The Fed’s deregulation package is one of the most highly anticipated events in the financial markets in 2018. Any deregulation is likely to have a large impact on bank balance sheets and, by extension, swap spread in USD markets. Below is a look at various possibilities for deregulation, as well as the impact each scenario will likely have on swap spreads.

For overall context, however, bear in mind that at the bank holding company level, US G-SIBs have a consolidated 5% leverage ratio requirement: 3% supplemental leverage ratio (SLR), plus 2% additional leverage buffer, or enhanced SLR (eSLR). It is also noteworthy that, in December, the Basel committee updated its guidance for the additional leverage buffer, and now recommends an additional leverage ratio buffer equal to 50% of a bank’s risk-based G-SIB surcharge, which are as yet unknown for 2017.

Here are what each of the US G-SIBs expects their fully phased-in G-SIB surcharge to be as stated in their most recent SEC filings:

At the moment, the implications are massive for banks, and the variables are unknown:

- Will the eSLR be “scrapped?” Or will it be “reduced?”

- Will the replacement “risk-sensitive leverage buffer” be equivalent to current Basel guidance of 50% of a bank’s risk-based G-SIB surcharge?

It’s difficult to know what the full effects of the Fed deregulation proposal until its finer details are known, but we have performed analysis of four possible scenarios involving the eight US G-SIBs. The first two scenarios are in line with the proposal reported by Risk.net. The remaining two are in line with previous assumptions that cash and/or Treasuries would be given an SLR exemption. Our scenarios are as follows:

- 1) No SLR exemption for cash or Treasuries. The eSLR is “scrapped entirely” and replaced with Basel’s risk-based leverage buffer.

- 2) No SLR exemption for cash or Treasuries. The eSLR is “drastically reduced” to 50bp, with an additional leverage buffer according to Basel’s recommendation

- 3) SLR exemption for cash, no change to the eSLR

- 4) SLR exemption for both cash and Treasuries, no change to the eSLR.

- Leverage is simply capital/assets. (SLR is actually defined as Tier 1 Capital/Total Leverage Exposure, but the numbers are very close.)

- All banks maximize assets and maintain minimum leverage ratios necessary to comply with leverage requirements. (Again, technically untrue, as all banks maintain actual leverage ratios in excess of minimums.)

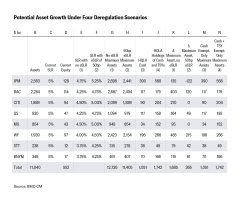

- Column E (scenario 1): 3% SLR + 50% of each bank’s risk-based G-SIB surcharge.

- Column F (scenario 2): 3% SLR + 0.5% eSLR + 50% of each bank’s risk-based G-SIB surcharge.

Scenarios 3 and 4 are more straightforward, simply exempting certain assets from SLR calculations. Therefore, the change in allowable assets is simply the stock of exempted assets on current balance sheets. (For clarity, these amounts are shown in columns I and J.) Columns M and N show the growth in assets made possible by exemptions for either just cash (scenario 3) or both cash and Treasuries (scenario 4). These numbers are not directly the asset size growth made possible by exemptions, rather, they represent the asset growth of non-cash/TSY assets possible. That’s because, once exempt, banks could add additional cash/Treasuries that would be exempted as well (more on this later).

Bringing it all together, columns K and N show the asset growth made possible by each of our scenarios – and the “Total” column reveals why so much is dependent upon the actual wording of the deregulation proposal. If the proposal scraps the eSLR entirely and replaces it with Basel’s guidance as described above, potential asset expansion totals nearly $1.7 trillion. This is more than the expansion if only cash were exempted from SLR calculations, and nearly as much were cash and Treasuries exempted. This would not justify a large move narrower in long end swap spreads because balance sheet would still become significantly cheaper.

However, if the eSLR is only “drastically reduced” from the current 200bp to just 50bp, and Basel’s additional liquidity buffer is implemented, potential asset expansion is merely $365 billion. That would be a strong negative for long end swap spreads.

In addition to the most potential asset expansion, a cash/Treasury exemption has two other important knock-on effects that make it preferable for investors holding long end spreads. Thus, we offer two caveats:

- Our analysis does not capture the entire asset expansion advantage that would come from a cash/Treasury exemption. Banks with asset sizes between $250 billion – $700 billion are subject to the SLR but not the eSLR. Therefore, they would realize no additional expansion from the proposal to reduce the eSLR. However, they would benefit from a cash/Treasury exemption, allowing for additional asset expansion.

- The Treasury exemption would incentivize banks to hold Treasuries to a larger degree than the proposal to reduce the eSLR. With banks further incentivized to hold Treasuries, liquidity in the long end of the Treasury market would improve, allowing swap spreads to widen more aggressively.

metric is similar to expansion under a cash/Treasury exemption scenario, such a proposal should

be considered a marginal negative for swap spreads. In all, we consider the impact of each deregulation scenario on swap spreads as: 1) slightly negative 2) strongly negative 3) slightly supportive, and 4) strongly supportive.