Since European Central Bank President Mario Draghi’s speech in late July promising to do “whatever it takes” to preserve the euro, followed by the announcement of an ECB program to buy short-dated peripheral government bonds under some circumstances, euro area markets have rallied and the single currency zone has faded as a source of concern for markets in the U.S. and elsewhere. Investors who earlier in the year were closely following the ins and outs of Greek coalition politics have turned their focus to other topics, in particular fiscal cliff negotiations in the U.S. While it no longer represents an imminent threat to global risk assets, however, the euro area crisis continues to unfold, and sooner or later it will return to the headlines. Indeed, bad news about euro area growth and renewed tension about Greece have likely contributed at the margin to the U.S. equity market sell-off in the past few weeks.

The coming months will likely bring a mixture of good and bad news about the euro area. The improvement in financial conditions achieved in recent months, if maintained, should help generate somewhat stronger growth for the region in 2013. That pickup in turn may represent part of a broader narrative of improving business cycle conditions outside the U.S. By contrast, the euro area’s institutional progress likely will remain fitful at best, leaving the region vulnerable to bouts of political disturbance and worsening sentiment.

For now, three moving parts within the euro area story deserve investor attention:

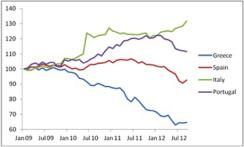

Financial conditions have improved significantly, but are now at risk. The ECB’s successive actions over the past year — especially the LTROs and more recently the yet-to-be-implemented OMT announcement — have by no means solved the euro area crisis, but they have done much to ease financial tension. Peripheral bond spreads have narrowed significantly (Chart 1), and both the Italian and Spanish governments have maintained their once-threatened access to the primary market. Euro area equities climbed more than 20 percent from late July to mid-September, though they did not quite return to their March peak. As a whole, euro area stocks this year have come close to matching the S&P500, though with considerable divergence across specific markets in the region. The German DAX, for example, has jumped more than 20 percent thus far in 2012, while Spanish equities have shed about 10 percent in U.S. dollar terms. The euro currency itself rallied against the dollar between July and September in response to the ECB, reversing an earlier dip and taking it back close to its end-2011 level. Equally importantly, capital flight from the peripheral countries appears to have slowed. Bank deposits have generally stabilized (Chart 2), and imbalances within the euro area’s internal payments settling system (TARGET2) have stopped worsening. Over time, these factors should help reduce bank lending rates facing corporations and households in peripheral countries, which have been slow to fall in response to ECB rate cuts. With a lag of a few months, these declining risk premia and borrowing rates should serve to lift euro area growth, in particular by lessening downward pressure on the peripheral economies.

Euro area peripheral bond spread and equities

Chart 1

Source: Bloomberg, JPMAM; data as of November 19, 2012 |

Peripheral country bank deposits (Jan 2009 = 100)

Chart 1

Source: European Central Bank, Bank of Greece; data as of September 2012 |

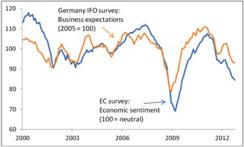

Nothing doing yet on the growth front. While our forecast includes improvement in euro area growth during 2013 — with GDP gains averaging just over 1 percent through the course of the year — no obvious sign of improvement has yet appeared. GDP contracted 0.2 percent Q/Q, SAAR in the third quarter, following a 0.7 percent dip in the second quarter of 2012. Neither did the monthly data flow improve during the course of the quarter. Perhaps more worrisome is that surveys are not showing any improvement in business or consumer confidence thus far, even though these indicators might be expected to reflect the improved financial environment quite quickly. To take two examples, both the overall EC Survey measure of economic sentiment and the Germany-specific IFO business survey continued to weaken through November, though the IFO’s expectations component did at least stabilize at a weak level (chart 3). For now, the euro area continues to struggle under the weight of ongoing fiscal austerity, an impaired financial system, and lower but still significant risk premia. With economic activity already at a weak level, the region is not experiencing a severe recession. But the roughly zero growth environment for now implies an ongoing increase in the euro area unemployment rate, weak corporate profit growth, and limited popular support for governments.

Euro area confidence surveys

Chart 1

Source: JPMSI; data as of October 2012 |

Shaky institutional progress, with Greece back in focus. While euro area leaders continue to support further integration rhetorically, actual institution-building is moving ahead very slowly. Most obviously, progress toward a banking union is unfolding at a glacial pace, with as yet little agreement on the division of labor between regional and national regulators and no facility yet in place to support pooled deposit insurance. More concerning in the short run, though, is the ongoing plight of Greece.

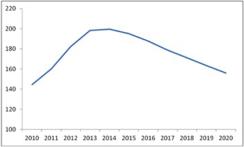

In partnership with the IMF, Greece’s euro area partners are funding the country, via the EFSF, while Greece carries out its large fiscal adjustment. The hope is that Greece’s efforts will eventually result in regained access to the primary market. The lenders’ current review of Greece’s progress, ahead of the next aid disbursement, resulted in fresh demands for more austerity measures, which precipitated a brief crisis within the Greek parliament. Ultimately, lawmakers approved the new round of cuts as well as the full 2013 budget. But new projections prepared as part of the review process highlight the debt burden, which remains crushing even after last year’s write-down of privately held bonds. With the economy mired in recession, the Greek public debt ratio seems unlikely to drop to 120%/GDP — a level adopted by the official lenders as a benchmark at which the country might be able to return to private debt markets — within the next 10 years (chart 4), even assuming herculean and sustained austerity efforts by the local authorities and a return to economic growth by 2015.

Greece public debt/GDP projection (%)

Chart 1

Source: JPMSI, European Commission; data and forecasts as of November 2012 |

With little appetite for returning to existential-crisis mode, euro area governments will probably continue disbursing loans to Greece, with or without IMF support. Having won approval for the 2013 budget, the government seems unlikely to fall in coming months. But ongoing debate within the country as well as among the euro area lenders about the long-term sustainability of the current process will keep Greece close to the headlines, until the official lenders decide either to write down their claims or force Greece out of the single currency. The possibility of the latter move, however small, makes it unlikely that currency and convertibility risk premia will disappear entirely from the euro area periphery.

For markets, the base-case scenario of improving euro area growth based on easier financial conditions implies (1) moderately favorable prospects for euro area stocks in 2013, although their performance this year has been sufficiently good that a further bounce does not look inevitable; (2) mild strengthening of the euro currency, with risk premia continuing to decline and the ECB unlikely to pursue an easier overall monetary policy stance than the Fed next year; (3) with limited euro implosion risk, continuation of the current global low-volatility atmosphere, especially in fixed income and currencies. Much depends, however, on the expected return to at least mildly positive growth in the euro area. Ongoing recession would further undermine popular support in the peripheral countries for fiscal adjustment, as well as region-wide enthusiasm for stepped-up integration. Lack of institutional progress would in turn limit the ECB’s willingness to serve as an aggressive lender of last resort, and breakup risk would rise anew. In this atmosphere, the tailwind for global markets from euro area developments would turn back into a headwind, likely with particularly negative consequences for global financial equities and credit.