Trade tensions, rate rises, and dollar appreciation have combined to cloud the outlook for emerging market (EM) equities. And, after a long period of strength, the tide appears to have turned as far as flows are concerned. After gathering €16 billion in assets in the past two years, outflows began in May and appear to be accelerating.

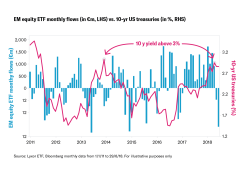

Higher yields in safe haven assets such as treasuries can make EM equities appear less worth the risk – to the extent that flows in or out of EM equity ETFs tend to be inversely correlated to the 10-year US treasury yield (albeit not perfectly). The last time rates were near 3% – during the “Taper Tantrum” of 2013 – we saw outflows of around €6 billion from February 2013 to February 2014. Now that the 10-year yield has passed 3% again, the outflows are becoming significant – €500m left these markets in May after 15 successive months of inflows. That was followed by €1.6 billion in June – and there’s every sign this will continue should yields continue their climb.

Rate rises = reallocations

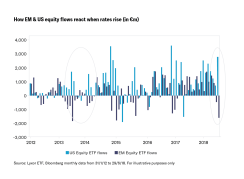

When US interest rates rise investors tend to shift their portfolios away from EM equities and into US equities. We saw outflows of around €6 billion from EM equities during the “Taper Tantrum” while inflows into US equities were very similar. All things being equal, that trend could continue. We’re not saying it should however; there are other options available to those less inclined to follow the herd. Asia for example presents pockets of opportunity – provided you know where to look.

Navigating Asian markets

Those areas of opportunity do not mean that Asia has escaped the EM malaise – far from it. Outflows have been accelerating and the markets are now below their January performance highs. But for all the external vulnerabilities, Asia’s fundamentals look underpriced, particularly as earnings growth expectations are robust and profitability is improving. The region’s exporters could be at risk from any moderation in global growth, but its domestic-focused markets offer some insulation from those issues, hence our preference for India over markets such as Taiwan and Korea. Here’s what we think is next in Asia:

- India: Domestic money is the key driver of equity markets despite the pressure of rising oil prices, meaning Indian equities are now less correlated to EM peers. The earnings outlook is strengthening, and the worst of the bad bank loans cycle is behind us. Forthcoming general elections (April-May 2019) are a wild card, as are global liquidity risks. Neither should prove too disruptive for now.

- View our Lyxor MSCI India ETF

- China: We’re positive on onshore equities because they are less correlated with other Asian markets, reasonably valued (we’ve seen earnings upward revisions in recent months) and offer exposure to domestic consumption. We also believe trade tensions and tariffs will be manageable.

- View our Lyxor Fortune SG MSCI China A ETF

- ASEAN: The bloc, most notably Indonesia and Thailand, also offers some insulation from US- and Europe-related risks. Reasonable valuation, recovering capex, and improving bank balance sheets augment the appeal.

- View our Lyxor MSCI Indonesia & Lyxor Thailand ETFs

- North Asia: We’re more cautious on the prospects for North Asian exporters such as South Korea and Taiwan. They are especially vulnerable to escalating trade tensions or an Italy-led euro crisis.

- Japan: The short-term case for Japan isn’t as strong as it was given yen upside risk and cabinet entanglement in political scandals. But the missing element in the long-term reflation case – wage growth acceleration – is (slowly) materializing.

- Sectors: The domestic earnings cycle remain strong and favours the consumer and financial sectors.

Why choose Lyxor for Asian equities?*

- 12 ways to access emerging Asia

- $3.2bn in AUM

- The cheapest EM Asia and physical China A Shares ETFs on the market

- The oldest and largest India ETF on the market

- 12+ years' experience managing single country and regional EM equity ETFs

To read the full brief, Visit janushenderson.com.

Disclaimers:

For professional clients only. All views & opinion are sourced Lyxor Cross Asset, Lyxor ETF & SG Cross Asset Research teams as at 13 July 2018 unless otherwise stated. Past performance is no guide to future returns.