Erik Norland, CME Group

AT A GLANCE

- Tight monetary policy aims to slow down an overheated economy by increasing interest rates.

- Conversely, loose monetary policy aims to stimulate an economy by lowering interest rates.

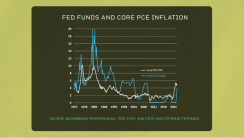

Global central banks have raised rates rapidly but their rates are still below inflation levels

Over the past eight months, central banks have been tightening policy quickly. But is monetary policy actually tight, or is it still loose?

This may sound like an odd question. The Fed has raised rates by nearly 400 basis points since March. That’s its fastest pace of tightening over any eight-month period since 1981. The Bank of England has raised rates by nearly 300 basis points, its quickest pace of tightening since 1989. And the European Central Bank has raised rates by 200 basis points in the past four months, its most rapid pace of tightening in the ECB’s 23-year history.

But while central banks have raised rates a great deal, their rates are still way below inflation. In the United States, the federal funds rate is now just below 4%. But core PCE inflation is running at 5.1%. This puts fed funds at -1.2% in real terms.

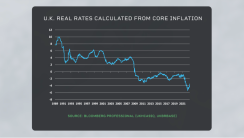

In the United Kingdom, the BoE has rates at 3%, but core inflation is 6.5%. This puts real rates at -3.5%. Likewise, the ECB has rates at 1.5%, but core inflation is at 5.1%. That’s a -3.6% real rate of interest.

Can central banks bring inflation down without putting real rates into positive territory? I’m not sure that anyone knows the answer to this question, but it is possible that with real rates still in negative territory that monetary policy is actually still quite loose.