By: Erik Norland

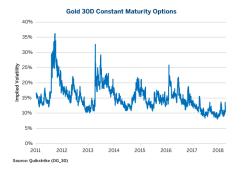

Twice this year implied volatility in gold options spiked from 9% to around 13.5%. Proportionally, that represents a 50% rise and seems like a big move, at least by the standards of recent history. What is more remarkable, however, is how calm the gold market has generally been. For the past two years, implied volatility on gold options have been near the lowest levels in recent memory and are a far cry from the 17% average levels that prevailed in 2015 and 2016, much less the spikes above 30% in 2011 and 2013 (Figure 1). So why has the gold market been so placid and what will likely drive volatility?

Figure 1: Implied Volatility on Gold Options Doesn’t Get Much Lower Than This.

Opposing Monetary and Fiscal Forces and Gold Prices

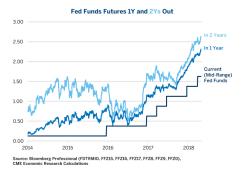

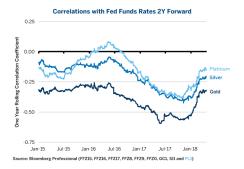

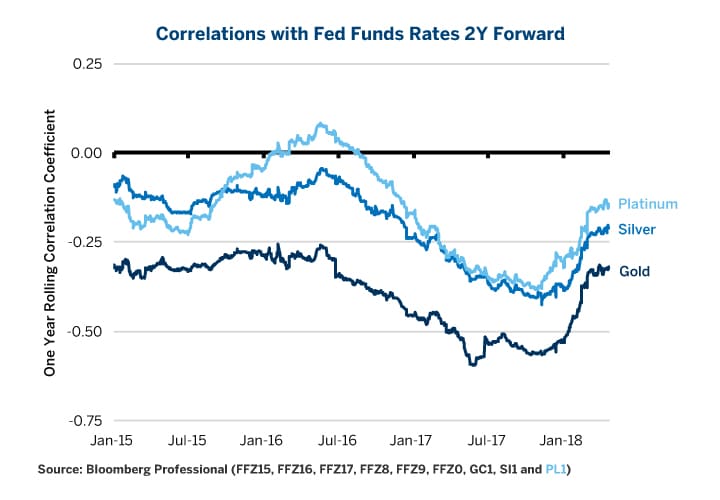

Part of the reason why gold options have been so calm of late is a lack of direction in gold prices -- this is surprising given the persistent rise in Fed Funds futures rates, which now price two or three more interest rate hikes in 2018, to be followed by one or two more in 2019 (Figure 2). Normally, higher interest rates would be bad news for gold, which typically has a negative correlation to movements in Fed Funds futures expressed as an interest rate (it has a positive correlation with Fed Funds futures expressed as a price). That correlation has weakened over the last several months (Figure 3).

Figure 2: Fed Funds Futures Are Pricing Far More Rate Hikes Than They Did Four Months Ago.

Figure 3: Gold Still Correlates Negatively with Fed Funds but Less So Than in the Past.

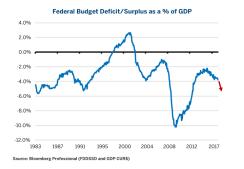

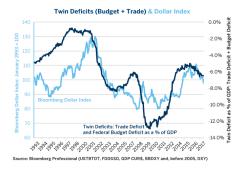

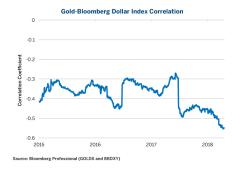

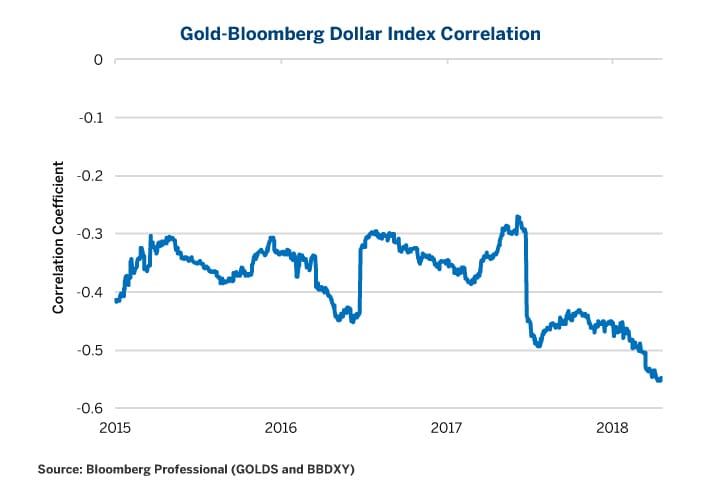

The reason why the correlation has weakened has a great deal to do with the fiscal deterioration underway in the United States. Deficits were rising even before Congress enacted its recent tax and spending legislation. In 2016, the budget deficit was only 2.2% of GDP – down from 10% in 2009. In 2017, the deficit expanded to 3.6% of GDP. As a result of the December 2017 tax legislation and the March 2018 spending bill, the U.S. budget gap is likely to approach 5% of GDP by 2019 (Figure 4). Wider budget deficits, combined with a slight expansion of the trade deficit, is putting the U.S. dollar under downward pressure (Figure 5) and this is overwhelming any benefit the dollar might receive from a tighter monetary policy. Gold typically has a negative correlation with the dollar – so a weaker dollar often means higher gold prices (Figure 6).As such, when it comes to gold, the bearish forces of tighter monetary policy are being almost perfectly offset by the bullish forces of a looser fiscal policy. So long as these forces remain at loggerheads and are roughly evenly matched, gold prices will likely continue to range-trade and implied volatility will likely remain at low levels. But for how much longer will fiscal and monetary policy remain opposing forces?

Figure 4: U.S. Fiscal Deficit Will Likely Deteriorate Further in Coming Years.

Figure 5: Twin Deficits (Budget + Trade) Correlate with the Strength/Weakness of the Dollar.

Figure 6: Gold Correlates Negatively with the Dollar Index, so a Weaker Dollar is Good for Gold.

When Fiscal and Monetary Policies Align

That the U.S. is entering a phase of expansionary fiscal policy after nine years of economy recovery is, to say the least, unusual. Deficits shrank as the 1980s expansion wore on into the later stages in 1988 and 1989. During the 1990s expansion, deficits turned into surpluses. Deficits also moderated during the brief expansion from 2003 to 2007 despite the negative fiscal consequences of the 2001 and 2003 tax cuts. Finally, deficits shrank for the first seven years of the current economic expansion as those tax cuts and the 2009 reduction in payroll taxes expired in 2013. At any rate, fiscal policy will likely remain loose and bullish for gold for a while.

In the meantime, monetary policy looks set to remain bearish for gold, at least for the next couple of years. The Fed’s “dot plot” chart suggests two or three more rate hikes in 2018, three additional hikes in 2019 and possibly one or two more in 2020. If the hikes materialize, it is likely that they will produce a flat yield curve by next year and a recession sometime in the early 2020s. It’s not really clear that the Fed can hike rates at that pace without triggering an economic downturn, especially given that the American economy is more highly leveraged than it was before the crisis in 2007. Any economic downturn could be massively bullish both for gold prices and the implied volatility on gold options for two reasons:

- An economic downturn will likely force the Fed back to zero rates, and rate cuts will most likely be bullish for gold.

- A recession would almost certainly cause a further fiscal deterioration for the U.S. which could also be bullish for gold – especially if the U.S. fiscal situation deteriorates more quickly than that of other countries.

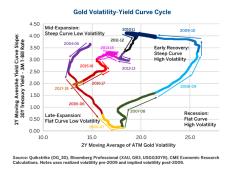

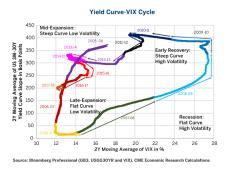

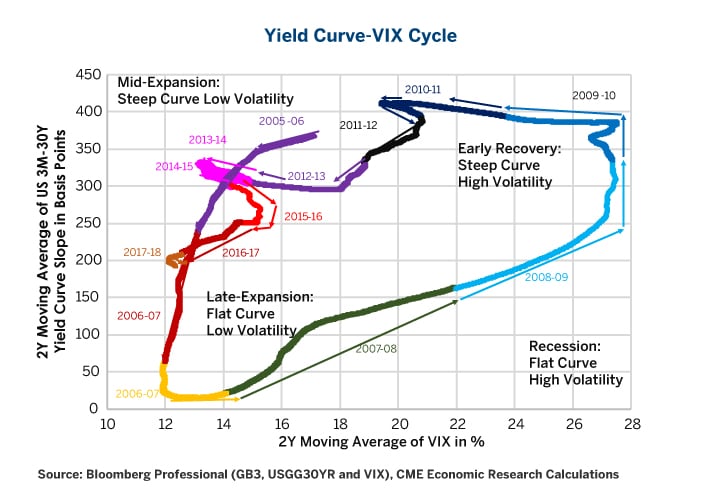

- Recession: high/rising volatility, wide/widening credit spreads, rising unemployment that is preceded by a flat yield curve and features a steepening yield curve.

- Early Recovery: High volatility and wide credit spreads coupled with a steep yield curve and high unemployment. Unemployment, credit spreads and volatility typically crest during this period and begin to recede.

- Mid-Expansion: Low/falling volatility, narrow/narrowing credit spreads and falling unemployment are coupled with a still steep but now flattening yield curve as the central bank begins tightening policy. Unemployment continues to fall.

- Late-Expansion: Flat yield curve and low but rising volatility/narrow but widening credit spreads. Unemployment hits bottom and may begin to rise.

If past is prologue, this is how things could evolve: The Fed will continue to hike rates in 2018 and 2019, flattening the yield curve. Volatility could remain low for perhaps another 12 months but, at some point, the Fed would have made one hike too many. Given the lag between changes in monetary policy and its impact upon various markets (services and products, employment, credit and gold/equity/Treasury options), the effect is often not fully realized until 12-24 months after. As such, it's not unusual for the markets to ignore monetary tightening as they happen but then suddenly suffer the ill effects a year or two after they end. This was the case during the Fed’s previous tightening cycle: it completed 17 consecutive rate hikes in June 2006. For one year, even as cracks appeared in the real estate market, volatility and credit spreads remained contained. The economy continued to grow. Suddenly in the summer of 2007, everything erupted. By 2008, the economy was sinking into the Great Recession.

The Fed is hiking more slowly this time around but even so it risks eventually tightening too much and that moment could come sooner than many anticipate. As such, later in 2019 or in the early 2020s, markets in general (gold, bonds and Treasuries) could see an explosion in volatility, a sharp widening of credit spreads and a rise in unemployment. While one cannot preclude an even earlier upturn in volatility and credit spreads, it appears more likely that gold volatility will remain low for much of 2018 and that the real fireworks will begin later when monetary policy and fiscal policy quit fighting a tug of war and begin pulling in the same direction.

Figure 7: Gold Volatility-Yield Curve Cycle Follows a Similar Pattern to Stocks, Bonds and Spreads.

Figure 8: Equities Are Completing Their Third Volatility Cycle Since 1990.

Bottom Line

- Fiscal policy has been weakening U.S. dollar while supporting gold.

- Monetary policy has put the brakes on any gold rally.

- As gold range-trades, implied volatility has plunged.

- Gold’s cycle of volatility appears to be similar to that of equities and Treasuries.

- At some point the Fed is likely to have tightened too much and provoke an upturn in credit spreads, unemployment and volatility across assets, including gold.

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author(s) and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

{kind=link}

{kind=link}

{kind=link}