By Matt Toms, CFA, Chief Investment Officer, Fixed Income

Our semi-annual themes provide a framework for our investment decisions. Our holistic view of the economy and global monetary policy helps determine the overall risk budget and portfolio positioning to capitalize on relative value across sectors, while helping inform our bottom-up security selection process.

As we reach mid-year 2018, the economic backdrop remains supportive for the fixed income markets. However, the unwinding of accommodative developed market monetary policy, compressed risk premia and increased geopolitical uncertainty portend muted returns and increased baseline volatility. This environment favors assets that can withstand episodic spikes in volatility.

Investment Themes

Developed Markets Growth: Growth rates remain intact but are diverging. After a soft patch, U.S. growth will reaccelerate on tax reform, deregulation and fiscal spending. European growth will remain above trend but decelerate on slowing exports and supply-side constraints.

Emerging Markets Growth: Prospects are mixed. DM central bank actions will expose vulnerabilities, but these will be contained due to attractive potential growth rates within EM economies and lead to idiosyncratic opportunities.

U.S. Inflation will rise moderately as productivity gains and greater labor participation offset skill shortages and waning disinflation from globalization. This will allow the Federal Reserve to continue quarterly rate hikes until reaching the neutral rate, when it will become more data-dependent in 2019.

Global Central Banks: The European Central Bank (ECB) will scale back overly easy monetary policy; the Bank of Japan (BoJ) will stay ultra-easy. The ECB will stop expanding quantitative easing, to ensure policy flexibility and credibility as it prepares for leadership transition.

U.S. Dollar: Higher interest rate differentials and stronger growth support near-term strength. Persistent U.S. debt issuance and a less accommodative ECB will limit dollar appreciation.

Corporate Credit: The fundamental backdrop remains solid with the credit cycle turn still beyond the horizon. Faster economic growth will support revenues and profits despite higher production costs.

Bond Market Outlook

Global Rates: ten-year U.S. Treasury yield stays range-bound, 2.75–3.00%, yield curve flattens; German 10-year bunds return to their prior 0.50–0.75% range, rate increases will correlate with expectations of higher U.S. rates

Global Currencies: U.S. dollar strengthens vs. yen, ECB actions limit appreciation against euro

Investment Grade Corporates: earnings and valuations are supportive, but interest rate and technical headwinds remain

High Yield Corporates: valuations offer few opportunities but fundamentals remain sound

Securitized Assets: outlook brightens for floating-rate, securitized credits such as ABS and CLOs

Emerging Markets: U.S. dollar strength, higher U.S. rates remain headwinds; bias towards local rates on solid country fundamentals

Global Growth Divergence

Heading into 2018, global growth was advancing full speed ahead, boasting signs of strength and synchronization across developed and emerging markets. Six months later, the narrative remains positive overall but divergent. Starting with the U.S. economy, after a modest slowdown in the winter, growth is on track to exceed 4% for 2Q18.

We believe this robust growth in the United States will continue, driven by tax reform, deregulation and fiscal spending. A slew of strong economic data further supports this: the May retail sales print came in at its highest pace in six months as U.S. consumers took advantage of tax cuts, while the unemployment rate continues to tick down. Additionally, inflation remains under control despite upward pressures from labor skill shortages and the fading disinflationary effect of globalization. While we expect it to eclipse the Fed’s 2% target later this year, we believe inflation will remain tethered to this range as productivity improves and the labor participation pool increases.

While the U.S. is setting the pace, the divergence in global growth begins with Europe. After heady expectations leading into 2018, growth remains above trend but has moderated from its peak. One can see glaring evidence of this through the euro, which has been on a near free fall versus the dollar since its peak in February. What’s more, economic data has been softer as of late as PMIs continue to tick down. We expect growth to continue to decelerate as exports slow, the political turmoil in Italy continues and labor strikes degrade any chances of supply side reform in France.

Meanwhile, the picture for emerging markets (EM) growth is mixed. Business investment and retail sales data show signs of slowing in China, and pockets of idiosyncratic risks remain driven by trade and political uncertainties. With that said, growth remains solid across many emerging economies and any volatility that stems from developed market central bank decisions will lead to potential opportunities for investors, while exposing the most vulnerable EM markets.

Central Bank Divergence

Similar to the global growth story, we have begun to see a true divergence in global central bank policy as well. As expected, the Fed raised short-term rates another quarter-point at June’s Federal Open Market Committee (FOMC) meeting. We believe the aforementioned upward trend in inflation will allow the Fed to continue with quarterly rate hikes, including two more this year, until reaching the neutral rate, at which point it will pivot to a more data-dependent response in 2019.

While the Fed continues down its tightening path, the ECB and BoJ have stayed the course of easy monetary policy. The ECB announced in June its intention to end bond purchases, but maintained a dovish outlook by saying it would hold interest rates steady through next summer. We expect the ECB to cease buying bonds at the end of the year in order for Draghi to gain necessary monetary policy flexibility and market credibility.

Despite this announcement, interest rate differentials remain high as the yields on German bunds have stayed relatively stagnant, while U.S. rates tick higher across the curve due to Fed hikes and increased funding needs. This, coupled with stronger relative growth in the U.S., has led to a stronger U.S. dollar; however, we believe further dollar strength is limited due to concerns over persistent U.S. debt issuance and our expectations of a less accommodative ECB.

Outlook and Positioning

The underlying macro environment remains broadly supportive of fixed income markets. However, as developed market central banks unwind their accommodative policies, valuations remain full and threats of trade war continue to lead to heightened uncertainty, the potential for outsized returns is modest. Furthermore, the baseline case for volatility has increased and expectations for future volatility spikes will persist.

Figure 1. European GDP and Industrial Production, Quarter-over-Quarter Percent Change

Source: FRED Economic Research, as of June 2018

Figure 2. Historical and Projected Central Bank Policy Rates

We remain constructive on corporate credit given the solid fundamental backdrop driven by higher nominal economic growth, and our belief that a turn in the credit cycle remains beyond the horizon. Further supporting our view is the continued responsible corporate trends demonstrated by management teams, as aggressive acquisitions and leverage have yet to increase meaningfully, particularly among issuers in the loans and high yield markets. Within corporate credit, we favor senior loans due to their floating-rate structure and to a lesser extent high yield given its more U.S.-centric nature, over investment grade corporates.

Finally, we believe periods of uncertainty and volatility will provide attractive idiosyncratic opportunities within emerging markets. Therefore, we hold a tactically positive view and look to capitalize by allocating to countries whose fiscal standings will best benefit from the stronger growth picture such as Russia and Indonesia, while avoiding those with increased downside potential such as Turkey and Venezuela. We favor sovereign risk, both local and hard currency, over EM corporates.

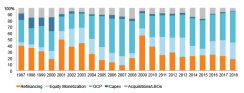

Figure 3. Use of Proceeds among High Yield and Senior Loan Issuers

Past Performance does not guarantee future results.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations, and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

©2018 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169 • All rights reserved.