For more than a year now, investors have been questioning the efficacy of quantitative investing. Much of their questioning has to do with performance. Many quant strategies have simply failed to deliver on their investment promise over the past few years. The problem, the reasoning goes, is that everybody knows about these strategies, so there are no returns left. It was this very argument that the editors of Institutional Investor recently posed to us, as they asked whether quantitative equity investing has a future. The fact that we have been asked this question suggests that many people think the future of quantitative investing is bleak. After all, upon seeing a good friend in full health — or even on death’s doorstep — would you really approach the person and say, “Great to see you — are you still alive?”1 If you have to ask, you probably think quant investing is already dead.

Before we begin, a brief description of what quants like us do is in order. In general, quantitative strategies choose investments based on objective measurable data points, such as a stock’s price-earnings ratio or the recent sales growth of a company, rather than on subjective “gut feeling” decisions (how a company organizes its stores or whether you trust its management team). Of course, almost all investors rely on some quantitative data in making decisions. But quant investors — on the whole — try to minimize their reliance on subjective inputs.

The subjectivity in quantitative investment management generally comes at the model design stage, not on the fly. It comes from deciding which data are important in determining a stock’s prospects and which are not — and this can come both from economic intuition and from the evidence of back tests and real-life experience. The characteristics quants look for have a logical intuitive explanation and usually correspond with what most “qualitative” analysts are already doing in their own subjective way. But applying these criteria with discipline allows quants to explain the precise reason they hold any stock in their portfolios. We think this transparency is a unique property of quantitative investing and one that belies the “black box” label and “HAL 9000” imagery often associated with it.

Another key difference between quantitative and nonquantitative management is diversification. Quantitative investors can research a much broader range of stocks, whereas nonquantitative investors often hold more concentrated portfolios. And although there are some quant strategies that use high-frequency trading to capture very short-term opportunities, the majority of quantitatively managed equity assets are in portfolios where rapid turnover or trading is avoided because of the transaction costs involved.

For most quantitative managers two of the most important factors in assessing an investment’s prospects are value and momentum. Value simply means favoring investments that are cheap, trading at a lower price versus fundamentals than comparable investments (though even among quants there is great variety and disagreement over how to best measure value). Momentum means favoring investments that are improving or on the upswing. These factors are so widely used that almost any quant will toss out these terms while explaining his investment process. Nor are they unique to quant investors. A nonquant stock picker who tells you he looks for “cheap stocks with a catalyst” is basically saying he likes stocks with good value and momentum.

In our opinion someone who says quant equity investing has no future is basically saying that value and momentum will no longer work to pick investments. As we noted above we can see where people get this idea. Many investors using these strategies have had poor recent performance, and it’s clear that these strategies are no longer a secret.

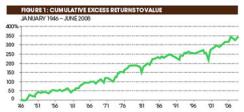

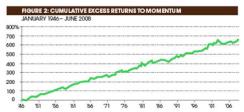

Although we can’t “prove” that quant investing has a future, we can demonstrate that quant strategies have had a successful long-term past — and that their recent performance is not inconsistent with this track record. To do so we use the returns for value and momentum developed by Eugene Fama and Kenneth French and available on French’s Web site.2 Their value index tracks the performance over time of a portfolio that is long cheap stocks (which Fama and French define as those with a high book value relative to their market price) and short expensive stocks (those with a low book value relative to their market price). Their momentum index tracks the performance of a portfolio that is long stocks with strong momentum (relatively good returns over the trailing year) and short those with weak momentum (relatively bad returns over the trailing year).

We use these data sets because they are publicly available (so our work can be verified), not subject to our own data mining and not particularly subject to data mining by Fama and French (they’ve been producing these measures in much the same way since at least the early 1990s). They represent very basic versions of value and momentum with little attempt made to improve them, adapt them to current market conditions or fix them when they have not worked for a while.

The results of the analysis are shown in the two charts on the right. The conclusions are pretty striking. The value index (Figure 1) has earned a fairly steady positive return over time. The technology market bubble of 1999–2000 was clearly a wild ride, but if you plot the returns over more than 60 years, performance is still right on trend. Do you detect a major deterioration in the power of this strategy over the past few years? We don’t.

The momentum index (Figure 2) shows a similar upward trajectory. The past eight years see a flattening out but hardly a disaster, and still positive. And, again, the cumulative return would barely be below trend, and the statistical significance of any recent alteration in performance is nonexistent.

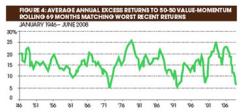

To approximate what many real world quants do, we simply combine the Fama-French value and momentum indexes 50-50. This comes out to be a far lower volatility portfolio than either value or momentum alone as these are negatively correlated strategies. Thus, to make this index comparable, every month we look back three years and we lever the 50-50 combo so its realized monthly volatility equals the average of the separate value and momentum portfolios.3

Figure 3 plots the results. Again, we see a very consistent (actually much more consistent) strategy through time. It’s not that this strategy never loses — it certainly does lose sometimes — but rather that it has worked over an unusually long period. You could again look at the period since 2002 and say it has flattened out. On the other hand, you could go back a few years more and say that period was the best stretch ever.

Let’s delve a bit more into the issue of recent performance. The flattish period in Figure 3 is worst when measured from October 2002 through June 2008, a 69-month period. To analyze what happened, in Figure 4 we plot the rolling 69-month returns of this 50-50 value-momentum portfolio going back to 1946. One prone to histrionics might say, “The world has changed!” If someone, in fact, says that to you, slap that person hard and tell him to get back into the fight.4 First, we chose the 69 months to correspond to the recent observed bad period for the strategy. (And remember that “bad” is a relative term; the strategy still went up!) Second, given this extreme bias toward negativity, it’s actually quite astounding that this is not the worst such precisely timed period. Two other periods have been worse, and one nearly the same, all while the strategy rolled merrily along over the past 60 years, recovering from such periods nicely. This does not prove the strategy will work going forward, but certainly shows that it has worked over a very long period and that nothing looks strange now, which is a big step in the right direction.

No analysis of the past performance of quant strategies could be complete without some discussion of August 2007. The radical negative returns to quantitative stock selection early that month — some have used the ridiculous phrase “–25 standard deviation event,” which translates to “I have no idea what the words ‘standard deviation’ mean”5 — and the smaller, but still radically positive, subsequent returns later that month do not show up in the monthly Fama-French data.

There are several reasons for this. First, Fama and French create portfolios that are always $1 long and $1 short. Real-life quants often try to target a constant volatility, not a constant dollar exposure (along with often targeting a specific beta). Volatility had been low for several years before August 2007, and this led many quants to raise their dollar exposures (leverage if in a long-short portfolio, deviations from a benchmark if in a traditional portfolio). The Fama-French portfolios ride out such low (and high) volatility periods without adjusting leverage, though this causes their realized volatility to vary. Thus, going into August 2007, typical quants were at higher than normal leverage while the Fama-French approach was not.6

Second, the wild ride really happened intra-August. By looking at monthly holding periods, we see only the much less wild summary. The main way to really hurt yourself in August 2007 was to have reduced your positions near the lows of the intramonth pain. The Fama-French strategies did not do that. (In the real world, as a general rule the more levered players did some version of taking the strategies off intramonth, at the worst time, while the players with little or no leverage did not.)

Last, the Fama-French value and momentum data don’t have a lot of bells and whistles, which ironically, in that fateful August, hurt the more sophisticated quants far more than those following the simpler strategies. Fama and French do not adjust for industry bets; they let them fall out of the data. Real-world quants often will limit or eliminate their industry bets, and value was a far bigger failure in early August if you hedged out your industry exposures. Fama and French rely only on book-to-price (or as we practitioners prosaically call it, price-to-book). Many active quants use a variety of value measures, and book-to-price was one of the ones to suffer least (perhaps because some of the others resemble measures used by aficionados of leveraged buyouts and this period coincided with a massive retreat from these structures).

Now these are all reasons that the simpler Fama-French portfolios did better in August 2007. This does not mean they always do better. In fact we, and many other quants, do not follow the very simple strategies precisely because we think many of the bells and whistles are indeed somewhat better over the long term and a true source of value added and differentiation. But for a little under two weeks in August 2007, that was certainly not the case!

What about the notion that quant equity strategies can’t work because everybody knows about them? Clearly, value and momentum are not a secret. But here’s the funny thing: In a general sense we can actually assess how many people are pursuing these strategies, particularly with respect to value, and how many people, whatever their reasons, are doing the opposite. We use a number we call the value spread, which represents the difference in valuation between cheap and expensive stocks (where cheap is based on a variety of factors such as price-to-earnings and price-to-book ratios). Cheap stocks are always cheaper than expensive stocks, of course, but the value spread shows how cheap they are relative to history. If lots of investors are pursuing value investing, the spread between cheap and expensive stocks narrows. If investors are avoiding value stocks, the spread widens. Today the spread is very wide.

Why is this relevant? Well, if “everyone” knows about these strategies and adjusts their portfolios to overweight value stocks, then the value spread would presumably contract. But, in fact, the value spread widened substantially in 2007 and remains quite wide. Essentially, while many declare that traditional quant strategies are overcrowded and not the place to be going forward, the strategies are simultaneously looking cheaper than normal (where “normal” itself has led to some great long-term returns). We are fond of saying that if these strategies are truly horribly overcrowded, then someone has apparently forgotten to tell the prices.

Those who argue that quant equity strategies have stopped working because everybody knows about them generally add a corollary: To avoid sure death quants must change everything. We believe that some competitors, academics and consultants are overreacting by advocating (in an occasionally hysterical fashion) this “you must radically change or die” policy. When you have great long-term strategies that have had a bad period, we don’t think the right reaction is to throw them out and look for new ones.

The tried-and-true strategies still look pretty great. Furthermore, brand-new uncorrelated great strategies do not become easier to find just because we really want them now. It is perhaps good marketing to say you’re going to find them, though even here we do not agree (that is, “Forget what we told you last year, now we’re going to build the really good models”). In addition, we think it’s poorly timed, as the more well-known stuff looks extra attractive right now.

In fact, we believe that changing what you do as a direct response to tough times often means making significant alterations at the worst possible moment. Every human bias that makes our models work over time also makes us want to “fix” them when they are temporarily “not working,” and this in our view is a very negative risk-adjusted-return strategy. H.L. Mencken sums up the bias toward a complex shiny new model versus a simple tested-and-true old one: “An idealist is one who, on noticing that a rose smells better than a cabbage, concludes that it will also make better soup.” In case you missed it, value and momentum are the cabbage.

This isn’t to say we don’t love research. Indeed, we love research to the point we should get a room. Our models today incorporate far more than just value and momentum, and even our measures of value and momentum have evolved considerably over time (some of this we published when we were younger and stupider about such things). But the research many are calling for to save quant investing looks to us like an overcorrection and some wishful thinking.

Apart from the arguments already described, some say that quant equity strategies cannot continue to work in the current economic and market environment, particularly given their need for shorting and leverage. The availability of leverage has decreased, while its cost has increased, and the “tail” risk associated with leverage is well known and widely feared. Meanwhile, almost every country in the world has experimented with some restrictions on short-selling. Now that regulators have crossed this Rubicon, who can say they won’t be going back and forth across it for years to come?

Within the universe of quantitative strategies, these concerns apply only to hedge funds. Quant strategies can be implemented quite nicely without any shorting or leverage in long-only portfolios (which we believe still constitute the bulk of all assets managed using such strategies). But since hedge funds can offer investors pure, laser-focused exposure to these strategies (without any equity market risk coming along for the ride), they are an important part of the quantitative universe.

For quant hedge funds the new environment for leverage and shorting may be troubling, but it is hardly a death knell. The kind of leverage quant strategies use is mostly confined to traditional stock borrowing and margin lending. For lenders this remains an attractive business. Margin loans on stock are well collateralized, with assets that remain easy to fund, easy to price and easy to liquidate, if necessary. Meanwhile, a more volatile world that makes leverage more difficult is the same world that lets quants use less leverage while still reaching their risk targets. So their total borrowing costs may actually come down. You see, there is some good news in a riskier world!

On the shorting side quant managers tend to hold very broadly diversified portfolios. This means that the importance of shorting any one stock, or even a group of stocks, is actually quite limited. For quants, shorting restrictions are just one more constraint that goes into the portfolio construction process (not that we like constraints!). In our portfolios, for example, the bulk of our long and short positions are industry-neutral. So if we can’t short financial stocks for some period of time, we, and most quants, simply skip that sector and continue to hold hundreds of stocks long and short in all of the other sectors of the market.

Some argue that quantitative techniques cannot work in the uncharted waters of the current market environment. We believe that’s almost exactly backward. Yes, models cannot easily anticipate a subprime mortgage crisis — or the broader credit crisis we have now — or what the effects of such will be. But can nonquantitative managers? If so, we’ve missed the evidence. We think tough times will reward, not punish, the discipline and diversification of quantitative investing and cause the biases they exploit to be more, not less, profitable.

It’s not hard to see why people might think quant strategies are dead. Recent performance, fears of overcrowding and the current market environment could easily lead one to question the viability of these strategies. As we have explained, we don’t think most of these concerns hold water. But the good news is that they keep many people from investing in the strategies. And this brings us back to the very fundamental question of how these strategies can earn a return if everyone knows about them.

|

|

And that’s why the very fact that we have been asked to tell you if there is a future for quantitative equity investing is — to us — a very encouraging sign. Historically, reports of the death of many investing strategies have often been highly profitable investment opportunities, because they suggest that the strategies are close to hitting bottom. (Think of BusinessWeek’s famous 1979 “Death of Equities” cover story that came at the dawn of a period in which the Standard & Poor’s 500 index tripled in ten years.)

|

|

1. Of course, given what we do for a living, it’s pretty unlikely we’re going to come to a bleak conclusion. As people who live, breathe and feed our families with quant investing, we are biased observers, to say the least. We believe what we’re saying, but we also believe in disclosing biases.

2. Fama is the Robert R. McCormick Distinguished Service Professor of Finance at the Graduate School of Business at the University of Chicago, and French is the Carl E. and Catherine M. Heidt Professor of Finance at the Tuck School of Business, Dartmouth College. In the 1980s they began studying the historical returns of value investing in an academically rigorous way and today make their data available for others to study.

3. We also define 50-50 value-momentum itself based on a rolling three-year realized volatility of value and momentum separately (that is, if rolling three-year volatility is a reasonable proxy for the future, our 50-50 portfolio is driven equally by value and momentum). This precise choice is not very important to our results.

4. Of course when you think quant, the first thing that comes to mind is General George Patton.

5. In reality it means you did not know the distribution, not that you drew a true –25 standard deviation event. And those saying “–25 standard deviation event” probably get this too; we’re just having fun with them.

6. Our 50-50 “combo” portfolio does indeed lever, but if you do everything in equal dollars the graphs look pretty much the same.

7. The current evidence in returns, in the value spread and in the continued popularity of Jim Cramer’s TV show suggests that investors still like a good story more than a good price.