collapse echo around the world, I’m on the lookout for value in global stocks that depend on China’s growth, particularly in sectors such as commodities.

Kevin Simms, Global Director—Value Research at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio management teams.