Introduction:

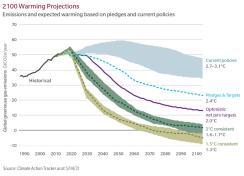

Problem: Our world is facing a climate crisis that requires immediate action. Scientific evidence suggests we must limit global warming to no more than 1.5 degrees Celsius above preindustrial levels by the year 2100. If we cannot accomplish this, the environment, and therefore society and the global economy, will be seriously harmed, perhaps irreversibly.Development: We are not on track to meet the Paris Agreement goal of limiting warming to well below 2, and preferably below 1.5, degrees Celsius above preindustrial levels. Today's regulations are consistent with an increase of 2.9 degrees, and existing government pledges, if met, would only limit warming to 2.6 degrees. Companies must step in to close the gap, and they need to do so in a rigorous and consistent way that is aligned with current climate science.

Materiality: Society’s focus on climate change is leading to more regulation of carbon emissions. To improve efficiency, manage costs and reduce risk, many companies are setting emissions reduction targets, but the robustness of these varies substantially. By evaluating company emissions targets, we can better predict future cost trends and business opportunities, and better understand the operational quality and resilience of the businesses we own.

Next steps: Use the ESG data tool developed by our ESG analysts to determine if the companies you cover have set, or have committed to setting, a science-based target.1 Engage with companies that have not done so already. For those that have set only a company-defined or net zero target, carefully analyze the target. Consider what each company's approach to climate issues says about management quality, long-term operational resilience, and the ability to take advantage of emerging climate-related opportunities.

Detail

Problem: Our world is in the midst of a climate crisis. Human activity that has increased greenhouse gas emissions, primarily the burning of fossil fuels, is warming the planet. Current scientific evidence suggests we must limit global temperature increases to no more than 1.5 degrees Celsius above preindustrial levels. If we cannot accomplish this, the environment will be seriously damaged, perhaps irreversibly. The temperature of the planet has not risen above the plus 2 degrees Celsius limit in 3 million years.Science suggests we are approaching, or indeed may have already passed, several tipping points that could accelerate or compound the problem further. For example, the polar ice caps melting and rainforest deforestation. Our society and economy require Earth's systems to function stably. The increasing temperature will result in hotter heat waves, more wildfires, more frequent droughts, rising sea levels, and other negative impacts — many of which we are already experiencing. These developments could cause unparalleled disruption to life as we know it. Crippled supply chains, mass migration caused by food insecurity, extreme weather and increased geopolitical unrest will be some of the many challenges.

Development: The Paris Agreement brought together over 190 countries with the goal of limiting global warming to well below 2 degrees Celsius by the year 2100. To accomplish this, society must achieve net-zero emissions by around 2050 with about a 50% absolute reduction in emissions by 2030. Encouragingly, the 192 countries that are part of this agreement are taking action. Each country has submitted a nationally determined contribution (NDC) that outlines its plan to reduce carbon emissions and address the impact of climate change.

But will society achieve its goal? Currently, the answer appears to be a resounding no. As shown in the chart above, today's regulations are consistent with an increase of 2.9 degrees, and existing government pledges are consistent only with a 2.4 degrees' increase. As a result, there is growing pressure on corporates to move beyond seeking minor reductions in carbon emissions per unit of energy produced, with the new goal of net zero or even absolute zero emissions.

Materiality: The transition to net zero emissions will require a substantial change in the mindset of company management teams. Some will act too slowly to avoid the impacts of future regulation, additional cost burdens, or a loss of their social license to operate. Companies that do make the necessary changes stand to benefit from lower costs and from new business opportunities.

Although most companies have set targets to reduce their emissions, the strength of these targets varies significantly. There are three basic types:

- Company-defined goals are generally the least stringent. These targets are based on the reductions the management team thinks the business can achieve. Not grounded in climate science, they neither rely on standardized climate accounting or measurement nor consider what the company needs to achieve in order to help broader society meet its goals. Therefore, it may be a red flag if a company has only set this type of target.

- Net zero commitments are generally more robust than company-defined goals. In a net zero commitment, the management team is agreeing to put the business on a trajectory to be "carbon neutral" by a certain date, usually 2050, in line with the Paris Agreement. Unfortunately, many net zero commitments are insufficient for one or more reasons, including the following:

- The company is not committed to reaching absolute zero emissions by 2050 but rather to balance carbon releases with a similar amount of "offsets" which fund projects that sequester greenhouse gases. However, the quality and impact of these projects varies significantly. Most carbon removal technologies remain unproven at scale, making the reliance on them problematic. In addition, offsets like carbon capture could result in stored emissions leaking back into the atmosphere over the long term or increased competition for land where reforestation is envisioned, making this option increasingly expensive. Importantly, the use of offsets may also delay actual emissions reductions that are needed in the near term

- Timing is another crucial shortcoming of net zero commitments. There is a significant difference in total expected emissions based on how quickly a company achieves net zero. The longer it takes, the less likely society is to achieve its climate goals.

- Scope 3 emissions,2 which can be a very large portion of a company's carbon impact, may not be included in a net zero commitment.

- Science-based targets are the most stringent carbon reduction target-setting processes currently available. A partnership of the CDP, the United Nations Global Compact (UNGC), the World Resources Institute (WRI), and the World Wide Fund for Nature (WWF), the Science-Based Targets initiative (SBTi) offers a more robust approach using climate science to define and promote best practices in the corporate emissions target-setting process. Science-based targets offer many assurances:

- Companies must follow strict SBTi guidance when developing their goals, making it easier for investors and other stakeholders to evaluate the strength of corporate targets.

- The SBTi reviews and approves all corporate submissions, which drives consistency and transparency in corporate target setting.

- The use of carbon offsets and avoided emissions is not allowed, and scope 3 emissions inclusion is required for most companies, ensuring corporate targets are more robust.

- SBTs do not require companies to set net negative goals, i.e., sequestering more carbon than they emit. Ultimately, net negative emissions will likely be needed to achieve the Paris Agreement goal due to some countries and companies failing to reach their targets and emissions from sources with no mitigation opportunities. As a result, companies may need to do even more than what is currently required by the SBTi.

- The SBT framework relies on the Sectoral Decarbonization Approach, which is based on assumptions that assign only a 50% probability of staying below a 2°C increase. Given that climate change affects humanity and the planet at large, a higher probability is preferable.

By evaluating company emissions targets, we can better understand the long-term cost trajectory, operational quality and resiliency of the businesses we own. In addition, a clear understanding of climate issues may also lead to new business opportunities for certain companies.

Next steps:

- Use the ESG data tool to determine if the companies you cover have committed to or have set a science-based target. Engage with companies that have not.

- For firms that have only set a company-defined or net zero target, analyze the trajectory of emissions reductions, strategies to achieve those reductions, and the long-term viability of any offsets that are part of the target.

- Consider what the company's stated approach to managing carbon emissions says about management quality and long-term operational resilience.

- Evaluate whether a company's deeper understanding of climate issues might enable it to take advantage of new business opportunities.

- Determine if any modeling or valuation adjustments are necessary for leaders or laggards.

- Continue engagement and monitoring of the company to understand progress.

In addition to working with our portfolio companies to understand environmental risk and opportunity, MFS is actively evaluating our environmental impact and working to implement a science-based target of our own.

Endnotes

1 Emissions reduction targets are considered "science-based" if they are in line with what the latest climate science deems necessary to meet the goals of the Paris Agreement — limiting global warming to well below 2°C above preindustrial levels and pursuing efforts to limit warming to 1.5°C. (source: The Science Based Targets initiative (SBTi))

2 Scope 3 emissions: all indirect emissions (not included in Scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions (source: The UN Global Compact (UNGC))

Please keep in mind that a sustainable investing approach does not guarantee positive results.

The views expressed are those of the author(s) and are subject to change at any time. These views are for informational purposes only and should not be relied upon as a recommendation to purchase any security or as a solicitation or investment advice from the Advisor.

Unless otherwise indicated, logos and product and service names are trademarks of MFS® and its affiliates and may be registered in certain countries.

ESG in Depth is an internal research series produced for the benefit of MFS investment professionals. Although some ESG in Depth communications are made available externally to illustrate the thematic research regularly produced by and for our investment team, all suggestions in the document are directed at MFS investment professionals, not to the general public.

Distributed by:

U.S. - MFS Investment Management; Latin America - MFS International Ltd.; Canada - MFS Investment Management Canada Limited. No securities commission or similar regulatory authority in Canada has reviewed this communication.

Please note that in Europe and Asia Pacific, this document is intended for distribution to investment professionals and institutional clients only.

U.K./EMEA – MFS International (U.K.) Limited (“MIL UK”), a private limited company registered in England and Wales with the company number 03062718, and authorized and regulated in the conduct of investment business by the U.K. Financial Conduct Authority. MIL UK, an indirect subsidiary of MFS, has its registered office at One Carter Lane, London, EC4V 5ER UK/MFS Investment Management (Lux) S.à r.l. (MFS Lux) – MFS Lux is a company is organized under the laws of the Grand Duchy of Luxembourg and an indirect subsidiary of MFS – both provides products and investment services to institutional investors in EMEA. This material shall not be circulated or distributed to any person other than to professional investors (as permitted by local regulations) and should not be relied upon or distributed to persons where such reliance or distribution would be contrary to local regulation; Singapore – MFS International Singapore Pte. Ltd. (CRN 201228809M); Australia/New Zealand – MFS International Australia Pty Ltd (“MFS Australia”) (ABN 68 607 579 537) holds an Australian financial services licence number 485343. MFS Australia is regulated by the Australian Securities and Investments Commission.; Hong Kong – MFS International (Hong Kong) Limited (“MIL HK”), a private limited company licensed and regulated by the Hong Kong Securities and Futures Commission (the “SFC”). MIL HK is approved to engage in dealing in securities and asset management regulated activities and may provide certain investment services to “professional investors” as defi ned in the Securities and Futures Ordinance (“SFO”).; For Professional Investors in China – MFS Financial Management Consulting (Shanghai) Co., Ltd. 2801-12, 28th Floor, 100 Century Avenue, Shanghai World Financial Center, Shanghai Pilot Free Trade Zone, 200120, China, a Chinese limited liability company regulated to provide financial management consulting services.; Japan – MFS Investment Management K.K., is registered as a Financial Instruments Business Operator, Kanto Local Finance Bureau (FIBO) No.312, a member of the Investment Trust Association, Japan and the Japan Investment Advisers Association. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks, including market fluctuation and investors may lose the principal amount invested. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

MFSE-FLY-845184-6/21

48607.1