The S&P 500 has outshone most of its global peers during the past year despite persistent disappointment about U.S. economic growth. Against a sea of red numbers elsewhere, the S&P rose (in price terms) 3.1 percent in the 12 months to June 30. While many factors have driven this performance, one partial explanation lies in the fact that the pace of U.S. growth, while hardly spectacular, has run fairly close to the economy’s underlying trend or potential rate of GDP expansion, believed to be just over 2 percent. In many other countries, while growth has easily exceeded that of the U.S., it has fallen well short of these economies’ trend rates. Investors have correspondingly marked down earnings expectations, and equity markets have punished these shortfalls.

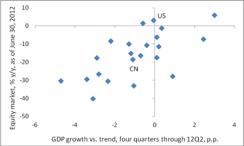

Chart 1 illustrates this connection. It plots, for a sample of 22 markets, the average quarterly GDP growth rate for the four quarters through the second quarter of 2012 relative to each country’s trend growth rate (using our estimates for this figure as well as for the second-quarter GDP reading) against the year-on-year percentage change in the equity market as of June 30, 2012. Though hardly perfect, the relationship looks genuine. The labels identify the U.S. as well as China, where stocks have fallen sharply despite GDP growth nearly six percentage points above the U.S. In China’s case, its growth over the past year has undershot the economy’s likely trend rate of around 9 percent by more than one full percentage point.

GDP growth vs. trend and equity market performance

Chart 1

Source: Bloomberg, JPMAM; data as of June 30, 2012 |

Second, and equally importantly, earnings themselves likely display high sensitivity to the relationship between actual and trend growth. In general, economies with high trend growth rates experience high interest rates as well, boosting the cost of capital relative to slower-growth countries. Interest rates in emerging economies, for example, routinely exceed those observed in developed economies (for a variety of reasons, among which is faster growth). This higher capital cost creates a higher bar for companies to jump over in making profits. In thinking about corporate earnings growth, then, investors should think not just about absolute economic growth, but growth relative to its underlying trend.

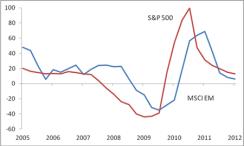

The tie between earnings and growth relative to trend helps explain why emerging-markets (EM) earnings growth does not always exceed U.S. earnings growth, despite GDP growth that runs considerably faster (by about four percentage points in real terms, and by roughly six percentage points in nominal terms). Chart 2 shows earnings growth for the MSCI EM index against the S&P 500, back to the start of reliable data for the former in the mid-2000s. Admittedly, for the period as a whole, EM earnings growth did easily top S&P 500 earnings growth (14.2 percent on average, versus 7.3 percent; note that inflation and currency appreciation against the dollar contributed mightily to EM earnings growth, on top of real GDP gains). Since the end of 2007, though, earnings growth rates for MSCI EM and the S&P 500 have basically matched each other. And partial data going back to the mid-1990s suggests a much narrower gap between average EM and S&P 500 earnings growth for that longer period. Very strong EM earnings growth in the 2004–'07 period coincided with an extended run of above-trend economic growth that eventually led to overheating in many EM economies; since 2008 average EM GDP growth has generally run at or slightly below its roughly 6.4 percent trend.

MSCI EM and S&P500 trailing 12-month earnings growth (% y/y)

Chart 1

Source: MSCI, Standard & Poor’s, JPMAM; data as of 12Q1 |

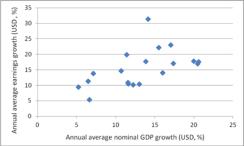

MSCI EM country component GDP and earnings growth, 2004-12Q1

Chart 1

Source: MSCI, JPMSI, JPMAM; data as of 12Q1 |

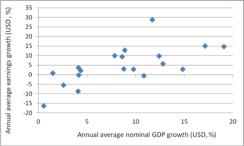

Chart 1

Source: MSCI, JPMSI, JPMAM; data as of 12Q1 |

In terms of the outlook for the next few quarters, U.S. economic growth — its current soft patch notwithstanding — seems likely to hold within shouting distance of its trend rate. With other major economies, especially the euro area, likely to continue struggling, an overweight position in U.S. equities (within an overall equity portfolio) still appears warranted. Meanwhile, our forecast shows EM economic growth remaining below trend through the rest of 2012 but gradually reaccelerating, helped by improvement in China as policy easing begins to take effect, with attendant support for the rest of EM Asia. This prospective pickup appears to justify an overweight position in EM Asian equities as well; with Asia accounting for nearly 60 percent of the MSCI EM, an overweight position in the overall index probably represents a satisfactory proxy.

Opinions and estimates constitute our judgment and are subject to change without notice. Past performance is not indicative of future results. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.