Since taking over as chair of the federal Reserve earlier this year, Janet Yellen has sharpened the central bank’s focus on the second part of its dual mandate: promoting full employment. The question of how much labor slack exists, and thus how much longer the Fed can maintain zero rates, is the biggest uncertainty that the bank — and investors — now face.

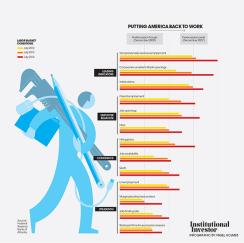

Leading indicators have shown the biggest improvement since the crisis. The number of people working through temporary placement agencies has risen well above the prerecession peak level of December 2007, as has the percentage of companies reporting openings they can’t fill. Measures of employer behavior, including payroll employment, also stand near or above prerecession peaks. But other gauges continue to lag, including two key confidence measures tracked by the Fed and two utilization measures Yellen often cites: marginally attached workers, or people discouraged from looking for jobs, and those working part-time because they can’t find full-time work. Figuring out when these measures add up to a rate hike is a full-time job for investors.