It wasn’t called Institutional Investor at first. Kaplan — the 26-year-old leader of what would become a global events, research, and media brand — made the same mistake that Facebook’s Mark Zuckerberg would make 37 years later: He put a “The” in front.

The “The” didn’t stop The Institutional Investor from early success. With backing from Seagram heir Gerald Bronfman, Kaplan’s magazine regaled those on Wall Street with the inside story of Wall Street. The best stories, one of his earliest editorial hires tells me, weren’t just about what happened behind the mahogany doors of the day’s reigning power brokers. The best stories, in Kaplan’s eyes, told the people behind those doors information they didn’t know about those very meetings: what the other side was thinking, who was influencing them, what was likely to happen.

Kaplan originally tasked George Goodman, the magazine’s first editor, with securing this access. (Goodman often wrote under the pen name Adam Smith and would gain fame as a pioneer of “New Journalism” alongside Hunter S. Thompson, Tom Wolfe, Gay Talese, and others.) Goodman’s resources were thin and his standards high. Fred Bleakley, who was hired in 1970, remembers one senior editor (himself) and three staff writers. “On one of my first stories, Goodman read it and said, ‘If you say this, they will hoot at us.’ It was his way of telling a writer that what he’d submitted wasn’t Institutional Investor quality.”

The best brands are early to their field, and Institutional Investor was that. The magazine quickly started rating sell-side analysts, producing data that would come to determine compensation packages for analysts the world over. To be a member of Kaplan’s All-America Equity Research Team meant you’d made it on Wall Street, and despite skeptics of the industry’s future, these rankings continue to be an annual obsession of analysts across the globe.

Within six years of founding the magazine, Kaplan purchased his first newsletter (The Wall Street Letter) and then, in the words of veteran newsletter leader Tom Lamont, “started expanding — into the trust business, corporate finance, options. We’d be adding a newsletter every year for five or six years. The culture was totally different from the magazine. These were the kids, the great unwashed down at the end of the hall, writing all this scandalous stuff, as opposed to the highbrow magazine people writing intelligent stuff on flashy paper for sophisticated people. From the moment we started, right up until the late 1980s or early 1990s, we were unique.”

The advent of the Internet inevitably depressed the newsletter and print business — but Institutional Investor (which long ago had dropped the “The”), early as always, had an answer: events. Eventually led by Diane Alfano and reaching its apogee in the form of the Institutional Investor Roundtables, the group still dominates the global market for bringing asset managers and allocators together.

How was Kaplan always early? “Because the guy had 20/20 foresight for what was going to be important,” Lamont says. “He had an uncanny knack for ideas that worked. Take, for example, something as simple as 401(k)s. People were vaguely aware of them when they started, but Gil knew we could do something. We started a newsletter on it, and the magazine covered them, well before many of our competitors.”

Yet time — like the media business — waits for no man.

As Institutional Investor enters its 50th year, we are faced with the pressuring confluence of two trends. The first, in my view, is cyclical, the second universally accepted as secular: a shift toward passive investing, and a move away from simple branding ads that for so long perpetuated this great media brand.

It is with this in mind that we are continuing what Gil Kaplan started in 1967: perpetual change and disruption, starting with this magazine.

I’ll leave the business-side changes aside — they are, after all, our competitive advantage! — but the editorial changes we are making will, with this redesigned issue, become clear.

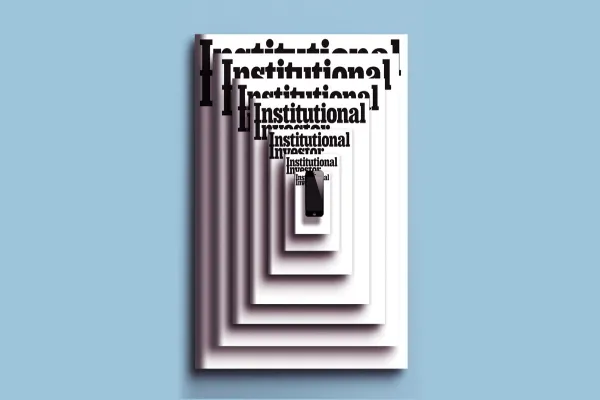

Start with our logo. For longtime readers, the two large words dominating the top of our cover will remind you of the heyday of Institutional Investor. That is intentional. For readers in the 1980s and into the 1990s, Institutional Investor was an essential read. (As Michael Bloomberg once told employee Heidi Fiske, “It was the only magazine really covering what was going on.”) By echoing the logo of that era as we look forward, we aim to once again become essential to our audience.

But as with books and people, it’s what’s inside a magazine that really counts. I believe people open Institutional Investor in print or online for three reasons: to help grow their portfolios, to help build their businesses and teams, and to expand their social currency — applying the idea that sharing interesting information has value.

Thus we have reorganized the front of the magazine, which we’ll mirror online shortly, into three sections: Social Currency, Corner Office, and Portfolio. The stories within those sections, as well as within our features and research (now Masters) sections, will adhere to two broad rules: They will be written, laserlike, for institutional investors and the people who service them, and they will aim to provide the reader with four elements — the access Gil Kaplan so valued, the disclosure essential to original journalism, quality writing, and the exposure of conflict. These, according to Graydon Carter of Vanity Fair, are essential for the production of good journalism. Institutional Investor’s goal is to be 75 percent respected — and 25 percent feared.

These changes will spill over, intentionally, into other Institutional Investor realms, including our events and video content. But make no mistake: At the base of this transformation remains a commitment to the high-quality written word. Kaplan would have accepted nothing less.

I asked Tom Lamont recently if Kaplan appreciated quality content. “He absolutely did — and he wanted to provoke people,” Tom said. “Not unfairly, but he loved sticking it to people — and it had never been done before. He would get calls from people who were screaming about stories in a newsletter. Gil and I would get on the phone with the person who was complaining. He’d be incredibly empathetic, but when we’d hang up he’d slap me a high five.”

Bring on the high fives.

Kip McDaniel is the Editorial Director and Chief Content Officer of Institutional Investor.