Broad European indices are up around 15% over the last six months and are now close to the multi-year peaks they reached in 2000, 2007 and 2015 before they subsequently corrected. This time around the improving economic and political situation, attractive relative valuations and a degree of under-allocation by investors should keep the bears from the door. It could, however, be time to dig that little bit deeper for more domestic-related opportunities.

Still room to run

‘European equities are no longer cheap, and many investors are asking just how much upside is left’, says Chanchal Samadder, Head of Equity Strategy, Lyxor. ‘In our view, the valuation gap with the US still makes them an attractive proposition, especially given better economic momentum and a pick-up in inflation. Still, it could be time to broaden your horizons’.

Among companies in the STOXX 600 index, 79% are less than 10% away from their 52-week highs, which suggests the rally has been fairly indiscriminate and that forgotten “gems” are few and far between. However, European equities are coming from far further back than their US counterparts so they still have room to run.

Source: Bloomberg, SG Cross Asset Research/Equity Strategy, 1 June 2017

Investors have ploughed $15 billion into European equity mutual funds and ETFs since the start of the year, but haven’t yet come close to reversing the $100 billion of outflows we saw in 2016. More inflows are likely to follow, but some caution is needed: the euro’s new found strength and frailties in the US market call for more of the selectivity we started to see in May. Until then, flows had focused on broad indices and large-caps, but small- and mid-caps have enjoyed a much greater share recently.

Currency complexities

May was the euro’s best month for some time, to the detriment of markets and companies reliant on overseas trade. Such was the price of Emmanuel Macron’s election in France, and the subsequent easing of political risk and ramp up in demand for eurozone securities.

Macron has now secured a large enough majority to make his ambitious reform agenda a much more concrete prospect. Widespread aversion to labour reform could still be a hurdle, however. The euro’s rise could be revived now that the result of French elections is clear, yet the ECB may act to manage this appreciation rather than face a fallback in inflation expectations.

Hit the mids

For return seekers, it becomes a question of how best to marry the search for upside with the desire to avoid the headwinds the strong euro poses for less domestic larger-cap indices. The answer lies in index exploration.

Some countries will be more affected than others, especially those like the DAX, which get the majority of their revenues from overseas. Markets such as the CAC, IBEX and MIB are less reliant on international trade (getting 57%, 61% and 60% of their revenues from the EU respectively).

With Dutch and French elections behind us, and risk seemingly contained in Germany, Italy has taken centre stage politically because of the rise of the euro sceptic Five Star Movement. ‘We are wary of political stress in the eurozone’s third-largest and second-most indebted country, especially as early elections remain possible’, says Samadder, ‘but it could be an attractive time to enter what’s still a cheap market despite its recent gains’.

The next layer down could, however, be more attractive. It’s not somewhere most investors naturally look, but mid-cap indices tend to be more reliant on domestic revenues than their larger peers. Germany’s MDAX index, for example, generates almost 60% of its revenue from the EU, while for France’s CAC Mid-60, that number is higher again. The index generates almost 70% of its revenues from the EU. Macron’s potential tax cuts could add further support and, unlike some European assets, French assets haven’t overshot yet.

Mid-cap indices also tend to be more cyclical (at least 20% typically) but they aren’t always as volatile as their reputation suggests, because the hot money tends to focus on ultra-liquid large-caps. That’s especially true in mainland Europe, where the MDAX and CAC Mid-60 have shown themselves to be marginally less volatile than their large-cap peers since the 2008 financial crisis.

Don’t skip sectors

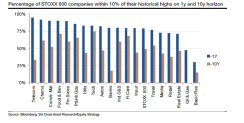

Better data and a potential post-election ramp up in infrastructure spending should provide support for domestic-related sectors such as banks and construction & materials, both of which also generate most of their revenues domestically. Only 17% of banks are within 10% of their 10-year highs, despite 80% of them being within 10% of their 1-year highs. This suggests looking at valuations rather than just prices, even if people tend to look solely at price action after large market rallies.

Rampant consumer confidence and the stronger employment picture should prove beneficial for the retail and autos & parts sectors – neither of which have really ridden the wave of European markets so far. ‘With no consumer to speak of, and hence no top line for the related stocks, returns had been extremely disappointing for retailers for some time’, says Samadder. ‘We now expect consumption to be the key engine for growth into 2021, so earnings should turnaround significantly’.

Ride the wave with Lyxor

Investors have already trusted Lyxor European Equity ETFs with nearly €20 billion. Lyxor offers some of the oldest, largest and most widely-traded single country ETFs in Europe, along with the most efficient CAC 40, FTSE 100, IBEX 35 and FTSE MIB ETFs on the market. Lyxor’s local knowledge allows its experts to dig deeper with greater ease, which is why it offers a number of mid-cap ETFs, including the only CAC Mid 60 and IBEX Medium Cap ETFs out there. Lyxor also has 20 different ways to invest in European sectors. No other provider lets you invest in Europe like this. .

Disclaimers:

Source: SG Research, European Equity Strategy Team. Lyxor ETF Research, June 2017. *All revenue breakdowns sourced from Factset, 1 & 5 June 2017. Opinions expressed are as at 1 June 2017. **Source: Lyxor International Asset Management/Bloomberg. Data period from 31/12/2015 to 31/12/2016. The rationale and construction of the indicator are detailed in an academic paper published by Thierry Roncalli, former Head of Research & Development at Lyxor and Professor of Finance at the Evry University, and Marlene Hassine Konqui, ETF strategist. The academic paper can be downloaded from SSRN: http://ssrn.com/abstract=2212596 or from REPEC http://ideas.repec.org/p/pra/mprapa/44298.html Past performance is not a reliable indicator of future results

This communication is for professional clients and qualified investors only.

This document is for the exclusive use of investors acting on their own account and categorised either as “Eligible Counterparties” or “Professional Clients” within the meaning of Markets In Financial Instruments Directive 2004/39/EC.

This document is of a commercial nature and not of a regulatory nature. This document does not constitute an offer, or an invitation to make an offer, from Société Générale, Lyxor International Asset Management or any of their respective affiliates or subsidiaries to purchase or sell the product referred to herein.

We recommend to investors who wish to obtain further information on their tax status that they seek assistance from their tax advisor. The attention of the investor is drawn to the fact that the net asset value stated in this document (as the case may be) cannot be used as a basis for subscriptions and/or redemptions. The market information displayed in this document is based on data at a given moment and may change from time to time. The figures relating to past performances refer or relate to past periods and are not a reliable indicator of future results. This also applies to historical market data. The potential return may be reduced by the effect of commissions, fees, taxes or other charges borne by the investor.

Lyxor International Asset Management (Lyxor ETF), société par actions simplifiée having its registered office at Tours Société Générale, 17 cours Valmy, 92800 Puteaux (France), 418 862 215 RCS Nanterre, is authorized and regulated by the Autorité des Marchés Financiers (AMF) under the UCITS Directive and the AIFM Directive (2011/31/EU). Lyxor ETF is represented in the UK by Lyxor Asset Management UK LLP, which is authorised and regulated by the Financial Conduct Authority in the UK under Registration Number 435658.