This blog is part of a new series on Institutional Investor entitled Global Market Thought Leaders , a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is AllianceBernstein, who will be providing analysis and insight into equities.

Over the past year it has been extraordinarily difficult for active equity managers—especially bottom-up stock pickers―to deliver premium returns, and skepticism about the value of active management has fueled wholesale shifts by many investors into passive portfolios. While an array of statistics out there might seem to suggest that active management is dead, I, for one, would say, “not by a long shot.”

The most powerful indicator of active-management potential, in my view, is dispersion, which combines correlations among stock returns with the level of individual-stock volatility. The best combination for active managers comes from low correlation (stocks aren’t moving up and down together, so there’s more opportunity for active managers to pick winners) and high stock volatility (when there are big variations in stock movements, there’s more opportunity for active managers to win big).

Today, with investors tarring most stocks with the same brush, correlations among pairs of stocks in the S&P 500, for example, are in the 0.7 range, an unusually high level, comparable with what we saw in the financial meltdown of 2008 and the market crash of 1987. Volatility has actually been muted for most of the past two years until spiking in the last few months.

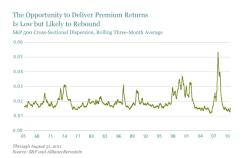

Put recent high correlation and muted volatility together, and the dispersion picture is not pretty. Dispersion for the three months ending August 31 was about 0.015―half its long-term average of approximately 0.03 and close to a 40-year low (Display). That suggests very limited opportunity for active managers to earn their keep.

Indeed, faced with investors’ flight to perceived safety, potential winners have been very hard to identify of late. In 2010, for example, the median active managers of US and global equity portfolios delivered dismal returns versus their respective benchmarks. But that’s only one side of the story.

Correlations, volatility and dispersion are all fluid statistics; for example, we expect correlations to carve out a new, somewhat higher, mean—but still retreat from their current high levels. Given the uncertainties about the European sovereign crisis and global economic growth, stock volatilities will likely remain elevated in the near term. Overall, the effect should be to increase dispersion, as indeed may just be beginning to happen. Active managers will pounce on even a slight rise in dispersion, bringing their research to bear on separating the wheat from the chaff among thousands of stocks.

And while opportunities may be harder to find for active managers in a low-dispersion environment, that doesn’t mean they don’t exist. While investors have decidedly soured on most financials, they’re kinder toward (and more discriminating about) some of the more defensive areas, such as consumer staples and healthcare. There are also cash-rich, high-quality companies scattered throughout the market selling at bargain prices. Focusing research in those arenas may yield benefits in the near term.

To paraphrase Mark Twain, the reports of active management’s death are greatly exaggerated.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein

Andrew Chin is Global Head of Quantitative Research and Investment Risk Management at AllianceBernstein