This blog is part of a new series on the Institutional Investor website entitled Global Market Thought Leaders , a platform that provides analysis, commentary, and insight into global markets and the economy from the researchers and risk-takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is AllianceBernstein , who will be providing analysis and insight into equities.

A “big data” revolution is under way, transforming the volume and nature of data generated throughout the economy. This trend — driven by the data-intensive nature of innovations such as social networking — is highly disruptive to the tech sector, creating fresh challenges and opportunities for investors.

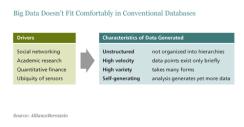

To the uninitiated, big data doesn’t sound all that inspiring. Yet it’s all around us, as the display below shows At one end of the spectrum is the huge amount of information involved in mapping the human genome (roughly 3 billion pairs of molecules), which requires computing power undreamt of when James Watson and Francis Crick revealed the structure of DNA in the 1950s.

At the other end of the spectrum is the massive amount of data that Google and Facebook gather and store when we search for books, CDs, information or friends. One doesn’t have to think hard to come up with other examples of modern human activity, from weather forecasting to quantitative finance, that require similarly huge volumes of information to function.

But most big data is, almost by definition, amorphous, unstructured, diverse, fleeting and endlessly regenerative. This makes it difficult to store in conventional computer systems and hard to organize and search. Little wonder that those who create it dump much of it as soon as it appears. Yet it is growing fast and is increasingly essential for science and business alike.

Indeed, our research suggests that big data will grow by more than 20 percent a year over the next decade. We forecast that by 2020, it will represent 35 zettabytes of computer storage capacity. (Simply put, a zettabyte is a one followed by 21 zeroes.) That’s 13 times the total volume of digital content expected to be generated globally this year, according to IDC, a research firm.

More importantly for investors, big data represents a huge market for business analytics, storage and servers that could be worth $71 billion, or nearly eight times its current size, by 2020.

Within the tech sector, the losers in this process are likely to be traditional hardware manufacturers because the large, centralized servers they manufacture can’t handle the quantities of data needed.

Tech winners are likely to include database software companies, data storage firms and makers of specialized “middleware” required to manage and analyze big data systems that use distributed computing approaches involving many computers in a network. Networking infrastructure companies that can help carriers move this massive amount of data around a network more efficiently could also benefit.

The stakes are equally high outside the tech sector. The winners will be those retailers, manufacturers, healthcare providers and companies of all kinds that find ways to harness the power and insight of big data soonest.

For investors, choosing the right company to back will be a critical choice, but a hard one. Many of the key players are unquoted companies, or are divisions of larger firms, such as Oracle, IBM and SAP. Many will be involved in takeovers, which can both create and destroy value. Some of the early leaders will inevitably fall by the wayside as the market develops.

As the painful history of the dot-com boom and bust reminds us, making the right choice requires in-depth knowledge and strong nerves. Good research will be key to harvesting the big data opportunity.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Chris Toub is Director of Equities at AllianceBernstein.