Illustration by Nicolas Ortega

Hedge fund performance has declined precipitously since the 1990s as assets under management have exploded. The managers are not solely to blame.

While alpha has withered, large institutional investors have piled into large hedge fund managers that are perceived to be safe — an industry transformation beautifully summarized by Blackstone Group:

The hedge fund industry undoubtedly includes many of the brightest minds in the investment universe. It creatively combines the use of equities, fixed income, commodities, derivatives, and private investments unlike any other segment of the investment landscape.

That being said, the value proposition of hedge funds is questionable today. Net of fees, the amount of alpha — or excess returns, adjusting for returns on cash and equity beta — retained by investors has been steadily declining over the last quarter century. This is an important measure as it clearly shows the value (or lack thereof) that hedge funds bring to the table in excess of investing in a passive combination of cash and an equity index. Looking at the alpha generated by hedge funds over four-year periods from 1990 to 2017, the downward trend is obvious.

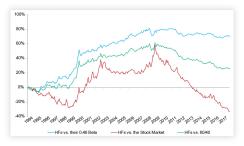

Cliff Asness of AQR Capital Management nicely illustrates the issue in a May blog post, “The Hedgie in Winter.”

Source: AQR Capital Management

Alpha generated by hedge funds has essentially been flat to slightly negative over the past decade, as per the blue line, which shows relative hedge fund performance versus a 46 percent exposure (beta) to stocks. Hedge funds did well from 1994 to about 2008 but have struggled since then. Hedge fund performance is worse compared to the full stock market (red line) as well as a 60/40 stock/bond portfolio (green line), but these are not appropriate comparisons, as Asness points out.

(AQR has calculated a beta of 0.46 since 1994 versus my 0.34 calculation since 1990. When determining the most accurate beta to use, note that Asness is smarter and funnier than me. However, I am better looking and my hockey team has won more Stanley Cups than his.)

This data suggests that over the last decade, investors could have replicated average hedge fund returns by putting roughly 40 percent of their assets into an equity index fund and the rest in cash. Brain power and liquidity must be sacrificed at the altar of hedge fund investing as well, compared to using index funds and cash. It’s not easy to recommend hedge funds unless you have meaningfully superior manager selection or portfolio-construction skills.

In the beginning — or, shall we say, starting in 1990, skipping the early history from 1949 to 1989 — the hedge fund industry managed just $39 billion in assets and less than $200 billion five years later, as per Hedge Fund Research. Most of this capital came from and was dominated by high-net-worth individuals and family offices. It is probably fair to say that they weren’t overly concerned with volatility or risk management or what the beta of a particular investment was.

With considerably fewer assets in the industry then — compared to $3-plus trillion today — the hedge fund industry delivered strong returns. There were a few bumps along the way, such as in 1994 (unexpected rate hikes by the Federal Reserve and issues with emerging markets) and in 1998 (Russia, Long-Term Capital Management). But hedge funds, by and large, kept bouncing back, recovering losses and delivering annualized returns of 18.3 percent in the 1990s, according to HFRI’s weighted composite index.. They performed roughly in line with the S&P 500 over the decade but with about half the volatility. The implied annualized alpha was 8.5 percent.

There were a few implosions during this time (such as the aforementioned Long-Term Capital Management), but investors who did their homework on both the investment and operational side could reasonably expect to avoid most of them. Joel Katzman, former CEO and CIO of J.P. Morgan Alternative Asset Management, described it this way in conversation: “It used to be that you could meet with a bunch of managers and one third could be considered interesting, one third were maybes, and one third you wanted to stay well away from. Now about 90 percent are maybes and only a handful look particularly interesting or particularly dangerous. The prime brokers have coached the poorer managers to look much better.”

Anecdotal evidence suggests that the standard fee schedule in the 1990s was closer to 1-and-20 than 2-and-20. The industry was still relatively immature, but alpha opportunities abounded.

What we now consider plain-vanilla strategies (or alternative betas), such as convertible arbitrage or merger arbitrage, prospered in the 1990s amid little competition. HFRI’s convertible arbitrage index had annualized returns of 11.7 percent from 1990 to 2000, versus 5.6 percent from 2001 to 2017, and its merger arbitrage benchmark delivered 13.1 percent from 1990 to 2000, versus just 4.3 percent since.

Starting with the endowments — led notably by Yale University CIO David Swensen, among others — institutional investors began increasing exposures to hedge funds in the late 1990s. The sector’s value proposition was clearly evident during the bursting of the dot-com bubble from 2000 to 2002. I call this period the golden age of active management. Long-only and long-short equity managers performed extremely well compared to the equity indexes by buying value stocks and avoiding or shorting overvalued tech names. While the HFRI Equity Hedge (Total) Index was up just 3 percent annualized from mid-2000 to mid-2002, this represents alpha of 5.8 percent over the S&P 500 after adjusting for a beta of 0.42 and a T-bill return of 4.2 percent.

Seeing the success of hedge funds through this downturn, pension funds began to significantly ramp up their hedge fund allocations over the next few years.

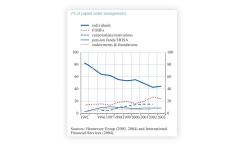

Hedge Funds’ Shifting Investor Base, 1992–2003

I remember worrying around this time that this increase in demand from institutional investors would put upward pressure on fees, making 2-and-20 more common. It did.

Total industry assets under management grew massively, from less than $500 billion in 2002 to $2.3 trillion at the end of 2007, as per BarclayHedge. I also worried, rightly so, as it turned out, that ballooning assets would usher in a meaningful decline in alpha generation. As the two charts above indicate, alpha has fallen precipitously over the last decade to just 0.3 percent, according to my calculations.

The popularity of funds of hedge funds flourished during this time as well — likely driven by new investors who felt underqualified to select individual managers or bought the funds of funds’ argument that hedge funds were too complicated for them. On top of the fees charged by underlying managers, funds of funds frequently charged 1-and-10 until the 2008 global financial crisis.

New institutional investors, on their own or via funds of funds, ramped up the investment and operational due diligence conducted throughout the industry. But their added scrutiny didn’t prevent high-profile implosions due to investment or operational failures, such as those of Amaranth Advisors, Lancer Group, and Bayou Hedge Fund Group. I thank the investment gods that I avoided these doomed firms in my early days of hedge fund investing.

The global financial crisis was obviously a very difficult period for market participants, and hedge fund managers were no exception. Without going into all of the gory details, the S&P 500 dropped 37 percent in 2008, while the HFRI Fund Weighted Composite Index was off by 19 percent. Assuming a beta of 0.37 for that year, these results imply alpha of roughly negative 7 percent.

Among the biggest news late in the year was the discovery of a gigantic Ponzi scheme orchestrated by Bernie Madoff — a fraud estimated at $64.8 billion.

My memories of that wrenching fall of 2008 center on the stress of worrying my investments would implode and on protracted, contentious negotiations with a couple of managers that needed help to survive. The dangerous triumvirate of illiquidity, directionality, and leverage was permanently drilled into my head. Nevertheless, I recognized that worthwhile long-term hedge fund investing demanded some risk-taking.

Interestingly, hedge funds were close to flat for the first two months of 2009, while the equity market fell steeply and didn’t bottom out until March 9. It appeared to be a good year for hedge funds as the HFRI Fund Weighted Composite Index gained a healthy 20 percent. One wonders if industry returns might have rebounded even more strongly absent the significant redemptions by investors fleeing or liquidating positions. Net assets invested in hedge funds fell almost $1.2 billion from mid-2008 to mid-2009, with redemptions estimated at more than $900 million. No doubt many investors crystallized their losses near the bottom of the market.

Funds of funds began their downward spiral in 2009. That segment of the industry contracted by more than 50 percent from mid-2008 to mid-2009. Over the decade ending in 2017, funds of funds went from almost half of the hedge fund market to less than 10 percent, according to BarclayHedge.

In my view, three central factors drove the fund-of-funds industry’s downfall.

First, funds of funds provided insufficient downside protection during the crisis. The HFRI Fund of Funds index fell 21.4 percent in 2008 versus 19 percent for the broader HFRI Fund Weighted Composite Index. Funds of funds lagged on the way back up in 2009 as well, gaining only 11.5 percent — an 850 basis-point deficit to the industry overall.

Second, the additional layer of fees became less palatable post-crisis.

Finally, many institutional investors — particularly pension funds that invested after the dot-com bust — had grown up by 2009. They’d gathered the confidence and the in-house expertise to select their own managers.

As the fund-of-funds industry shrank, it also began to consolidate. The relatively few funds of funds that prospered from 2009 onward tended to be either firms large enough to withstand fee pressure (such as Blackstone or UBS) or niche specialists (such as PAAMCO Prisma Holdings, which invests in and seeds emerging managers).

As institutional investors focused more on direct investing and less on funds of funds post-crisis, there was a resulting shift in the aggregate demand for hedge funds. With relatively less capital coming from family offices and funds of funds and more from large, crisis-scarred pension funds, these new power allocators sought strong risk management, tight operational controls, and robust compliance policies and procedures. Operational due diligence was deemed crucial in the post-Madoff world. As fiduciaries for their underlying beneficiaries, investment staffs at these institutional investors may have shifted their emphasis toward “safer” investments in an effort to avoid criticism. Combined with a raft of post-crisis regulations, barriers to entry went up and the costs of operating a fund rose correspondingly.

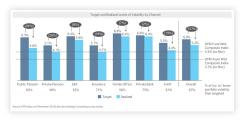

As evidence of institutional investors’ propensity to take on less risk, private pensions and insurance companies have had the lowest targeted and realized levels of volatility with their hedge fund investments, while family offices and private banks have had the highest, as the graph below from Barclays Capital illustrates.

2016 Hedge Fund Volatility Versus Targets

Institutions’ reluctance to invest in smaller or newer hedge funds is depicted well by the 2017 Barclays Capital chart below. As an example, pension funds and insurance companies only had 5 percent invested in managers with less than $500 million in assets, compared to 18 percent for family offices. Similarly, in 2017, 56 percent of family offices indicated that they were looking to increase their allocation to small managers, compared to just 20 percent for pension funds and insurance companies.

Investor Sentiment Toward Small/Emerging Managers

These larger managers became very profitable. In a paper, Barclays Capital found an average profit margin on management fees of about 50 percent for hedge funds (defined as product specialists, primarily focused on one main strategy) over $500 million. With margins this high, it appeared that managers’ incentives started to shift toward maintaining their client bases — not getting fired, in other words — as opposed to generating significant alpha for their clients.

As corroborating evidence of managers taking on less risk, the volatility of the HFRI Fund Weighted Composite Index fell from 7.1 percent in the period from 1990 to 2003 to 5.7 percent for 2004 to 2017. Undoubtedly, a significant driver of lower hedge fund volatility was the drop in overall market volatility, but manager behavior and incentives likely played a part as well. The relative volatility of the HFRI Fund Weighted Composite Index to the volatility of the S&P 500 fell from 47 percent to 43 percent over these periods. The early pitches I sat in on when I started researching hedge funds in 2002 emphasized absolute-return generation more so than recent pitches, which tended to highlight risk management.

Where We Are Now

Some changes to the industry eventually began to occur. A few high-profile investors like CalPERS and PGGM announced that they were divesting their hedge fund holdings. Low-cost smart beta (or alternative beta) strategies gained in popularity, often at the expense of hedge funds. The biggest ah-ha moment, though, was in early 2016. After a drawdown of 7.2 percent in the HFRI Fund Weighted Composite Index and seven losing months in nine, significant progress emerged on alignment of interests and fees. A number of hedge funds cut their fees (management and/or incentive), concerned with asset outflows and criticisms of the share of gross returns going to investors. In addition, interest in smaller managers seems to have picked up a bit. Yet much more work must be done to improve the value proposition of the industry.

The Problem, in Short

My high-level analysis of the current state of the hedge fund industry is as follows:

- The makeup of hedge fund investors shifted from return-seeking high-net-worth individuals and family offices to large institutions that had more modest return expectations and were more focused on risk management and diversification benefits.

- The demand for hedge funds by these large institutions altered supply-and-demand dynamics, pushing up fees and diluting returns.

- The focus on risk management and compliance by institutional investors resulted in a pickup in market share by larger firms that have the resources to address the requirements of these investors.

- Large hedge funds took advantage of the demand for their products by capturing significant profit margins from their management fees and reducing volatility to limit business risk.

- For investors, the biggest benefit has been a reduction in funds that have blown up or been involved in fraudulent activity. The biggest negative has been degradation in alpha received from their hedge fund investments.

What Investors Can Do

Investors can address the problem and improve their value proposition if they:

- Realistically assess what they can achieve via hedge funds and how they can win given their resources and abilities. If necessary, ensure the quality of the investment professionals researching hedge fund managers is sufficient.

- Stop chasing past performance.

- Take a skeptical view of a manager’s ability to replicate prior successes with higher assets under management.

Hedge fund managers can improve the industry and their clients’ experiences if they:

- Are intellectually honest. Don’t charge incentive fees on returns driven by cash or beta exposure.

- Emphasize alpha generation over asset gathering. Management fees should not be a significant source of profit. One percent management fees are appropriate for most managers over $500 million. That said, incentive fees over 20 percent may be acceptable if there is an appropriate hurdle in place. In fact, better-aligned fee terms can be revenue neutral to a manager if it hits its targeted gross returns. For example, if a manager believes it can generate 16 percent gross, it would do roughly as well with 1 percent management fees and 30 percent incentive fees with a 4 percent hurdle as it would with current common terms such as 1.5-and-20 and no hurdle.

- Don’t sell their firm to an outside organization that can change the culture that helped the firm get them to where they are today.

Besides investors and managers, regulators can also improve the hedge fund industry if they:

- Regulate sensibly by focusing on eliminating conflicts of interest.

- Are aware of unintended consequences of regulations.

David Finstad led the hedge fund investment programs at the Ontario Municipal Employees’ Retirement System and Alberta Investment Management Corp. He is currently a visiting researcher for Bodhi Research Group, and can be reached at dave.finstad@bodhiresearchgroup.com. This paper was inspired by conversations with Randy Cohen of Harvard Business School.