While talk of the U.S. entering a Lost Decade appear wide of the mark, a number of demographic and economic trends in Europe are eerily similar to those seen in Japan.

For instance, Europe’s engine of growth today, Germany, is expected to witness a labor force decline that is not only greater than that of other euro zone peers, according to United Nations’ data estimates that extend from 2011 to 2036, but is one that ranks among the worst in the world (alongside that of Japan). By closely examining the structural changes occurring in Europe, it becomes abundantly clear that the continent faces economic headwinds well beyond its current trouble. As mentioned, Germany is expected to see roughly a 20 percent decline in its working age population in the next two decades or so, while France, the region’s second-largest economy, will stagnate at close to zero growth in its working population. Additionally, Portugal, Italy, Austria, Netherlands, Switzerland, Finland and Greece are all estimated to see declines in working age population of between 7 percent and 15 percent, with the former countries faring more poorly than the latter.

In contrast, the United Kingdom, Canada, Sweden, Norway, the United States, New Zealand and Australia are all developed market countries that should see modest expansion to working age populations during this period, and as we argued in the previous installment of this article, the U.S. actually holds relatively favorable demographic characteristics. Why do demographic trends matter so much? In our view, and as has long been argued in much economic literature, working age population growth rates can have a meaningful impact on the rates of nominal GDP growth, which strongly suggests that many European countries face stiff demographic headwinds to improved economic growth in the years ahead. Additionally, there also appears to be some compelling evidence to suggest that Europe’s economic troubles are not merely cyclical in nature, but rather could represent early signs of deeper problems for the region.

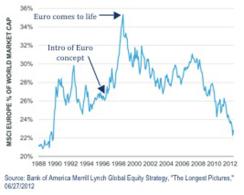

Indeed, according to Bank of America Merrill Lynch Global Equity Strategy research, when looking at historic long-term trends in economic growth, Europe as a whole also does not fare well. For instance, from an extremely long-term perspective (from 1900 to 2011), continental Europe saw its share of global GDP decline from 25 percent to 21 percent, while the United Kingdom saw a much more precipitous decline over this period, from 12 percent to 3 percent. Taken together, Europe as a whole saw the greatest losses in share of global output, while Asia (ex-Japan), Latin America and North America saw gains. Over the past two decades, Japan has seen its share of global GDP roughly cut in half, to less than 9 percent. In some sense, then, European economies have already been experiencing a secular relative decline, which can also be seen in the region’s dramatic drop in share of global equity market capitalization (see Figure 1). All these factors suggest that even with an eventual solution to the euro zone sovereign debt and banking crisis, the inevitable longer-run outcome for European economies may well still be very slow growth, high levels of indebtedness and a Japan-like economic malaise.

Figure 1: European Markets Decline as a Percentage of Global Market Capitalization

Chart 1

Source: Bank of America Merrill Lynch Global Equity Strategy, "The Longest Pictures," 06/27/2012 |

Rick Rieder is BlackRock’s chief investment officer of Fixed Income, Fundamental Portfolios.