I’m just now getting around to reading the OECD Review of Swedish National Pension Funds by Clara Severinson and Fiona Stewart. The report, which was released in April, carries quite a bit of importance for those of us that study the structure, process and governance of public institutional investors. Why? Because, after more than a decade of operation, we may get some useful insights from the Swedish case as to ‘what works’ and ‘what doesn’t work’ for public institutional investors.

Encouragingly for the AP Fonds, the OECD has quite a bit of good news. Specifically, there’s plenty of praise for the funds’ good governance and low cost. Kudos. But, alas, there is room for improvement. And for the AP Fonds, one area where improvement is sorely needed is ‘investment restrictions’. As the OECD report flags up, the Fonds are subject to a variety of rules and constraints that make life rather difficult for the managers. For example, here’s the list of rules (lifted directly from the report):

- "Only investments in capital market instruments which are quoted and marketable are permitted.

- Direct loans are prohibited.

- No more than 5% of the funds’ assets may be invested in unlisted securities.

- These investments must be made indirectly via portfolio management funds or similar.

- At least 30% of the funds’ assets must be invested in low-risk, interest-bearing securities.

- No more than 40% of assets may be exposed to currency exchange risk.

- The funds also cannot invest in commodities.

- No more than 10% of a fund’s assets may be exposed to one issuer or group of issuers.

- Shares held in listed Swedish corporations may not exceed 2% of total market value.

- Each fund may not own more than 10% of the votes of any single listed company.”

Some of the restrictions above aren’t quite as bad, such as the restriction on the percent of assets that may be exposed to one issuer (i.e., 10%). But even that’s rather obvious. It’s a bit like restricting people to swim only in pools that have water in them. Aren’t we all smart enough to understand why it’s a bad idea? Do we need a rule saying as much?

As I see it, these investment constraints – and the constraints at peer funds around the world – reflect a lack of trust on the part of the sponsor in the governance and management of the funds. And, as a consequence, the non-expert sponsors impose on the finance professionals financial rules to ensure that the professionals don’t act like non-experts. Makes sense, right? Not to me – I can barely understand what I just wrote.

Wouldn’t it be better to be a bit less prescriptive and replace a rules-based approach for a more principled and flexible approach underpinned by an expert and reliable governance structure?

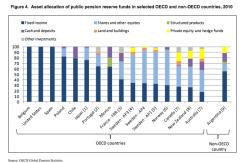

And this goes for all the funds with investment restrictions by the way. See below for the list – Sweden doesn’t even look that bad compared to some (e.g., USA).

In my view, plan sponsors should think harder about the constraints and limitations placed on the qualifications and skills of board members and less about the specific investment restrictions for investment managers. With a credible and expert Board – armed with a clearly articulated mandate and return objective – flexibility and prudence will beat fixed rules over the long term.