")

In the minds of many investors, the stock market is an inscrutable beast, wild and unpredictable. Yet the reality is that stock prices do follow regular cycles, the most important of which are linked to the economy.

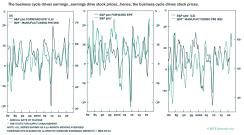

The accompanying chart shows that the business cycle drives corporate earnings, while corporate earnings, in turn, usually dictate the path for stocks. In short, macroeconomics is arguably the most important determinant of equity returns.

This fact leads to what I call the “Golden Rule for Stock Market Investing.” It simply says, “Stay bullish on stocks unless you have good reason to think that a recession is around the corner.”

The evidence for this is strong. During the past 50 years, except for two occasions, the S&P 500 has never fallen by more than 20 percent outside of a recessionary environment. The only two exceptions were the brief but violent 1987 stock market crash and last week’s selloff, which saw the S&P 500 briefly fall into bear market territory.

If history is any guide, stocks will rally during the remainder of the year — provided, of course, that the economy doesn’t fall into a recession.

But can a recession be averted? That’s the trillion-dollar question. While recessions are notoriously difficult to predict, they typically don’t just come out of the blue, either. Most recessions result from the buildup of imbalances in the economy — imbalances that are usually laid bare by tighter monetary policy.

Today, the U.S. private sector finds itself in reasonably good shape. The so-called financial balance — the difference between what the private sector earns and what it spends — is in surplus to the tune of 3 percent of GDP. In the lead-up to both the 2001 and 2008 recessions, the private-sector financial balance was in deficit. This made it necessary for many firms and households to cut spending when the economy turned down.

Granted, inflation is very high, and if it remains high, the Federal Reserve will have no choice but to raise rates to punitive levels. This could cause a recession.

Our guess, however, is that inflation will come down quite rapidly over the coming months.

Overall spending in the U.S. is broadly in line with its pre-pandemic trend. What is out of line is the composition of spending. Outlays on goods remain far above trend, while outlays on services remain far below. Companies selling fitness equipment raised prices, but gyms, figuring that the pandemic shock was temporary, did not cut prices. This asymmetry, along with various supply-chain disruptions, has fueled inflation in the prices of goods.

As the pandemic recedes, spending will shift from goods to services, and supply-chain bottlenecks will ease. An influx of lower-skilled workers, many of whom have been slow to reenter the labor force, should also help keep a lid on labor costs.

As inflation comes down, the Fed will breathe a sigh of relief, patting itself on the back for something that probably would have happened anyway. Stocks will rally.

Matters are more complicated outside the United States. Europe has been badly hit by higher energy prices. China is grappling with a major Covid outbreak and a floundering property market.

These problems are real, but they’ve arguably been fully discounted by financial markets. European stocks are currently trading at 13 times forward earnings. Chinese stocks trade at only 11 times forward earnings.

It’s not difficult to envision a scenario later this year in which European growth rebounds once a detente in the Ukraine war is reached. Meanwhile, China is almost certain to shower its economy with stimulus money in the lead-up to the 20th Party Congress this fall.

How long will this Goldilocks period for the global economy last? Our guess is about 12 to 18 months. As inflation declines, real wages — which are now falling in the major advanced economies — will start to rise. Stronger real income growth will boost consumer spending. Inflation will probably reaccelerate in early 2024, forcing the Fed to start raising rates again.

The last hurrah for stocks is coming, but investors would still be wise to keep one eye on the exit.

Peter Berezin is currently BCA Research’s Chief Global Strategist and Research Director. BCA is a global independent research provider owned by Euromoney Institutional Investor.