Major League Baseball’s playoffs are approaching, and I’m left with a vexing question. What does Billy Beane know that we don’t?

Billy Beane is the General Manager of the Oakland A’s and protagonist of Michael Lewis’ Moneyball. He spoke at a Goldman Sachs Prime Brokerage conference in 2012 and commented that data and analytics in baseball were becoming ubiquitous, and all his peers would soon be on equal footing. He predicted that the teams that make the playoffs five years hence would be the ones with the highest payroll, allowing them to pay for the players everyone agreed were the best in an efficient market for talent.

Change took longer than Beane anticipated. Sports Illustrated columnist Ben Reiter, who chronicled the worst-to-first story of the Houston Astros in the book Astroball, described in a recent episode of my Capital Allocators podcast how behavioral bias prolonged the adoption by teams of the new paradigm. Many teams clung to the old way of playing the game, suffering from availability heuristics off the field, such as talent scouts continuing to tout prospects that “look like” top ballplayers, and confirmation bias on it, such as when a pitcher gets angry when a hitter grounds a ball through an infield shift.

Nevertheless, Beane was mostly right. Ten teams of the thirty in baseball make the playoffs each year, and most of this year’s contenders paid a pretty penny for their roster. The A’s are a notable outlier, with a payroll ranking 28th out of 30 teams. Beane figured out something the rest of the teams don’t know. Maybe he gained insight into scouting players, developed a new analytical edge to assess the likelihood of player success, created new tactics on the field, or discovered subtleties in chemistry within the team. Whatever the A’s edge might be, I don’t know what it is.

Here’s the rub — no one else does either, not even their diehard fans.

The parallels with investing are apparent. Jim Simons’ Renaissance Medallion Fund has cracked the code on investment markets. All the other smart and hard-working competitors in the industry try to accomplish the same feat, but Renaissance is one step ahead, and only Jim knows how it’s done.

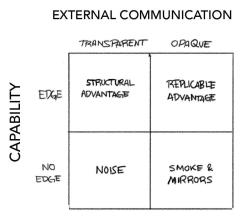

Acquiring an edge in investing is not easy. Building a business around that edge is even more challenging. Managers must tiptoe the line between disclosing enough to win new clients and maintain the trust of existing ones, and guarding their secrets enough to protect their lead over the competition. The following schematic describes the situation:

Billy Beane and Jim Simons have insight that probably can copied by competitors, who in turn would erode the edge if it were revealed. It makes sense that they need to be somewhat opaque with their trade secrets. Other asset managers, like Vanguard, have a structural advantage. Vanguard’s scale is not replicable by others, so they can discuss the benefit of scale openly without jeopardizing their ability to be the low-cost provider of index funds. A manager who is transparent but has no edge creates little more than market noise (and probably should find a different profession).

Most edges in markets are ephemeral, but on rare occasions investors figure out how to create more durable advantages. When David Swensen wrote Pioneering Portfolio Management in 2000, few institutional investors at the time understood the value of adding venture capital, private equity, and hedge funds to their portfolios. Swensen, of course, is the chief investment officer of Yale University’s investment office, where I started my career.

One way or another, eventually word would get out, capital would flow into talented managers, and competition for capacity would increase. In writing his seminal tome, Swensen may have sped up that dynamic and shortened the window of time during which Yale and a few other peers had the world as their oyster to source great managers in alternatives.

At the same time, by sharing Yale’s innovative model, Swensen elevated Yale’s reputation to create a structural advantage that has lasted eighteen years and counting. Swensen made Yale’s investing approach a global brand, cultivated Yale as a favored client by managers, and engendered deep loyalty among his client base (the University and its alumni). That status has enabled Yale to command favorable terms on its investments, which enhances bottom-line returns and promotes a positive flywheel for the investment program.

Yale has continued to post returns at the top of an industry that he made more competitive through the publishing of his book. I imagine Yale figured out some additional, replicable advantages along the way, but I wouldn’t hold your breath waiting for the pre-release of Pioneering Portfolio Management 2.0.

The bottom-right corner of the matrix is problematic. If opacity signals a competitive advantage, it behooves a manager without an advantage to profess that they have one. The challenge for allocators is to distinguish between an alpha generator and a poser.

In a world in which transparency has become an institutional imperative, this framework manifests an unfortunate result for active management. Most structural advantages are tied to scale or brand, so a winning competitive strategy for managers in a world that demands transparency is to grow assets under management. Is it any wonder that assets in alternatives are increasingly getting concentrated in the hands of a few managers?

Investors allocating to these managers should recognize that they have embraced the comfort of a crowd. Their returns may be satisfactory relative to objectives but are unlikely to be outsized. Instead, allocators may need to embrace managers with more opaque, replicable advantages to generate returns in a more challenging environment. Entering an investment that incorporates aspects of known unknowns can be uncomfortable for allocators and their governance boards. Indeed, successful investing is uncomfortable, and this is one example.

I wish I knew what Billy and Jim do. But I never will.