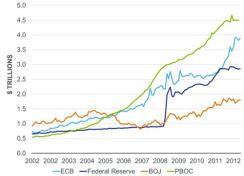

The initial shock of the global financial crisis on economies worldwide forced central banks into taking dramatic action in 2008, and of course, high degrees of monetary accommodation have been part of our economic and investment landscape ever since. To combat deflationary pressures and anemically growing economies, the world’s largest central banks have been growing their balance sheets to both try to stave off euro zone contagion and to supplement slow velocity of money resulting from depressed levels of credit creation (see Figure 1). The extent of this balance-sheet expansion has been extraordinary, and today major central bank balance sheets are almost as large as 30 percent of global equity market capitalization, up from close to 12 percent in 2008. Central banks will continue their attempt to execute on monetary policy to stimulate growth, avoid deflation risk and maintain low real rates, as we saw last week from the European Central Bank (ECB), but the timing of action is more of an open question, as is its ultimate impact on real economies.

Figure 1: Central Bank Balance Sheet Expansion Continues Apace ($ Trillions)

Central Bank

Source: Deutsche Bank |

In the end, perhaps we may begin to see a reversal (or at least a slowdown) in the flows of money that have dramatically shifted capital to the euro zone core from the peripheral countries. This eventuality, should it occur, might go some distance toward restoring confidence in the region’s stability, thereby bringing private capital flows back in a meaningful way. The key for policy makers in ensuring that market access remains (at viable interest rate levels) for the majority of the regions’ nonprogram countries (since Greece, Portugal and Ireland are already limited in market access) is first stabilizing and then restoring a high degree of market confidence. The maintenance of confidence, in all forms of investing, is perhaps the dominant, if sometimes underappreciated, component of a credit-based capitalist system. Indeed, the origins of the word “credit” are to be found in the Latin credere, meaning “to believe or to trust,” and these characteristics undergird the activities of lending and borrowing now as much as ever.

Turning briefly to the United States, we still believe that quantitative easing by the Federal Reserve is highly likely to be implemented, despite our view that the U.S. economy is stabilizing and is not likely to fall into recession. There are several reasons for this belief, but a central pillar to the thesis is the fact that the Fed isn’t anywhere close to achieving its mandate of healthy labor markets. The unemployment rate remains elevated, and the employment-to-population ratio has flatlined at an extraordinarily low level. Additionally, we have so far not seen any definitive relationship between U.S. money printing and domestic inflation, although we did make the case last year that QE had influenced inflationary outcomes abroad, which can then result in some imported inflation. Further, as bank lending and credit creation is slowly improving in the U.S., there is a considerable incentive for the Fed to maintain monetary accommodation to facilitate this recovery, as well as to incentivize the corporate sector to increase capital expenditures as economic uncertainty abates.

We shall see if Chairman Bernanke follows Mr. Draghi’s lead this week, and if the Fed does move, we will be watching to see how bold the steps taken are. We believe that the Fed still has considerable room to use more aggressive communications as part of its approach to monetary policy, and we would not be surprised to see the FOMC explicitly introduce the idea of a more open-ended form of quantitative easing, in terms of both purchasing amount and timing. Moreover, they may consider setting either growth or employment triggers that would add predictability to how QE may be implemented. Assertive monetary policy is buying time on both sides of the Atlantic, but at this point we need to see greater focus on the structural factors inhibiting faster growth.

Rick Rieder is BlackRock’s chief investment officer of Fixed Income, Fundamental Portfolios.