By Erik Norland, CME Group

AT A GLANCE

- In each of the last three rate increase cycles, the Federal Reserve wound up hiking rates much more than traders anticipated

- With inflation near 7%, conditions could be right for another larger than expected increase in 2022

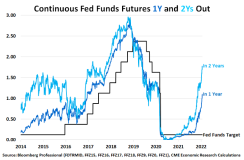

Fed Funds Futures now price four rate hikes in 2022 and three more in 2023. But how accurately have Fed Fund Futures anticipated what the central bank actually did during past rate tightening cycles?

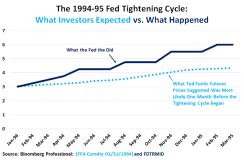

Let’s look at the past three tightening cycles starting with the one in 1994-95. In January ‘94, investors thought that the Fed would most likely raise rates by 125 basis points to about 4.25% percent. Instead, the Fed raised over twice as much, putting rates at 6%.

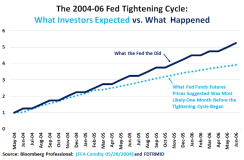

Fast forward a decade to 2004 when investors thought the Fed would most likely hike rates from 1% to 4% by mid-2006. But the Fed went further, hiking rates to 5.25% by June ‘06.

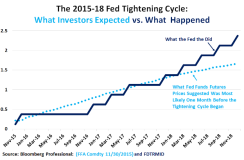

Finally, late 2015 markets thought that the Fed would hike slowly and steadily until it got to around 1 5/8% by the end of 2018. That time the Fed hiked more slowly than expected in 2016 but then did much more than expected in 2017 and ‘18, bring rates to 2 3/8%.

All three times, the Fed wound up hiking much more than traders initially anticipated. There are both upside and downside risks to the current scenario in pricing Fed Funds futures. But with inflation at 7% and unemployment below 4%, it’s difficult to exclude a scenario in which the Fed once again raises rates more than investors anticipate.

Read more articles like this at OpenMarkets