California State Treasurer Bill Lockyer wants to make sure his state's financial crisis doesn't become the catalyst in the next ‘Big Short’ on Wall Street. He put all 86 firms involved in the state's underwriter pool on notice that their quarterly reports to the state, starting with the last quarter of 2010, must include their municipal Credit Default Swap (CDS) activity. And, Lockyer asked Congress to ban naked trading in order to avoid speculation in muni CDS, but the request didn't make it into the Dodd-Frank reform bill.

General Obligation (GO) bonds, loans taken out by states, municipalities and authorities to pay for capital improvements and some not-so-long term expenditures, lately have lost their luster as a safe, tax free investment. Bond funds were falling even before financial analyst Meredith Whitney made the now infamous late fall 2010 pronouncements of muni defaults to come, and have suffered withdrawals of over $20 billion in November.

The State of Washington has no CDSs against its bonds, although its bonds are included in some indexes, the Washington State Investment Board (WIB) acknowledged in a written statement to Institutional Investor. "On a fundamental level, we expect the investment banks we work with to be our partners in the marketplace, not our adversaries." Implicit in that, said a spokesman, is the understanding that they won't bet against the state's bonds. The state didn't even raise the issue in its 2009 RFP for underwriters. But the WIB did include a provision in its RFP to be returned in the first half of this year, which states that banks wanting to underwrite cannot short their bonds.

CDS fears are warranted. Much of the shouting that rocked US Senate chambers during the post credit crisis hearings was sparked when Senate investigators realized banks were shorting the very instruments they were selling by dealing in CDS contracts – what Michael Lewis coined, ‘The Big Short,’ in his book of the same name. Look at what happened to housing when the CDS market took off against Mortgage Backed Securities (MBS) and their derivatives, Collateralized Debt Obligations (CDOs). The overwhelming demand for CDS, much of it by people not invested in MBS, actually fueled the market's appetite for the riskiest mortgages to be used in creation of the CDOs that the CDSs were betting against. Could the same scenario happen to GOs? Institutional Investor has already reported on Wall Street's plans for boosting liquidity in the muni markets.

Could bond buyers be encouraged to simply buy a CDS to hedge their investment and skip the more difficult task of analyzing the credit quality of a GO (which could undermine the positive impact of the free market to get governments to operate more efficiently)? And might people who missed the big MBS/CDS opportunity see this as their next big chance?

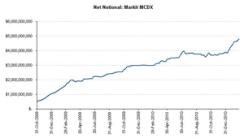

As the graphic from Markit below shows, investor interest in muni CDS has climbed. "Interest in the municipal CDS market has been growing steadily as a way to take a credit view on municipal debt and as an indicator of the market-perceived risk facing municipal borrowers," says Otis C. Casey III, Director of Credit Research for Markit, a London-based global financial services company that tracks a basket of 50 municipal issues.The weekly volumes represent the 'net notional' protection, meaning the sums are taken after counterbalancing positions are canceled out, bought by muni CDS counter-parties in Markit's muni credit default index (MCDX).

Markit draws the CDS volume data for its index from the Trade Information Warehouse, operated by the NY-based Depository Trust Clearing Corporation (DTCC), which records bilaterally agreed OTC contracts. "The volumes show that for the index, the total net protection [muni insurance] buying expanded from just under $500M in 2008, to nearly $5B for the week of Feb. 22, 2011," says Casey. Importantly, these positions are based on the whole index. Consequently, they don't represent individual contract risk, but the net amount of insurance a party may have to pay his counter-party if a credit event were to occur for all credits in the index and the amounts recovered from their bonds were zero. Also, actual payments would depend on the recovery rate for the underlying bonds.

"Anytime you have rank speculation without intelligent decision making you get an over-bought market," says Brett Schundler, the former mayor of Jersey City, who created securitized tax lien-backed bonds during his administration of that cash-strapped city. "You could have people just rushing in because they saw people make a bundle on MBS/CDSs and say, 'I hear the next market to blow up is going to be munis. I don't know the credit quality of this state's GO, but I bet I'll make a bundle on these things.'"

From a market perspective, the presence of an insurance product, like muni CDS, "could make investors more confident in buying bonds," adds Schundler, who is also a financial professional formerly with Salomon Brothers. "Anything that adds to liquidity in the market is potentially a good thing." On the other hand, negative rumors about a GO can scare people into paying more for insurance. "The potential exists for both," he says.

Meanwhile California's Treasury office is still slogging through the reports from its underwriters pool. According to the spokes person, "some members of the pool no doubt have traded in California CDS. The question is the extent to which they have been net short or long, and the extent to which those positions have been taken in market-making or propriety trading." But all six major banks have already told the state they have no clue as to why their clients buy California CDS or the extent of their market-making activities in naked trading of California CDS.

"Warren Buffett says if you're twenty minutes into a poker game and don't know yet who is the patsy, you're probably it," says Schundler. "One would presume the insurers, the writers of these contracts, are actually going to do their homework on the credits that they're guaranteeing," so that premiums and fees will be appropriate.

Still, it's got to make residents of struggling states a little uneasy to think as they commute home at night that there are a growing number of investors, whose risk reward is greater if a bond defaults, out there betting against your recovery to the tune of 50 or 100 times premium.