The Global Financial Crisis of 2007-2008 and the current COVID-19 pandemic invite comparison with the Great Depression and global influenza crisis of the first half of the 20th century. So is it farfetched to suggest that the world could be in for an extra dose of optimism and progress in the 2020s – much like what occurred in the 1920s? A report from the research team at Nuveen Real Estate makes a compelling case for this, while also examining key negative factors that could spoil the party.

Why the 1920s prospered

The Roaring 1920s saw many long-brewing societal and technological trends come to fruition, ushering in an era of prosperity. The use of electrical power exploded, transforming households as well as factories and transportation. New technologies allowed the world to integrate, with commercial flights, radio, film, and advertising establishing the modern consumer economy. Society was also transformed, foremost through the liberation of women.One of the primary drivers of the Roaring 1920s was an economic expansion led by real estate. New York’s famous skyline is a product of the 1920s and was made possible by new building techniques that used steel and elevators. Life became increasingly urban. Department stores revolutionized retail shopping, with automobiles and public transit shuttling people from apartment blocks and new suburban homes to offices and industrial buildings. Modern architecture was born with Walter Gropius’s Bauhaus school in Germany and Le Corbusier in France. It fully bloomed with Ludwig Mies van der Rohe, Frank Lloyd Wright, and others in the U.S. And even though Asia was still restrained by European colonialism, the Great Kantō earthquake (1923) destroyed much of Tokyo and kickstarted a building and modernization boom of such speed that by the end of the decade Tokyo rivaled London and New York for the race to become the biggest city in the world.

Why the 2020s could boom

Is the investment world primed for a real estate-driven Roaring 2020s? Analysis from Nuveen Real Estate’s research team made the case both for and against. Here are five reasons why they could roar.1. A Relief Bounce for Retail and Travel?

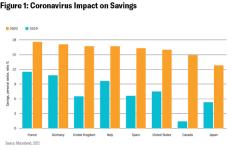

Glimmers of pent-up demand began to appear during the summer months of 2020, with shopping centers and popular brands reporting large queues and the need for crowd management. This was short-lived – infections surged once more, stores had to reclose, and lockdown measures resumed.Despite increased inequalities between socio-economic groups in 2020, many consumers felt far better off than previously. Spending on commuting costs, leisure activities, and annual holidays plummeted. And savings ratios more than doubled in some countries (see Fig. 1), highlighting a spending pot that can be easily tapped to facilitate pent-up demand when the pandemic is under control by successful vaccination programs and consumer confidence returns. Demand for travel is likely to surge after 2020’s postponed and cancelled holidays and business travel, and as families long to reunite. The reopening of hospitality venues in greater numbers and larger audiences should help meet that demand and increase output from the sector. If the hospitality and retail sectors rise from the ashes, it may not look too different from the legendary 1920s parties.

2. Europe’s “Hamilton” Moment and America’s Re-Engagement

The €750 billion Next Generation EU recovery plan agreed to in July 2020 was unparalleled. For the first time, it allowed the EU to issue debt. Some analysts hailed the decision as Europe’s “Hamilton” moment, a nod to the U.S. founding father who federalized the nascent country’s war debt in 1791. If Next Gen EU will transform Europe to such an extent remains to be seen, but it certainly has brought the continent closer to political and financial unity than was previously conceivable, reviving a dream that had all but vanished in the last few years.The Eurobonds raised from capital markets will help member states address the pandemic’s economic and social impact while ensuring their economies undertake green and digital transitions to become more sustainable and resilient. This could have a considerable impact on Europe’s real estate sector. The European Commission recommends that renovating housing be one of the national recovery and resilience plans’ priorities. Such renovations could simultaneously help achieve the two European goals of ecological transition and digitalization of the economy through smart buildings that are more energy efficient.

One immediate consequence of the 2020 U.S. presidential election felt by those domestically and abroad was a return to predictability of U.S. federal policy and governance. The consensus is that this will positively impact both the U.S. economy and the real estate market. U.S. commercial real estate investors should benefit from more consistent political messaging and a greater chance of additional public investments.

3. The Rise of Real Estate Alternatives

The analysis by Nuveen Real Estate pointed to three significant trends – a continued shift towards renting, a transformation of healthcare systems and a rise in the digital economy – that could drive long-term outperformance in the alternative housing, healthcare, and technology real estate property types.In the U.S., the market value of institutionally owned alternative real estate grew by 23% year-over-year in Q3 2020 to $36 billion, according to NCREIF data. Despite this growth, alternative real estate sectors have a minor 12% allocation in most NFI-ODCE investors’ portfolios and less than 5% in Europe’s MSCI-type portfolios.

The alternative sectors are likely to become a mainstay in institutional investors’ portfolios during the next decade as investors realize, post-COVID-19, how much they need to increase diversification within their traditional real estate portfolios. During the pandemic, these sectors proved their resilience relative to most of the traditional real estate sectors.

Historically, these property types have outperformed traditional real estate sectors through economic cycles and have the potential to do so for the next decade. Much of the anticipated future outperformance of alternatives is driven by their stronger net operating income growth and lower capital expenditure requirements in alternative housing, healthcare, and technology real estate. In Europe in particular, it’s anticipated stocks of these sectors could grow to between 15% and 20% of the total within a decade. This implies that a substantial part of real estate construction activity will be in what is now called alternative real estate sectors, providing a huge investment opportunity likely to unfold around data centers, controlled environment agriculture, mobile phone towers, health care, research facilities and many new forms of residential.

4. Mega Investment Boom in Green Tech with the De-Carbonization of Global Building Stock

The 2020s should herald a shift in the global response to climate change and swift action to reduce emissions to ward off the worst impacts. This will include deployment of deep retrofits to existing buildings and innovative design and engineering solutions for new construction. This transformation will define the early 2020s. Governments will prioritize low-carbon buildings in pandemic recovery packages. Why? Decarbonizing the building and construction sector will not only slow climate change but also deliver strong economic recovery benefits. The research team at Nuveen Real Estate identified a few things to watch for:The Biden administration’s climate plan proposes accelerating and incentivizing improvements to energy efficiency in U.S. buildings, deploying clean technology and targeting a reduction in the carbon footprint of the U.S. building stock by 50% by 2035. In a similar vein, the EU recovery fund described above has prioritized build-back-greener projects, many with a strong connection to real estate. The adoption of strict building codes and training for builders and inspectors will create job opportunities through investment in green buildings, enabling stronger, more resilient communities.

Carbon pricing will boost the return on investment for improvements in energy efficiency, accelerating the adoption of net zero carbon strategies and shifting market preference toward low-carbon buildings. Carbon pricing also further stimulates clean technology and market innovation, fueling new low-carbon drivers of economic growth.

During the next decade, cities in emerging markets will be expanding at a fast pace to keep up with high population growth and rapid urbanization. Green buildings represent a significant low carbon investment opportunity in emerging markets, estimated by the IFC at $24.7 trillion by 2030.

Grid-interactive efficient buildings will become smarter about the amount and timing of energy use through technology. By making equipment more intelligent with next-generation sensors, controls, connectivity, and communications, building occupants will have more control in managing comfort and productivity while saving on energy bills and enhancing grid reliability and resilience by helping balance the supply of renewable generation.

Post-pandemic, occupant experience will be prioritized by landlords, and smart-connected buildings can improve occupant experience by providing transparency on healthy environments.

The smart-building trend will be accelerated in the early 2020s as landlords adapt to new normal tenant expectations for environmental performance and for health and safety (see Fig. 2).

5. A New Community Spirit

The widening gap between the haves and have-nots is an indicator of social and economic imbalances which have been evident for some time and which the pandemic has intensified. These include urbanization and isolation, automation, and the low carbon economy.People have realized that climate change is not going away and that crises like COVID-19 have a disproportionate impact on lower income communities. The social upheaval brought about by COVID-19 has the potential to accelerate the growth and prominence of impact investing in the built environment, with social impact increasingly being considered as part of an overall strategy. The real estate world has begun to evaluate its wider role in society more seriously – from diversity and inclusion in the workplace to a far greater emphasis on the environmental, social, and governance agenda.

As a result of this reassessment within the real estate sector, coronavirus could spur capital coming into real estate impact investment. The pandemic has highlighted the need for greater investment in social infrastructure – a broad term that includes such assets as modern healthcare facilities, care homes and senior living, affordable housing for key workers and specialist housing for vulnerable groups.

Urbanization and associated community and environmental issues are central to impact investing. Many teachers, healthcare professionals and emergency workers struggle to find affordable living near their place of work, making many urban areas less inclusive and less resilient.

Even before the pandemic, we saw a slow but steady increase in demand for impact products and the pandemic had further put these strategies on the radar of investors, according to the research team at Nuveen Real Estate. In addition, long-term institutional investors are now focusing on ways to meet sustainable development goal contribution targets that may soon be a regulatory requirement.

It’s not all rosy, however

While much of news is optimistic, the company’s analysis also identified key issues – including asset overvaluation, tax increases, inequality and others – that could bring more bust than boom to the current decade.Learn more about what might drive the Roaring 2020s – and what might make them a groaner.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature.

Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

Investing involves risk; principal loss is possible. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards.

Real estate investments are subject to various risks associated with ownership of real estate-related assets, including fluctuations in property values, higher expenses or lower income than expected, potential environmental problems and liability, and risks related to leasing of properties.This information represents the opinion of Nuveen, LLC and its investment specialists and is not intended to be a forecast of future events and or guarantee of any future result.

Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time.

Nuveen, LLC provides investment advisory services through its investment specialists.

This information does not constitute investment research as defined under MiFID.

GWP-1729001PR-O0821X

© 2021 Nuveen, LLC. All rights reserved.