By Suny Park, Chief Institutional Strategist, Janus Henderson Investors

Emerging markets equity (EME) exhibits the highest long-term expected return across the three public equity regions: U.S., non-U.S. and emerging markets. In fact, at the index level, EME is the only region that exceeds the long-term required rate of return (7% to 8%) of most U.S. institutional investors, and yet most U.S. investors have neglected their allocations to emerging market equities.

In what follows, we examined the current allocations to EME across different investor types and challenged the conventional practice of following the regional allocation as indicated by the MSCI All-Country World Index (ACWI). We challenged the conventional practice because, in our opinion, the latter may not achieve the required rate of return of most investors.

When examined across different types of investors, under-allocation to emerging markets is most pronounced for individual investors. The Yale, Harvard and Stanford university endowments – arguably three of the most sophisticated U.S. institutional investors – are at the other extreme of the allocation range to emerging markets. Their extreme overweight to emerging markets clearly indicates that they favor EME over U.S. and non-U.S. developed market equities in their strategic asset allocations. Their EME allocations “appear downright imprudent in the eyes of conventional wisdom”1 and when compared to the MSCI ACWI’s regional breakdown. What is so compelling about emerging markets equity that they would overweight the region so significantly, despite the perceived risk? Or, to put it another way, what do the Yale, Harvard and Stanford endowments know that the rest of the investment community is missing?

The Yale Endowment case study

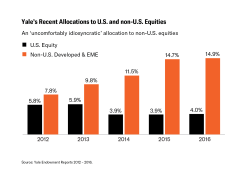

Because Yale is a leader among all institutional investors, it is useful to examine how its portfolio allocation came to look so different from traditional institutional portfolios. From 2012 to 2016, Yale roughly doubled its foreign equity allocation while simultaneously reducing its U.S. equity allocation, as shown below.

What is even more striking is the allocation difference between U.S. and emerging market equities. In 2016, Yale allocated 9% of its endowment assets to EME versus 4.0% in domestic equities. Yale CIO David Swensen and his team clearly favor emerging market equities over U.S. equities, even though the former is conventionally viewed as riskier than the latter. While Swensen notes that the Yale endowment represents the “most uncomfortably idiosyncratic portfolio,”2 we observe this same tilt toward EME among its nearest peers.

While renowned leaders in investing and active asset allocation, neither Yale nor its nearest peers are infallible. In fact, one could argue that Yale was too early in rotating into emerging markets equity from 2012 to 2016. The three endowments mentioned are not more clairvoyant than the rest of us regarding how the future will unfold. Yet, their asset allocation decisions appear informed and deliberate rather than haphazard. In the next section, we present a possible explanation as to why these leaders have staked such a sizable claim in EME.

Shiller P/E

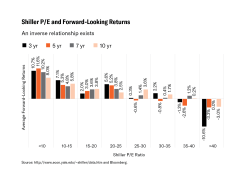

Currently, there is a fair amount of debate about whether U.S. equities are fairly valued or overvalued. Given the incredible run that U.S. equities have had since the depths of the financial crisis (up approximately 340% since the crisis low in February 2009), many find it hard to believe that U.S. equities are undervalued. An ongoing debate about the effectiveness of the Shiller P/E ratio in forecasting future equity returns notwithstanding, it is instructional to relate the current Shiller P/E ratio to the historical forward-looking returns, as well as to compare the Shiller P/E ratios across different regions.

Below you’ll see a comparison of the U.S. Shiller P/E ratio to the forward-looking returns from January 1881 to August 2017. To clarify the methodology, the chart relates the Shiller P/E ratio at a given point in time to the returns realized in the next three, five, seven and 10 years. For example, the Shiller P/E ratio of 44 at the end of 1999 is compared to the ensuing U.S. equity returns from 2000 to 2002 to estimate the annualized forward three-year return, returns from 2000 to 2004 to estimate the annualized forward five-year return, and so on. This process is repeated on a rolling monthly basis to estimate the average forward-looking returns for each Shiller P/E valuation bucket.

There are a couple of observations worth making: first, there exists an inverse relationship between the level of Shiller P/E ratios and the forward-looking returns; second, when the Shiller P/E ratio was between 30 and 353, the forwarding-looking returns for the next three, five, seven and 10 years were quite poor. When viewed cross-regionally, the emerging markets equity Shiller P/E ratio stood at about a 43% discount to that of U.S. equities. While not cheap, EME’s Shiller P/E of 16.5 seems much more reasonable than the 29.0 level for U.S. equities. We believe this valuation metric illustrates at least one of the reasons why the Yale, Harvard and Stanford endowments favor emerging market over U.S. equities.

However, a word of caution is in order. The Shiller P/E ratio is not meant to be a market timing signal, and we do not advocate using it as such. It provides a measure of relative value across different regions and across time, but it provides no information whatsoever as to when to get in or get out of equities.

To read the full brief, visit janushenderson.com.

1 “Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment” by David F. Swensen, pp. 8. Simon and Schuster, 2000, 2009.

2 “Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment” by David F. Swensen, pp. 8. Simon and Schuster, 2000, 2009.

3 We estimate the Shiller P/E ratio as of December 31, 2017, to be approximately 32.

The opinions and views expressed are those of the author(s) and are subject to change without notice. They do not necessarily reflect the views of others in Janus Henderson's organization and no forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector.