By Pierre Couture, A.S.A., E.A., M.A.A.A., Senior Actuary and Portfolio Manager and Virginia O’Kelley, CFA, Private Credit Portfolio Manager

Executive Summary

- Regulatory and market conditions are encouraging more corporate plan sponsors to de-risk.

- This de-risking trend coupled with a potentially smaller universe of long corporate bonds is causing the portfolios of many traditional long duration managers to look exceedingly similar.

- Against this backdrop, plan sponsors using multiple long duration managers could be overexposed to a handful of corporate issuers, leaving plans more vulnerable to volatility and funded status deterioration.

- We believe alternative asset classes like investment grade private credit represent an attractive way for plan sponsors to expand the opportunity set for liability-hedging assets and reduce issuer concentration risk.

The potential for investment volatility is a significant concern of corporate plan sponsors in today’s market environment. Yet sponsors seeking to implement traditional de-risking strategies across multiple benchmark-oriented managers are potentially overexposing their pension plans to issuer concentration risk that can exacerbate volatility.

To combat the effects of concentration risk, most pension plans have taken the traditional approach and diversified across multiple long duration managers in their long duration portfolio. However, demand for long corporates is likely to grow as current regulatory and market conditions encourage more plans to de-risk, leaving plans still potentially exposed to issuer concentration even with a diversified manager roster. Investors are also faced with a potentially smaller universe of corporate bonds. Against this backdrop, the portfolios of many traditional long duration managers can look exceedingly similar.

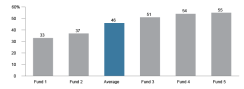

An analysis of the five largest actively managed long duration managers in Morningstar’s U.S. Long Term Bond category reveals that the top 20 corporate issuers in each portfolio represent, on average, nearly 50% of the portfolio’s corporate exposure (Figure 1). In addition, while the average issuer overlap of these top 20 holdings is only 26%, a closer look at the market value of the bonds issued by the same corporations shows that the largest long duration managers share heavy concentrations in a very small subset of corporate issuers. For example, the market value of bonds issued by corporations that appear in at least three of these five long duration portfolios represents an average of 51% of each strategy’s total credit exposure.

Figure 1. The Largest Long Duration Managers Are Heavily Exposed to a Small Subset of Corporate Issuers

Top 20 Corporate Issuers: % of Total Corporate Exposure (market value)

Source: Voya Investment Management and Morningstar Direct. As of December 31, 2017. Funds chosen for this analysis represent the five largest actively managed funds (by asset size) in the U.S. Long Term Bond category.

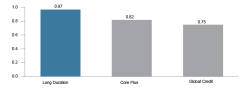

Figure 2. The Historically High Correlation of Long Duration Strategies

Average Correlation vs. Managers: 10 Years Ending 12/31/17

As of December 31, 2017. Source: Voya Investment Management and eVestment. Data represents average correlation versus other managers for the eVestment Long Duration Fixed Income, Core Plus Fixed Income and Global Credit categories.

Given this issuer concentration risk, we believe that investors should not view long duration like other fixed income allocations. Unlike other strategies, optimal diversification in the long duration space cannot be achieved by allocating to multiple benchmark-oriented managers. Figure 2 provides additional evidence, showing that the correlation of managers in the long duration universe is significantly higher than other asset classes.

Faced with these market realities, we believe the most effective way for plan sponsors to safeguard against volatility and reduce issuer concentration risk is to incorporate alternative asset classes into long duration portfolios.

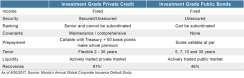

Investment Grade Private Credit Can Enhance Issuer Diversification

Most plan sponsors view private credit only through the lens of below-investment grade mezzanine debt. However, this is only a subset of the asset class. Issuance in the investment grade private credit market is roughly $60–$65 billion annually. Figure 3 highlights the differences between the asset classes.

Investment grade private credit can help plan sponsors enhance the issuer diversification of their long duration credit exposure. Only 3.4% of investment grade private credit1 issuers overlap with issuers in the Bloomberg Barclays Long Corporate Index. In addition, only two private credit issuers also appear in the top 20 issuers of the five largest long duration strategies highlighted in Figure 1.

Life insurers, the primary market participants in the investment grade private credit market, have long embraced the asset class as an essential component of their “core” fixed income allocations—and for good reason. Yields for investment grade private credit are higher than for public bonds with the same rating and maturity and from the same sector. They typically have been 20–100 basis points higher but are closer to the lower half of the range in the current low spread environment.

Figure 3. Investment Grade Credit: Public versus Private

Tracking Error Now, Protection Later

Covenant protections also give private bond holders more robust rights than are available in the public bond market. Private bond covenants often limit the ability of other creditors to assume a more senior position and provide for prepayment fees, thereby offering investors structural protection, and some comfort that bonds will continue to provide a steady yield until maturity (or will provide compensation if redeemed earlier). Compared to public bonds, private credit also allows investors to take a more proactive and informed role with meaningful representation in deal structuring and workouts. As a result of these characteristics, investment grade private credit has exhibited significantly higher recovery rates versus public bonds.

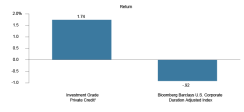

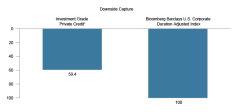

Investment grade private credit has also delivered better risk-adjusted returns and downside protection compared to public bonds. As Figure 4 highlights, this is especially true during periods of extreme investment volatility, making the asset class particularly attractive for plan sponsors concerned about market turbulence going forward.

Given current spread levels for investment grade public credit and the impending turn in the credit cycle, we believe investment grade private credit provides even more attractive relative value in long duration portfolios. Having said that, it is important to be aware that adding private credit investment grade bonds may slightly increase the portfolio’s tracking error to the liability in normal times. It will depend on how the sector and sub-sector allocations of the bonds in the portfolios compare with those used to create the Aa-rated corporate bond yield curve used to calculate the liability value. However, as shown in Figure 4, during periods of low spreads and potentially increasing downgrade and default risks, having bonds with strong covenants that provide much higher recovery rates will produce better returns than a portfolio with just public bonds. As a result, since the liability can neither default nor get downgraded, we believe a corporate bond portfolio that includes investment grade private credit should produce returns that better match those of the liability.

Conclusion

For plan sponsors who believe they are gaining diversification by using multiple benchmark-oriented managers, the issuer concentration risk highlighted in this paper creates the potential for unexpected outcomes. Going forward, the trends contributing to issuer concentration are likely to accelerate, as more plans look to de-risk and seek high-quality, long duration public credit.

Against this backdrop, we encourage plan sponsors to look at credit risk and issuer concentration holistically across their entire liability-hedging portfolio. For plan sponsors who find unacceptable levels of concentration, we believe investment grade private credit is a compelling solution. Accepting some deviations versus the bonds in traditional long duration benchmarks for the potential to protect funded status in periods of volatility is a tradeoff we believe most plan sponsors would be willing to make.

Figure 4. Protecting on the Downside: The Benefits of Private versus Public Investment Grade Credit

Financial Crisis: Peak-to-Trough (September 2007 – March 2009)

Source: Voya Investment Management and Bloomberg Barclays. Represents the time period September 1, 2007 through March 31, 2009. The Bloomberg Barclays

U.S. Corporate Duration-Adjusted Index is the U.S. Corporate Index published by Bloomberg Barclays that is adjusted to have duration identical to that of a representative private credit portfolio.

1 Given the limited availability of private credit market data, investment grade private credit information is represented by the Voya Private Credit Investment Grade composite.

Disclosures

The Bloomberg Barclays U.S. Corporate Duration-Adjusted index includes both corporate and non-corporate sectors. The corporate sectors are industrial, utility and finance, which include both U.S. and non-U.S. corporations. The non-corporate sectors are sovereign, supranational, foreign agency and foreign local government. The index does not reflect fees, brokerage commissions, taxes or other expenses of investing. The index has been adjusted for duration to reflect a value that is more representative of the private credit universe. Investors cannot directly invest in an index. Source: Bloomberg and Voya Investment Management.

Principal Risks

All investing involves risks of fluctuating prices and the uncertainties of rates of return and yield inherent in investing.High-Yield Securities, or “junk bonds,” are rated lower than investment-grade bonds because there is a greater possibility that the issuer may be unable to make interest and principal payments on those securities. The strategy may use Derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses and have a potentially large impact on performance. Foreign Investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic. Risks of foreign investing are generally intensified in Emerging Markets. As Interest Rates rise, bond prices may fall, reducing the value of the share price. Debt Securities with longer durations tend to be more sensitive to interest rate changes. Other risks include but are not limited to: Credit Risks; Other Investment Companies’ Risks; Price Volatility Risks; Inability to Sell Securities Risks; and Securities Lending Risks.

Important Information

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations, and (6) changes in the policies of governments and/or regulatory authorities.

Voya Investment Management Co. LLC (“Voya”) is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) (“Act”) in respect of the financial services it provides in Australia. Voya is regulated by the SEC under U.S. laws, which differ from Australian laws.

This document or communication is being provided to you on the basis of your representation that you are a wholesale client (within the meaning of section 761G of the Act), and must not be provided to any other person without the written consent of Voya, which may be withheld in its absolute discretion.

Past performance does not guarantee future results.

©2018 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169 • All rights reserved.

For qualified institutional investor use only. Not for inspection by, distribution or quotation to, the general public.